The expiration of the Tax Cuts and Jobs Act (TCJA) at the end of 2025 marks a major shift for American taxpayers in 2026, bringing higher tax rates and significant changes to deductions.

The fiscal year 2026 marks a historic turning point in American taxation as the sunset provisions of the TCJA of 2017 officially take effect. For the past eight years, the individual tax code operated under a temporary framework designed to expire at the end of 2025 to meet federal budget reconciliation requirements. As a result, 2026 is the first year since 2017 that taxpayers are filing under the “Snapback” rules, which revert the Internal Revenue Code to its pre-2018 structure, albeit adjusted for nearly a decade of inflation.

This transition, often referred to by financial planners as the “Tax Cliff,” represents a technical reversal of most individual income tax cuts, while the permanent corporate tax rate reduction (21%) remains untouched. For the average household, this means that the mathematical assumptions used for long-term retirement and investment planning since 2018 are now obsolete. The 2026 code requires a complete recalibration of withholding strategies, as the lower marginal rates that defined the previous era have been replaced by the higher, more traditional tiers of the 1986 code (as amended).

Understanding the technical nuances of the 2026 snapback is critical for avoiding a massive underpayment penalty at the end of the year. While the 2017 law was marketed as a simplification of the code—primarily through the doubling of the standard deduction—the 2026 return to Personal Exemptions and more complex itemized deductions brings back a higher degree of technical variability. Taxpayers must now distinguish between “Taxable Income” and “Adjusted Gross Income” with higher precision, as the thresholds for various credits and deductions have shifted back to their legacy ratios.

2026 Individual Tax Brackets: A Technical Comparison

The most immediate impact of the 2026 shift is the rise in marginal tax rates across almost all income levels. Under the TCJA, the rates were 10%, 12%, 22%, 24%, 32%, 35%, and 37%. In 2026, these have “snapped back” to their previous levels of 10%, 15%, 25%, 28%, 33%, 35%, and 39.6%. This shift means that middle-class earners previously in the 22% bracket may now find themselves in the 25% bracket, representing a 13.6% relative increase in their marginal tax liability.

Technically, the “bracket creep” caused by this sunset is partially mitigated by the annual inflation adjustments performed by the IRS. However, the structural change remains significant for high earners, as the top marginal rate has returned to 39.6% for individuals earning over approximately $530,000 (indexed for 2026). The following table illustrates the finalized 2026 brackets compared to the expired 2025 TCJA levels:

| Marginal Rate (2025) | Marginal Rate (2026) | 2026 Income Threshold (Projected) |

| 10% | 10% | $0 – $11,925 |

| 12% | 15% | $11,926 – $48,475 |

| 22% | 25% | $48,476 – $117,350 |

| 24% | 28% | $117,351 – $223,450 |

| 32% | 33% | $223,451 – $485,725 |

| 35% | 35% | $485,726 – $531,000 |

| 37% | 39.6% | Over $531,000 |

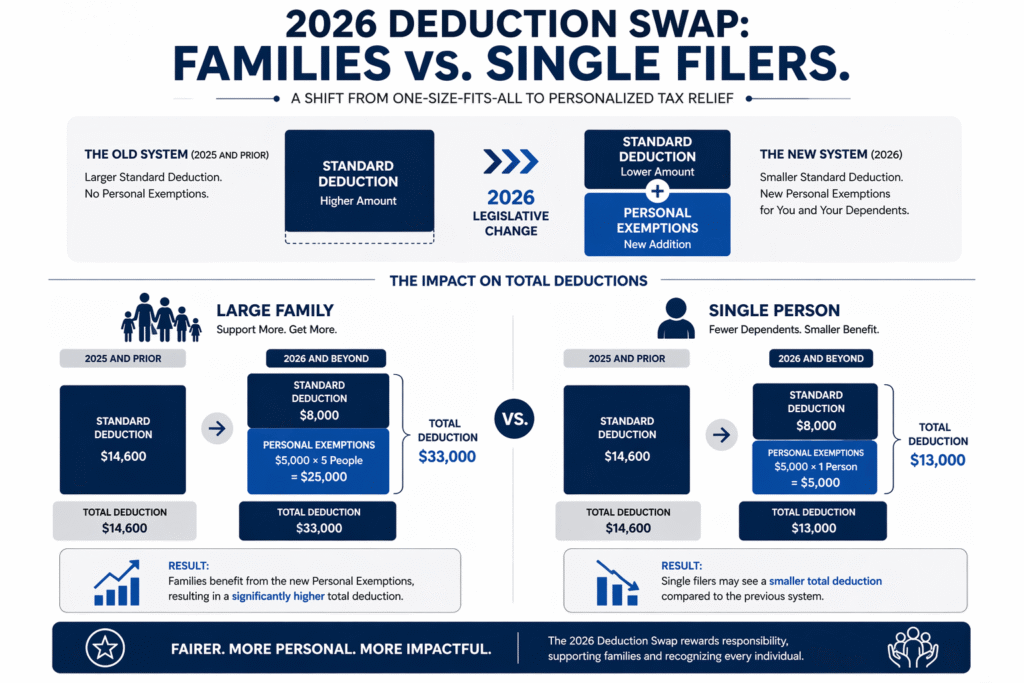

The Standard Deduction vs. Personal Exemptions

One of the most complex technical trade-offs in 2026 is the reduction of the Standard Deduction and the simultaneous return of Personal Exemptions. Under the TCJA, the standard deduction was nearly doubled ($12,000 for individuals, $24,000 for married filing jointly), while personal exemptions were suspended. In 2026, the standard deduction has dropped back to roughly half its previous level (adjusted for inflation), returning to approximately $8,300 for individuals and $16,600 for couples.

To compensate for this reduction, the tax code has reinstated the Personal Exemption, which is a specific dollar amount that can be deducted for the taxpayer, their spouse, and each dependent. For 2026, this exemption is estimated to be approximately $5,300 per person. This change technically favors larger families; for instance, a family of five may now be able to deduct significantly more through combined personal exemptions and a smaller standard deduction than they could under the high standard deduction of the TCJA era.

However, for childless couples or single filers, the 2026 shift is likely to result in a higher taxable base. The technical “break-even point” depends on the number of dependents and whether the taxpayer chooses to itemize. Because the standard deduction is so much lower in 2026, a much higher percentage of taxpayers will find it technically advantageous to return to Itemizing Deductions on Schedule A, requiring a more rigorous collection of receipts for mortgage interest, medical expenses, and charitable gifts throughout the 2026 fiscal year.

The SALT Cap and Itemized Deductions in 2026

The expiration of the TCJA marks the end of the controversial $100,000 State and Local Tax (SALT) Cap. Since 2018, taxpayers in high-tax states like New York, California, and New Jersey were limited to a $10,000 deduction for state and local income or property taxes. In 2026, this cap has vanished, allowing taxpayers to once again deduct the full amount of their state and local tax liability. This change provides a massive technical “tax hedge” for high-income earners in these jurisdictions, often offsetting the rise in marginal rates.

Beyond the SALT cap, several other itemized deduction rules have technically shifted back to their pre-2018 standards. The 2026 code has reinstated the 2% floor for miscellaneous itemized deductions, allowing professionals to deduct unreimbursed employee expenses, tax preparation fees, and investment advisory costs once they exceed 2% of their Adjusted Gross Income (AGI). This provides a new layer of “Career Deductions” that were technically unavailable for the past eight years. The finalized 2026 rules for itemized deductions include four critical shifts:

- SALT Deduction: The $10,000 limit is removed; full state/local taxes are now deductible.

- Miscellaneous Deductions: Reinstated for expenses exceeding 2% of AGI (unreimbursed work expenses).

- Mortgage Interest: The debt limit for interest deductions has technically returned to $1,000,000 (up from the TCJA’s $750,000).

- Charitable Contributions: The cash contribution limit has technically reverted from 60% of AGI back to 50% of AGI.

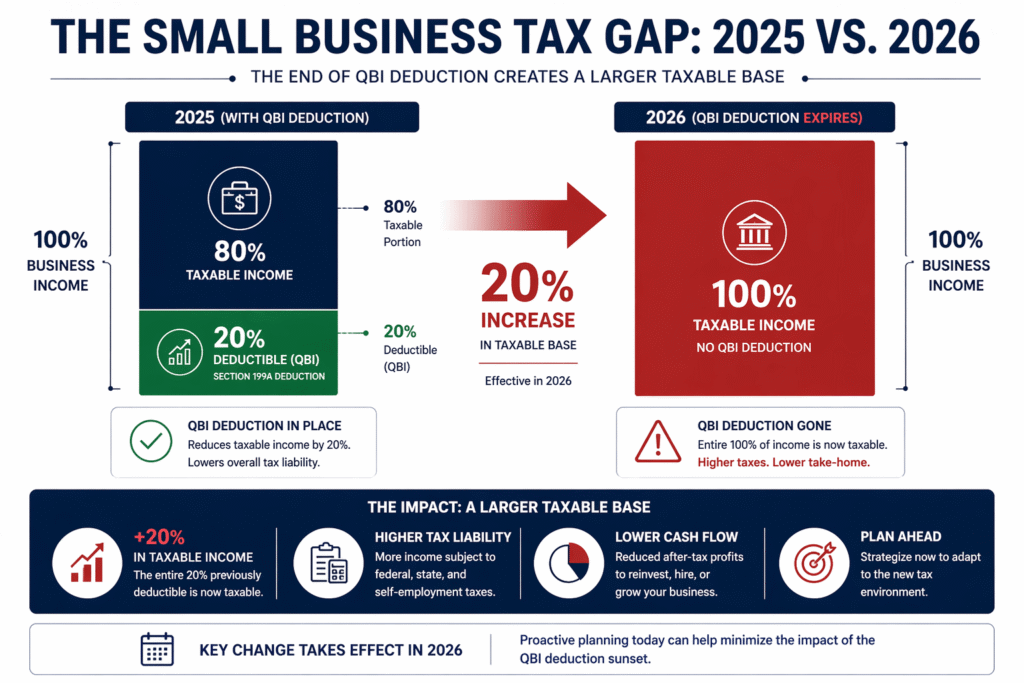

Small Business Impact: The Expiration of Section 199A (QBI)

For small business owners and “gig economy” workers operating as pass-through entities (Sole Proprietors, LLCs, S-Corps), the most significant technical loss in 2026 is the expiration of the Qualified Business Income (QBI) Deduction (Section 199A). This provision allowed eligible businesses to deduct up to 20% of their qualified business income from their taxable base. As of January 1, 2026, this deduction has ceased to exist, effectively resulting in a 20% increase in the taxable income for millions of entrepreneurs.

Technically, the loss of QBI means that a business owner’s taxable base is no longer “discounted” by the 20% factor. In the 2025 tax year, the calculation for taxable business income was:

In 2026, the formula has simplified but become more expensive:

This shift, combined with the rise in personal marginal rates, creates a “double-taxation” effect for small business owners who are now paying higher rates on a 20% larger income base. Strategically, this may lead many 2026 business owners to reconsider their entity structure, as the C-Corporation flat rate of 21% remains permanent under the TCJA, making the corporate structure technically more tax-efficient than the pass-through structure for the first time in nearly a decade.

FAQ: 2026 Tax Planning

Are Capital Gains taxes increasing in 2026?

The statutory rates for long-term capital gains (0%, 15%, and 20%) technically remain the same in 2026. However, because these rates are linked to the income tax brackets, which have shifted, more taxpayers may find their gains pushed into the 20% tier earlier than in 2025. Additionally, the Net Investment Income Tax (NIIT) of 3.8% remains in effect for high earners, potentially bringing the effective top rate to 23.8%.

What is the 2026 Estate Tax exemption limit?

The TCJA doubled the estate and gift tax exemption (to roughly $13.6 million per person in 2025). In 2026, this exemption has technically been cut in half, returning to approximately $7 million per person (indexed for inflation). For families with significant assets, 2026 is a critical year for “Gifting” strategies to move wealth out of the taxable estate before the lower exemption is applied to future transfers.

What is the “Bunching Strategy” for 2026?

With the lower standard deduction, “bunching” has become a vital 2026 technical strategy. This involves concentrating your deductible expenses—such as two years’ worth of charitable donations or elective medical procedures—into a single tax year. This ensures that you exceed the standard deduction threshold in the “bunched” year, allowing you to maximize the tax-benefit of itemizing.

How does the 2026 shift affect the Child Tax Credit (CTC)?

Under the TCJA, the CTC was $2,000 per child. In 2026, it has technically reverted to the pre-2018 level of $1,000 per child. Furthermore, the credit is once again subject to stricter refundability rules. Families must also remember that the Personal Exemption for children has returned, which may provide a larger “tax shield” than the $2,000 credit did for some high-income families who were previously phased out of the credit.

Does the Alternative Minimum Tax (AMT) affect more people in 2026?

Yes. The TCJA significantly increased the AMT exemption and phase-out thresholds, exempting most middle-class families. In 2026, those thresholds have technically reverted to much lower levels. This means that taxpayers with high itemized deductions or specific tax preferences (like ISO exercises) are much more likely to be triggered into the AMT calculation in 2026 than in previous years.

Should I update my Form W-4 for 2026?

Absolutely. Because the marginal rates have increased and the personal exemptions have returned, the “Withholding Tables” used by employers have been completely redesigned for 2026. If you do not update your W-4 to account for your new 2026 filing status and number of dependents, you risk a significant “Underpayment Penalty” or a massive, unexpected tax bill when you file your return in 2027.