The Corporate Transparency Act (CTA) has reached a critical evolutionary milestone in 2026, transitioning from a nascent regulatory requirement into a fully enforced pillar of the United States’ anti-money laundering framework. As the Financial Crimes Enforcement Network (FinCEN) intensifies its oversight, small business owners and estate planners find themselves navigating a high-stakes reporting environment where technical errors can result in significant civil and criminal liabilities. The primary objective of the CTA remains the collection of Beneficial Ownership Information (BOI) to combat illicit financial activities, but for the average LLC or corporation, the challenge lies in the precise identification of who truly exerts “substantial control” over the entity.

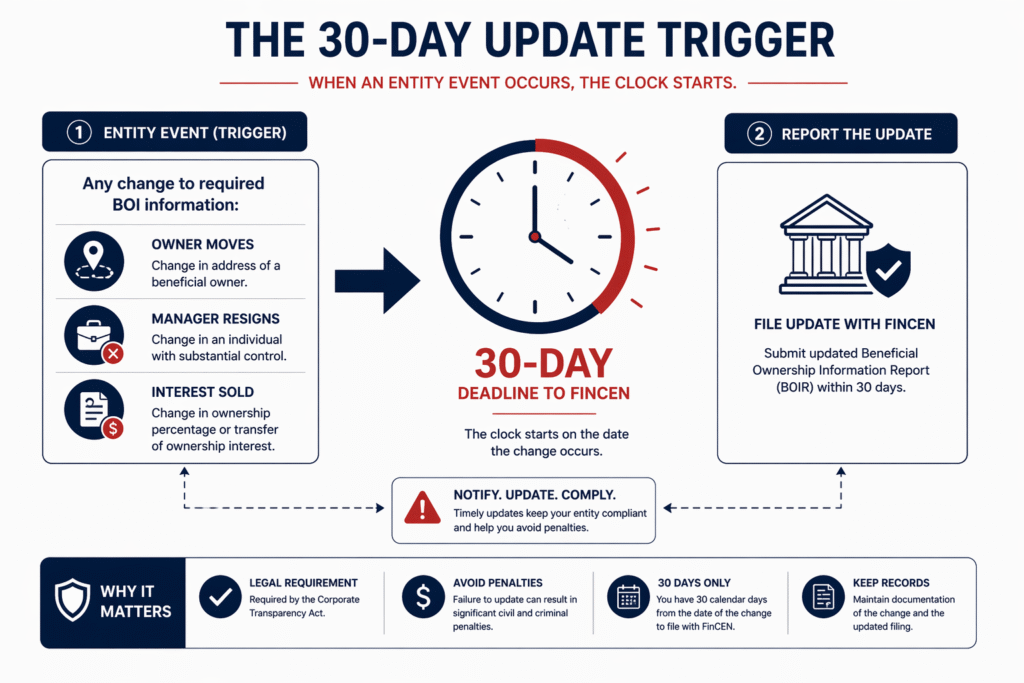

By 2026, the initial “grace period” for legacy entities has long expired, and the focus has shifted toward the continuous monitoring of entity structures. Any change in beneficial ownership, including address updates or changes in senior leadership, now triggers a mandatory 30-day reporting window. This requirement necessitates a robust internal compliance protocol, as the traditional “set it and forget it” approach to corporate filings is no longer legally viable. Consequently, the technical management of BOI data has become a standard component of modern financial hygiene, requiring a granular understanding of how various ownership interests are aggregated and reported.

The 2026 landscape is also defined by the integration of BOI data with other federal and state databases, creating a transparent digital nexus for regulatory bodies. This interconnectivity means that discrepancies between tax filings, state-level annual reports, and FinCEN submissions are more likely to be flagged for audit. For serial entrepreneurs and investors with complex portfolios, the technical burden of maintaining accurate records across multiple entities is immense. Achieving regulatory alignment in this environment requires not only legal precision but also a strategic approach to data management that ensures consistency across all corporate disclosures.

Deciphering “Beneficial Ownership” in Complex Multi-Tiered Structures

The technical core of the CTA lies in its broad and nuanced definition of a Beneficial Owner. An individual is classified as such if they either exercise substantial control over the reporting company or own/control at least 25% of the ownership interests. In 2026, FinCEN has clarified that “substantial control” transcends formal job titles; it encompasses anyone who can direct, determine, or have substantial influence over important decisions. This includes “shadow directors” and certain high-level consultants who may not appear on the official cap table but exert significant operational or financial leverage.

For multi-tiered structures involving holding companies, trusts, and subsidiaries, the identification process requires a “look-through” analysis to find the natural persons at the end of the chain. If an LLC is owned by another LLC, the reporter must keep ascending the hierarchy until they identify the individuals who ultimately hold the power. This is particularly complex in the context of irrevocable trusts, where the beneficial owner might be the trustee, the beneficiaries, or even the grantor, depending on the specific powers of appointment and control mechanisms established in the trust indenture.

In the 2026 regulatory environment, the determination of beneficial ownership is not a one-time event but a functional analysis that must be re-evaluated whenever there is a shift in the entity’s governance or voting power.

Navigating these complexities requires a forensic review of operating agreements, bylaws, and shareholder pacts. In many cases, individuals with “veto power” over major corporate actions are deemed to have substantial control, even if their equity stake is negligible. This focus on de facto control ensures that the BOI database remains a true reflection of the power dynamics within the American corporate ecosystem, leaving no room for the “anonymity layers” that characterized previous decades of corporate law.

Filing Deadlines and the “Change in Information” Trigger

In 2026, the strictness of the 30-day reporting window for updates is the most frequent source of non-compliance. Unlike the initial filing, which had a longer lead time, any subsequent change to a beneficial owner’s name, residential address, or the identifying number from their passport or driver’s license must be reported within 30 days of the change. This creates a significant administrative overhead for companies with numerous owners. To understand the current filing standards, the following table contrasts the 2026 requirements with common exemptions:

| Reporting Category | Requirement Status | Deadline for 2026 | Key Technical Exception |

| New Entities (Formed in 2026) | Mandatory | 30 Days from Formation | Publicly Traded Companies |

| Address/Name Changes | Mandatory Update | 30 Days from Event | N/A (Always Required) |

| Transfer of Ownership | Mandatory Update | 30 Days from Close | Exempt Non-Profit Entities |

| Large Operating Companies | Exempt | N/A | >20 FTEs & >$5M Revenue |

The “Large Operating Company” exemption is a technical “safe harbor” that remains highly relevant in 2026. However, if a company’s revenue falls below the $5 million threshold (as reported on the prior year’s tax return) or if its full-time equivalent (FTE) count drops below 21, the exemption is lost, and the entity must file its BOI report within 30 days. This makes financial monitoring a critical component of CTA compliance; a single bad quarter that leads to layoffs could inadvertently trigger a federal reporting obligation that, if missed, carries penalties of up to $500 per day.

Furthermore, the “Company Applicant” rule continues to apply to all entities formed after January 1, 2024. The person who physically files the formation documents and the person primarily responsible for directing the filing must both be identified. While the information for company applicants does not need to be updated after the initial filing, the accuracy of the initial data set is paramount, as errors in the applicant’s record can invalidate the entire filing and flag the entity for further scrutiny by FinCEN’s automated compliance algorithms.

FinCEN Identifiers: Technical Advantages for Serial Entrepreneurs

For individuals who serve as beneficial owners for multiple entities, the FinCEN Identifier (FinCEN ID) has become an indispensable technical tool in 2026. A FinCEN ID is a unique number issued to an individual who provides their BOI directly to the agency. Once obtained, the individual can provide their FinCEN ID to the reporting companies in lieu of their sensitive personal documents (e.g., a copy of their passport). This drastically reduces the risk of identity theft and simplifies the administrative burden of managing multiple filings.

The strategic advantage of the FinCEN ID lies in its centralized update mechanism. If a beneficial owner moves to a new house, they only need to update their information once through the FinCEN portal using their ID. This update then automatically propagates across every entity that uses their identifier in its BOI report. In 2026, this “single point of truth” approach is the gold standard for serial entrepreneurs and high-net-worth individuals who may be associated with dozens of LLCs or special purpose vehicles (SPVs).

Moreover, the FinCEN ID facilitates a “Clean Data” environment for the reporting company. By using identifiers, the company avoids the liability of storing the Personally Identifiable Information (PII) of its owners locally. This is a critical consideration for data privacy compliance, as the unauthorized disclosure of an owner’s passport or driver’s license could trigger state-level data breach notification laws. Utilizing the FinCEN ID effectively shifts the primary data security burden back to the federal government, which maintains a high-security, encrypted environment for BOI storage.

Data Security and Privacy Concerns in the BOI E-Filing System

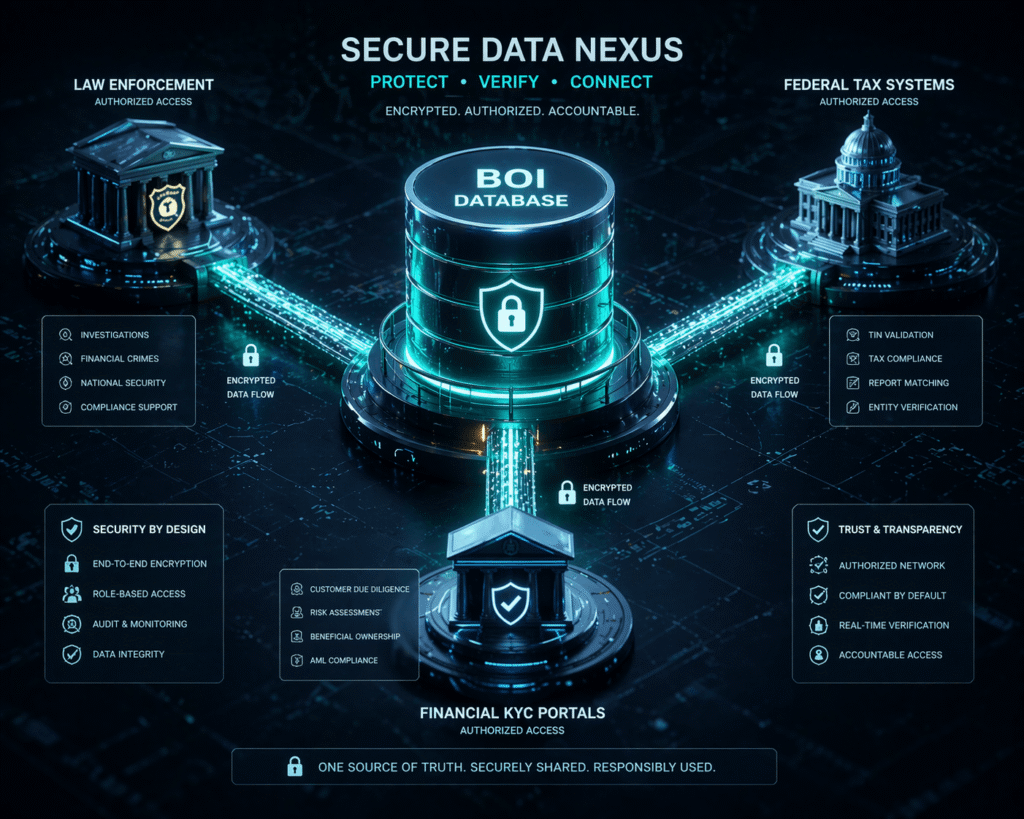

As the volume of data in the BOI database has surged, so too have concerns regarding cybersecurity and data sovereignty. In 2026, the FinCEN E-Filing system utilizes a “Multi-Layered Encryption” architecture, but the vulnerability often lies at the point of entry—the small business owner’s computer. The rise of CTA-themed phishing attacks has forced FinCEN to issue frequent warnings. These scams often mimic “official” federal notices to trick owners into revealing their sensitive data. A technical audit of one’s filing process is now a mandatory step in the compliance lifecycle.

Access to the BOI database is strictly controlled and limited to authorized government agencies, law enforcement, and, in certain circumstances, financial institutions with the consent of the reporting company. In 2026, the “consent protocol” for banks has become a standard part of the Know Your Customer (KYC) process. When a business opens a new account, the bank will often request permission to access the BOI database to verify the ownership structure. This inter-agency data sharing ensures that the information provided to FinCEN is consistent with the information provided to private financial institutions.

To ensure a robust and secure compliance posture, business owners should follow a standardized BOI Compliance Audit Checklist in 2026:

- Entity Status Verification: Confirm if the entity is active, dissolved, or qualifies for any of the 23 specific exemptions.

- Beneficial Owner Identification: Map all individuals with >25% equity or “Substantial Control” (including silent partners).

- Document Integrity: Ensure that the identifying documents (passports/licenses) are current and not expired.

- FinCEN ID Reconciliation: Verify that all identifiers used are active and that the linked personal information is up to date.

- Filing Receipt Archival: Maintain a permanent, encrypted record of the “Transcript of Filing” for each submission.

FAQ: Corporate Transparency and Regulatory Compliance

What are the consequences of “Willful Non-Compliance” with BOI reporting in 2026?

The penalties are severe and are designed to deter intentional evasion. Under the CTA, providing false information or failing to report can lead to civil penalties of up to $500 per day for each day the violation continues. More significantly, criminal penalties can include fines of up to $10,000 and imprisonment for up to two years. In 2026, FinCEN has demonstrated a willingness to prosecute “enablers”—professionals who knowingly assist clients in filing fraudulent BOI reports—underscoring the need for absolute technical accuracy.

Does a “Dissolved LLC” still have a reporting obligation if it was active for part of 2026?

This is a nuanced “edge case.” If an entity was dissolved before its filing deadline, it generally does not have a reporting obligation. However, if a company existed for a single day in 2026 and then dissolved, and it had not previously met its filing requirements, it may still technically be required to file a “final” BOI report. Because the CTA looks at the “existence” of the entity, the safest technical approach in 2026 is to file the BOI report simultaneously with the state-level dissolution papers to ensure no “regulatory gap” exists.

How is the “Ownership Interest” calculated for individuals with stock options or convertible debt?

In 2026, FinCEN uses an “as-converted” basis for calculating the 25% threshold. This means that any options, warrants, or convertible notes are treated as if they had been exercised. If the exercise of those instruments would push an individual over the 25% mark, they must be reported as a beneficial owner. This requires a sophisticated “Pro-Forma” cap table analysis for startups and venture-backed companies, where potential ownership is as legally relevant as current equity.

Can an “Acting Manager” be considered a Beneficial Owner even if they have no equity stake?

Yes, under the “Substantial Control” prong. A manager who has the authority to enter into significant contracts, hire or fire senior officers, or direct the strategic direction of the company is a beneficial owner. In many small LLCs, the “Manager-Managed” structure means the manager is the only person with substantial control, even if the “Members” (owners) hold all the equity. In 2026, failure to report a non-equity manager is a high-frequency audit trigger.