The 2026 tax season has introduced a fundamental shift in how the Internal Revenue Service (IRS) views and tracks digital wealth. With the debut of Form 1099-DA (Digital Asset Proceeds From Broker Transactions), the era of self-reported “estimates” and inconsistent data has come to a definitive end. This new form acts as the digital equivalent of the traditional 1099-B, requiring centralized exchanges, hosted wallet providers, and payment processors to report gross proceeds directly to the IRS. For the taxpayer, this means that the “information gap” that once existed between private digital activity and federal oversight has been technically bridged by a standardized reporting infrastructure.

The implementation of the 1099-DA is not merely a paperwork change; it is a technical integration of digital assets into the broader federal tax enforcement system. In 2026, the IRS has the technical capacity to match data from millions of 1099-DA forms against individual returns, making it easier than ever to identify discrepancies in reported gains. This transparency is a direct result of the 2021 Infrastructure Investment and Jobs Act, which mandated a reporting regime for digital asset brokers to ensure that cryptocurrency and NFTs are treated with the same fiscal rigor as traditional stocks and bonds.

Ultimately, 2026 marks the year where digital asset compliance has transitioned from an “optional best practice” to a hard technical requirement. Taxpayers can no longer rely on the relative anonymity of centralized platforms to defer or omit capital gains reporting. As brokers furnish these forms by mid-February 2026, the focus has shifted from whether a transaction was “caught” to ensuring that the data reported by the broker aligns perfectly with the taxpayer’s internal records.

Reporting Timeline: 2025 Activity vs. 2026 Mandates

Navigating the 2026 filing season requires a technical understanding of the “transitional periods” established by the IRS. For the returns being filed in early 2026—which cover activity from the 2025 calendar year—brokers are primarily required to report Gross Proceeds from sales and exchanges. While some platforms may voluntarily include cost basis information for 2025, it is not yet a technical mandate for all “non-covered” assets, leaving the burden of historical basis calculation on the individual taxpayer.

However, as of January 1, 2026, the rules for “Covered Securities” have taken full effect for digital assets. Any digital asset purchased on or after this date must have its Cost Basis (what you originally paid) tracked and reported by the broker upon its eventual sale or exchange. This means that for the current 2026 activity year, the reporting will become significantly more granular, technically requiring brokers to store and transmit the acquisition date and price for every “covered” unit in their custody. The technical transition between these reporting standards can be summarized as follows:

- 2025 Activity (Filed in 2026): Mandatory reporting of Gross Proceeds; Cost Basis reporting is generally optional for brokers.

- 2026 Activity (Filed in 2027): Mandatory reporting of both Gross Proceeds and Cost Basis for assets purchased on or after Jan 1, 2026.

- Historical Assets: Assets held before 2026 remain “non-covered,” meaning you are still responsible for providing your own basis records if the broker lacks that data.

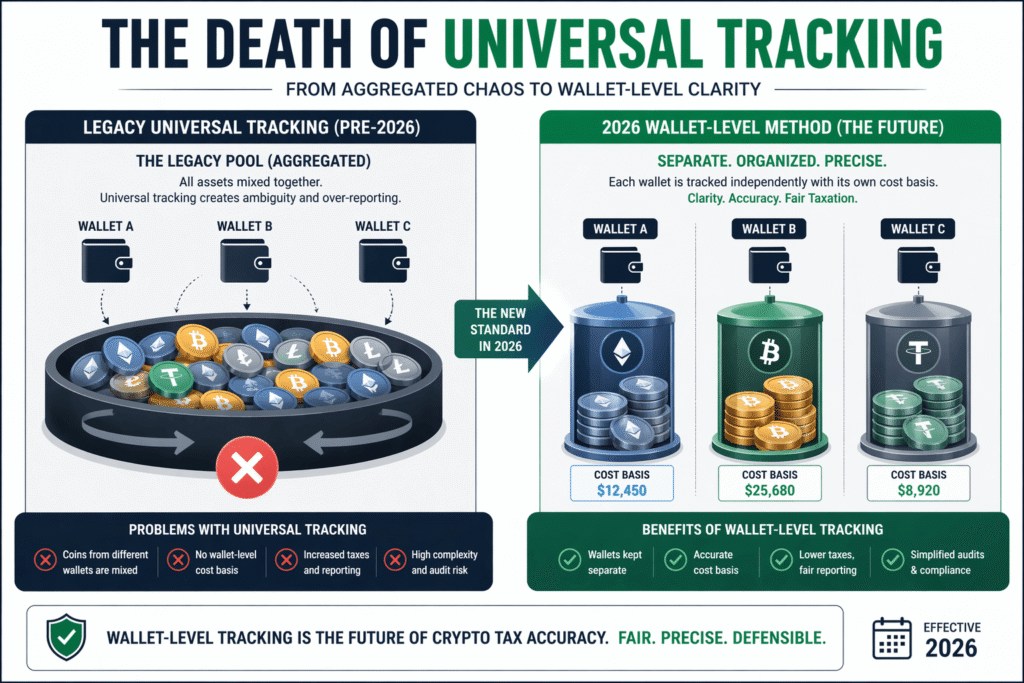

The Death of the “Universal Wallet” Tracking

One of the most profound technical changes in 2026 is the IRS’s official elimination of the “Universal Method” for tracking cost basis. In previous years, many taxpayers treated all their holdings of a specific coin across multiple wallets as one combined pool, allowing them to “cherry-pick” the highest cost basis from any wallet to minimize their gains on a specific sale. In 2026, the IRS mandates “Wallet-Level Tracking,” where cost basis must be maintained and reported on a per-wallet or per-account basis.

This shift requires a technical reconciliation of all assets held as of the start of the 2025 tax year. Under Revenue Procedure 2024-28, the IRS offered a “safe harbor” that allowed taxpayers to perform a one-time allocation of their “unused basis” to specific wallets by the time they file their 2025 returns in 2026. Without this specific allocation, a taxpayer who moves assets between platforms in 2026 risks having their basis disregarded by the IRS, which could technically result in the entire sale proceeds being treated as taxable gain ($0 cost basis).

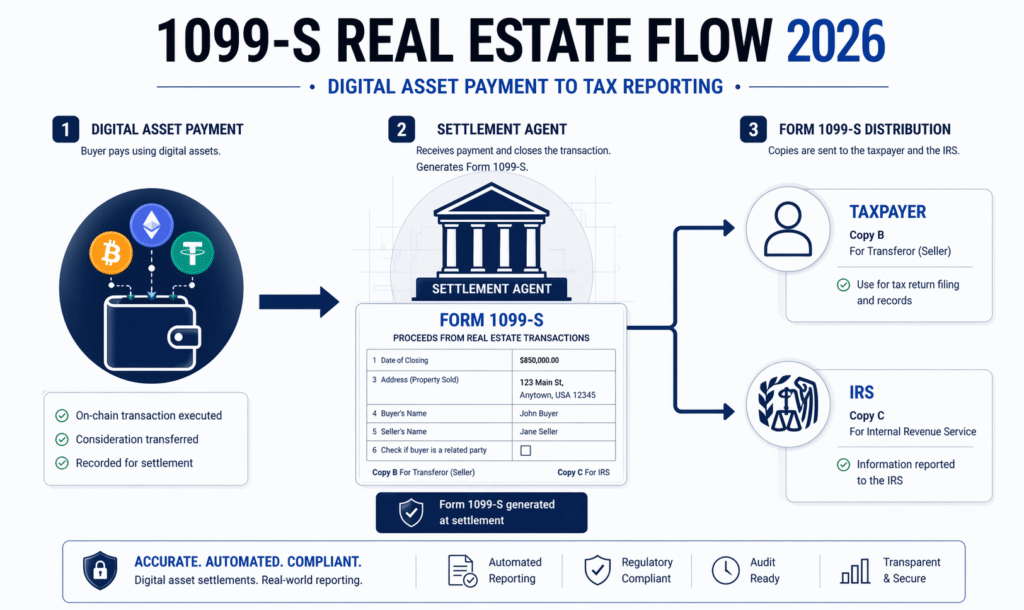

Real Estate and Digital Assets: The 1099-S Integration

The technical reach of 2026 digital asset reporting extends far beyond simple exchange trades; it has now officially integrated into the Real Estate Sector. Beginning in tax year 2026, any sale or exchange of real estate that involves digital assets as part of the consideration must be reported on Form 1099-S. This ensures that “crypto-to-real-estate” transactions, which were often opaque in previous years, are now subject to the same reporting triggers as cash or traditional financing.

For a 2026 real estate transaction, the settlement agent is technically required to report the Fair Market Value of any digital assets received at the time of closing. This creates a direct data link between the property transfer and the taxpayer’s digital asset disposition. If you use Bitcoin to pay for a vacation home in 2026, the 1099-S will notify the IRS of the exchange, technically triggering a capital gains event on the digital asset that must match the proceeds reported by the real estate entity. The 1099-S integration specifically targets three technical scenarios:

- Direct Exchange: Using a digital asset as a direct payment for a property title.

- Down Payment Funding: When digital assets are converted to fiat at the point of closing as part of the escrow process.

- Partial Consideration: Any transaction where digital assets are used to pay for a portion of the indebtedness or property value.

Backup Withholding and Compliance Penalties

The 2026 reporting regime includes a “teeth” mechanism known as Backup Withholding. If a taxpayer fails to provide a correct Taxpayer Identification Number (TIN) to their digital asset broker, the platform is technically required to withhold a portion of the transaction proceeds—typically 24%—and send it directly to the IRS. This ensures that even “non-compliant” users contribute to the federal tax base, though it can create a massive liquidity crisis for the individual during a high-value trade.

Beyond withholding, the penalties for inaccurate basis reporting have been technically sharpened in 2026. The IRS can apply a 20% accuracy-related penalty for negligence or substantial understatement of income. In cases where a taxpayer intentionally uses unsupported cost basis from a “universal pool” rather than the mandated wallet-level tracking, the IRS may treat the entire proceeds as a taxable gain, potentially leading to an effective tax rate far higher than the standard capital gains percentage.

| Event | Deadline | Technical Action Required |

| Furnishing to Recipient | February 15 – 17, 2026 | Broker must provide Form 1099-DA to the taxpayer. |

| Electronic Consent | 5 Days after request | Brokers must confirm electronic delivery preferences. |

| Standard Filing | April 15, 2026 | Taxpayer reports 1099-DA proceeds on Form 1040. |

| Extended Filing | October 15, 2026 | Deadline to reconcile complex basis across multiple forms. |

| Record Retention | 7 Years | Brokers must keep statements accessible for audit. |

FAQ: Navigating the 1099-DA Filing Season

What if I traded on a decentralized exchange (DEX) in 2026?

As of early 2026, the mandatory reporting for “unhosted” or decentralized platforms remains in a technical evaluation phase. While centralized brokers (CEXs) are required to issue 1099-DA forms, many DEXs may not yet have the technical infrastructure to do so. However, the IRS still requires you to report these gains on your 2025 return, even if no formal 1099-DA was issued by the platform.

What is the minimum threshold for receiving a 1099-DA?

The standard de minimis threshold for many 1099 forms is $600. However, for certain payments in tax years beginning after 2025, the IRS has explored increasing thresholds to $2,000. For the current 2026 filing season (2025 activity), you should expect a 1099-DA if your gross proceeds exceeded $600 at any single centralized platform.

How do I reconcile multiple 1099-DA forms from different exchanges?

Because the “Universal Method” is dead, you must technically verify that the basis reported on one exchange doesn’t overlap with another. If you moved crypto from Exchange A to Exchange B, Exchange B likely won’t have your original cost basis. In 2026, you must provide “Substantiation Documents” (trade logs) to prove your acquisition price and ensure your total gains are not over-calculated across multiple forms.

Is there a “Safe Harbor” for my 2025 cost basis reporting?

Yes, under Revenue Procedure 2024-28, you have until the time you file your 2025 return (mid-2026) to make a one-time allocation of your digital asset basis to specific wallets. This technically “locks in” your starting point for the new wallet-level tracking rules. If you miss this window, the IRS may disregard your historical basis in future audits.

Are Stablecoins and NFTs reported on the 1099-DA in 2026?

Generally, yes. The IRS defines digital assets broadly to include any digital representation of value that is recorded on a cryptographically secured distributed ledger. This includes stablecoins and most NFTs. Even if a stablecoin trade results in $0 gain (due to a 1:1 peg), the Gross Proceeds of the sale must technically still be reported on the 1099-DA.

What happens if my 1099-DA has a technical error?

You must contact the broker’s support immediately to request a Corrected 1099-DA. Do not file your return until the error is resolved, as an “Information Return” mismatch is the primary trigger for 2026 IRS audits. Most brokers are required to provide corrected forms within five business days of verifying the error.