The full implementation of the SAVE plan in 2026 has transformed student debt management, offering a critical interest subsidy that prevents balances from growing even when monthly payments are low.

The student loan landscape of 2026 has reached a state of technical maturity following the high-profile legal and legislative shifts of 2024 and 2025. The centerpiece of this new era is the SAVE (Saving on a Valuable Education) Plan, which has evolved from a contested proposal into the primary defensive tool for over 20 million American borrowers. In 2026, the pivot is no longer about simply “pausing” payments; it is about the sophisticated management of the Interest Subsidy, a mechanism that prevents the soul-crushing growth of loan balances that characterized previous decades.

For the 2026 borrower, the SAVE plan represents a fundamental shift in how education debt is serviced. Unlike the legacy Income-Driven Repayment (IDR) plans of the past—such as IBR or PAYE—SAVE is designed to decouple the principal balance from the interest accrual. This means that for the first time in the history of federal lending, a borrower’s balance technically cannot grow as long as they are enrolled in the plan and making their calculated monthly payments, even if those payments are $0.

This stabilization of the debt cycle has profound implications for 2026 household finances. By eliminating Negative Amortization—the process where unpaid interest is added to the principal—the SAVE plan allows borrowers to maintain their creditworthiness and “Debt-to-Income” (DTI) ratios at levels that make homeownership and other life milestones technically achievable. In 2026, student debt has transitioned from a permanent financial “leak” into a managed liability with a clear, algorithmically defined ceiling.

The “Interest Curative” Mechanism: Ending Negative Amortization

The most powerful technical feature of the 2026 SAVE plan is the 100% Interest Subsidy. In legacy plans, if your calculated monthly payment was $50 but your loans accrued $200 in interest, the remaining $150 was often added to your balance, causing the debt to snowball. Under the 2026 SAVE rules, if your payment doesn’t cover the monthly interest, the Department of Education technically “cures” the difference by waving it entirely. To leverage this “Interest Curative” mechanism, the 2026 borrower must follow a specific technical protocol:

- Verified Enrollment: Ensure that all eligible Direct Loans are consolidated and enrolled in the SAVE plan through the modernized StudentAid.gov portal.

- Monthly Payment Compliance: Even a $0 calculated payment technically counts as a “full payment” for interest subsidy purposes.

- Annual Recertification: Maintain an active income data link with the IRS to ensure the subsidy is applied continuously without technical lapses.

This subsidy effectively turns every student loan into a non-compounding debt for those whose incomes fall below specific thresholds. In 2026, this is the ultimate “arbitrage” for the borrower: while inflation may erode the real value of the original principal, the interest subsidy ensures that the nominal balance remains static. This technical design makes the SAVE plan the most efficient wealth-preservation tool currently available in the federal student loan ecosystem.

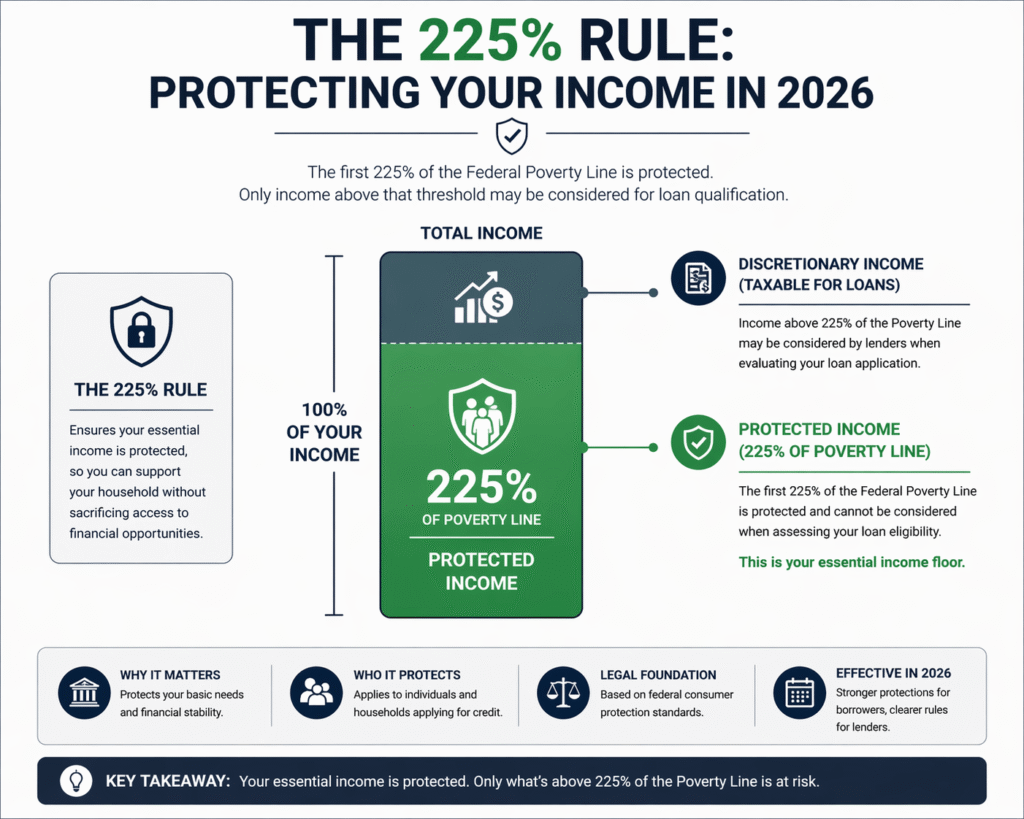

Calculating Discretionary Income in 2026: The 225% Rule

The calculation of your “Discretionary Income” is the technical engine that determines your monthly payment under SAVE. In 2026, the threshold for non-discretionary income has been locked at 225% of the Federal Poverty Guideline. This is a significant increase from the 150% used in previous plans, meaning that a much larger portion of a borrower’s income is technically “protected” from loan payments to cover basic necessities like housing and food.

For example, for a single borrower in 2026, the calculation works as follows: if the 2026 Poverty Guideline for an individual is approximately $16,000, then 225% of that amount is $36,000. If that individual earns $50,000 a year, their “Discretionary Income” is only $14,000 ($50,000 – $36,000). Their loan payment is then calculated as a percentage of that $14,000, rather than their total gross income.

The 5% vs. 10% Split: Optimization for Undergrad vs. Graduate Loans

In July 2024, a technical shift occurred that reached full operational status in 2026: the reduction of payment percentages for undergraduate loans. Under the SAVE plan, payments on undergraduate loans are capped at 5% of discretionary income, while graduate loans remain at 10%. For borrowers who have a “mixed portfolio”—meaning both undergraduate and graduate debt—the 2026 systems apply a weighted average based on the original principal balance of each loan type.

This split creates a strategic opportunity for 2026 borrowers to optimize their repayment. By understanding the weighted average, a professional can technically project their long-term cash flow with high precision. For instance, a borrower with a 70/30 split between undergraduate and graduate loans will pay a blended rate of roughly 6.5%. This technical granularity is essential for 2026 financial planning, as it allows for the precise allocation of “surplus capital” toward other high-yield investments or emergency reserves.

Furthermore, the 2026 system is now fully automated in distinguishing between these loan types. Borrowers no longer need to manually calculate their blended rates; the 2026 servicer platforms provide a “Payment Transparency Dashboard” that shows exactly how the 5% and 10% rules are being applied. This level of technical clarity ensures that borrowers aren’t overpaying and that they are receiving the maximum benefit of the reduced undergraduate rates.

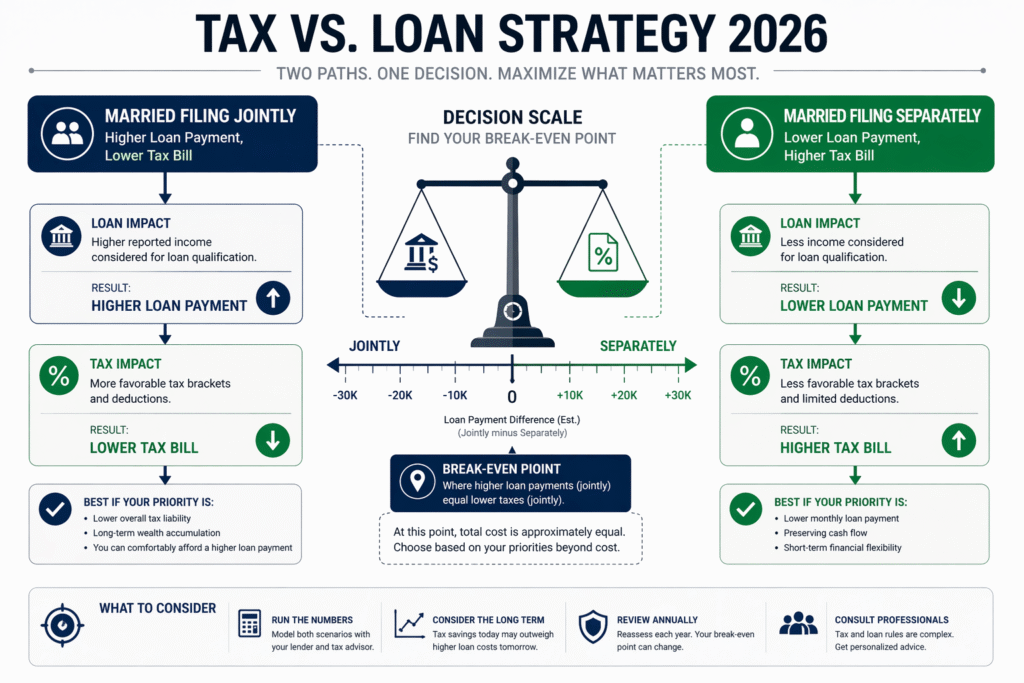

Strategic Tax Filing: Married Filing Separately in 2026

For married borrowers, the SAVE plan has introduced a vital technical loophole regarding tax filing. Unlike some older plans, SAVE allows married couples to file “Married Filing Separately” (MFS) to exclude their spouse’s income from the payment calculation. In 2026, this is a primary strategy for dual-income households where one spouse has significantly higher earnings and lower student debt.

However, this strategy requires a technical “Break-Even Analysis.” Filing separately often results in the loss of certain tax credits and a higher overall tax liability. The 2026 professional must calculate whether the monthly “Student Loan Savings” from a lower payment outweighs the “Tax Penalty” of filing separately. This “Tax-Loan Optimization” is a hallmark of 2026 financial intelligence, requiring a coordinated view of both the IRS and the Department of Education’s rules.

| Feature | SAVE Plan (2026 Standard) | PAYE (Legacy) | IBR (Legacy) |

| Discretionary Income Base | 225% of Poverty Line | 150% of Poverty Line | 150% of Poverty Line |

| Payment % (Undergrad) | 5% | 10% | 10% – 15% |

| Interest Subsidy | 100% of Unpaid Interest | Partial / Time-Limited | Limited |

| MFS Exclusion | Yes | Yes | Yes |

| Negative Amortization | Technically Eliminated | Possible | Possible |

FAQ: Navigating the 2026 Student Loan Landscape

What happens if my income changes mid-year in 2026?

The 2026 system allows for “Instant Recertification.” If you experience a job loss or a significant income drop, you can technically submit a “Self-Certification” of your new income on StudentAid.gov. The system will update your payment within one billing cycle, ensuring that your cash flow is protected immediately rather than waiting for your next tax return.

Does the SAVE plan impact my ability to get a mortgage in 2026?

Yes, but positively. Because the SAVE plan often results in a significantly lower monthly payment than other plans, your Debt-to-Income (DTI) ratio is technically improved. Most 2026 mortgage lenders (including FHA and Fannie Mae) use the actual monthly payment on your credit report for qualification purposes. If your SAVE payment is $0, it is technically treated as $0 for your DTI, increasing your purchasing power.

Is there a “Tax Bomb” on forgiven debt in 2026?

As of early 2026, federal student loan forgiveness remains tax-free at the federal level due to the extension of the American Rescue Plan provisions. However, some states may still technically treat forgiven debt as taxable income. Borrowers should consult with a 2026 tax professional to determine their specific state-level liability before reaching the 20- or 25-year forgiveness mark.

How does the “Low-Balance Forgiveness” work in 2026?

The SAVE plan includes a “Fast-Track” for low-balance borrowers. If your original principal balance was $12,000 or less, your remaining debt is technically forgiven after just 10 years of payments. For every $1,000 above that, one additional year is added. In 2026, many community college graduates are seeing their balances hit $0 automatically through this technical provision.

Can I consolidate my old FFELP (commercial) loans into SAVE in 2026?

By 2026, most FFELP loans must have been consolidated into the Federal Direct Loan program to be eligible for SAVE. If you haven’t done this yet, you should perform a “Consolidation Audit” immediately. While the 2024 “One-Time Account Adjustment” deadline has passed, consolidation still opens the door to the SAVE plan’s superior interest subsidy and lower payment percentages.

Does the 2026 SAVE plan cover Parent PLUS loans?

Technically, no. Parent PLUS loans are not directly eligible for the SAVE plan. However, some 2026 borrowers utilize the “Double Consolidation” loophole (if completed before the 2025 sunset) to move Parent PLUS debt into a Direct Consolidation Loan that is eligible. If you missed this window, your Parent PLUS loans are likely restricted to the less-favorable Income-Contingent Repayment (ICR) plan.