The financial landscape of 2026 has officially closed the curtain on the era of “ghost debt.” For years, Buy Now, Pay Later (BNPL) operated in a regulatory grey zone, allowing consumers to leverage short-term, interest-free installments without these obligations appearing on their formal credit reports. However, by mid-2026, the maturation of the industry and the finalized implementation of federal oversight have integrated BNPL into the core of the American credit ecosystem. What was once a “hidden” financial tool is now a primary data point for lenders, requiring a new level of technical discipline from the modern consumer.

This integration is the result of a coordinated effort between the Consumer Financial Protection Bureau (CFPB) and the three major credit bureaus. In 2026, BNPL is no longer treated as an alternative to credit; it is technically recognized as a specific form of revolving or installment debt, depending on the provider’s structure. This shift ensures that the $100+ billion in annual BNPL volume is now visible, providing a more accurate—and sometimes more challenging—picture of a household’s total financial leverage.

For the 2026 professional, the stakes of a “Pay-in-4” plan have been significantly raised. A missed payment on a $50 pair of sneakers now carries the same technical weight as a missed credit card payment, directly impacting the FICO 10T scores. As transparency becomes the default, the strategic use of BNPL has transitioned from a simple convenience to a sophisticated exercise in Credit Reputation Management, where every small transaction contributes to the consumer’s longitudinal trended data.

The CFPB Mandate: BNPL as Credit Cards

In a landmark move that reached full enforcement in early 2026, the CFPB officially mandated that BNPL providers must comply with the same fundamental consumer protection rules as traditional credit card issuers. This reclassification technically subjects providers to Regulation Z, ensuring that the “wild west” days of opaque fee structures and limited dispute rights are over. For the consumer, this means that the technical safeguards they expect from a high-tier Visa or Mastercard are now legally required for every Klarna, Affirm, or Afterpay transaction.

This regulatory umbrella provides a level of technical “Dispute Sovereignty” that was previously unavailable. In the early 2020s, resolving a failed delivery or a defective product bought via BNPL was often a bureaucratic nightmare, with providers frequently pointing fingers at merchants. In 2026, the provider is technically liable for ensuring that billing errors are corrected and that consumers have a clear, standardized path to contest charges. This has standardized the “User Experience of Debt,” making it safer but more structurally rigid.

To ensure compliance with the 2026 standards, providers have introduced the following four technical rights for all users:

- Standardized Disclosures: Clear, up-front listing of any late fees or “missed payment” penalties in a format identical to credit card Schumer boxes.

- Refund Sovereignty: The right to a prompt refund when a merchant fails to deliver, with the BNPL provider acting as the primary point of contact.

- Dispute Transparency: A mandated 60-day window for consumers to challenge billing errors, with the provider required to acknowledge and investigate within strict technical timelines.

- Billing Rights Statements: Periodic statements that clearly outline the total balance, upcoming installments, and the “True Cost of Capital” if any interest is applied.

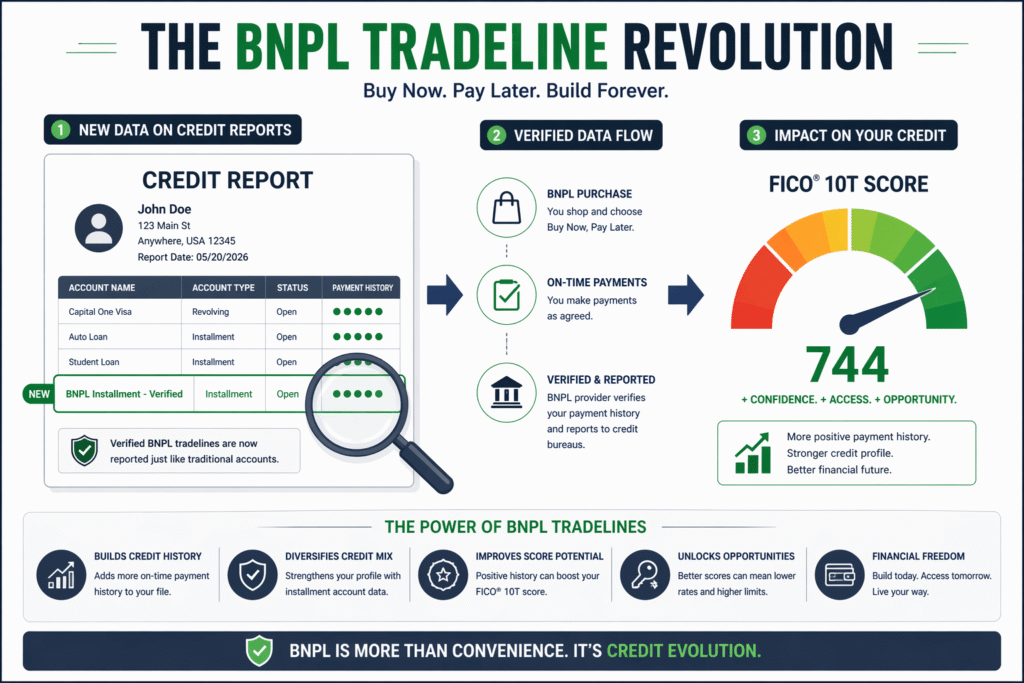

Reporting to the Big Three: The “Tradeline” Revolution

The most significant technical shift in 2026 is the ubiquitous reporting of BNPL “Tradelines” to Equifax, Experian, and TransUnion. Unlike the sporadic reporting of the past, 2026 regulations have standardized how these short-term loans are ingested by the bureaus. BNPL accounts now appear as distinct line items, contributing to the consumer’s total “Credit Velocity” and “Account Age.” This visibility has technically eliminated the “DTI Blind Spot” that previously allowed over-leveraged consumers to appear creditworthy.

This reporting revolution has a dual-edged impact on the 2026 score. For the “Thin-File” borrower, a series of successfully completed BNPL plans acts as a powerful Credit Accelerator, proving their technical ability to manage debt without the need for a traditional $5,000 limit credit card. However, for the established borrower, the sudden appearance of multiple new BNPL tradelines can technically lower their “Average Age of Accounts,” potentially causing a temporary dip in their FICO score just as they are preparing for a major loan application.

In 2026, the invisibility of BNPL has been replaced by absolute transparency; your “hidden” installments are now a matter of public record, serving as either a ladder for your score or a weight on your financial reputation.

Optimization Strategy: Managing BNPL for Score Growth

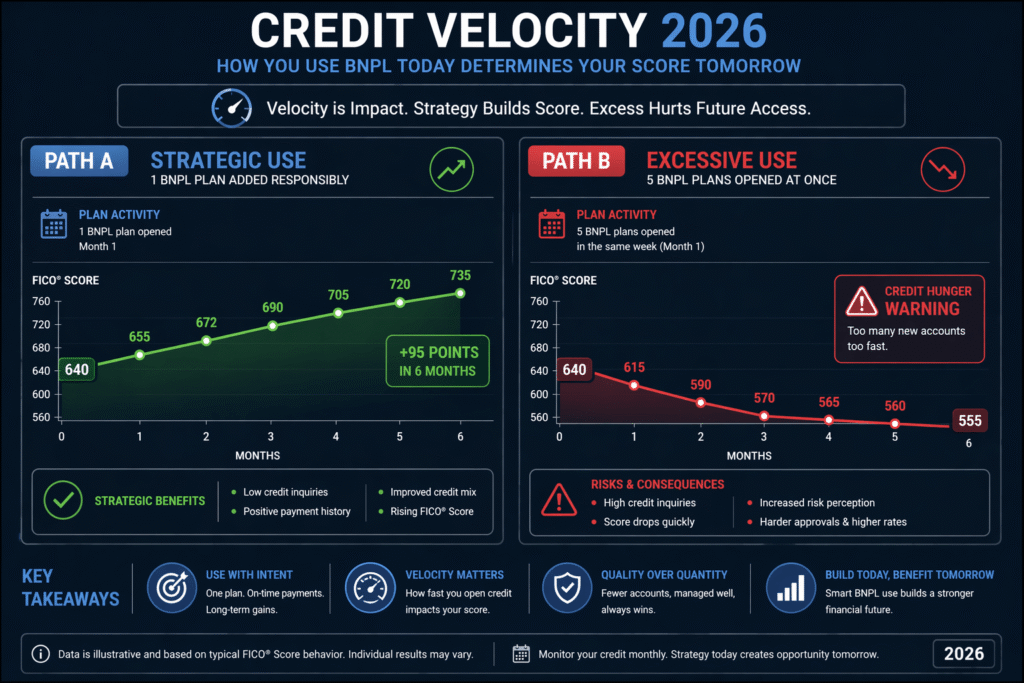

Success in the 2026 credit market requires the Strategic Throttling of BNPL use. Because these loans are now reported, the “velocity” of opening multiple accounts in a short period is technically flagged by AI-driven scoring models as a sign of financial strain. The 2026 professional should treat each BNPL application as a “Soft-Hard Hybrid” event—while it may not always trigger a hard inquiry, the new tradeline will undeniably impact the “Account Opening Trend” that FICO 10T monitors over a 24-month window.

To optimize for growth, consumers should use BNPL for “Strategic Gap-Filling” rather than everyday consumption. Utilizing a single BNPL provider consistently is technically superior to jumping between four different apps, as it maintains a more stable and predictable tradeline on the report. In 2026, the “Loyalty Bonus” is real: many providers now offer higher limits and lower “Synthetic Interest” to users who demonstrate a multi-year history of on-time installments, which in turn strengthens the user’s credit profile.

Furthermore, 2026 consumers must be aware of the “Utilization Lag.” Because BNPL loans often close quickly (usually in 6 to 8 weeks), the time it takes for the bureau to update the “Paid in Full” status can sometimes overlap with new purchases. This can technically create a “Ghost Utilization” spike, where it appears you owe more than you actually do on the day a lender pulls your report. The technical advice for 2026 is to pause all BNPL activity 60 days before applying for a mortgage or auto loan to ensure the “Credit Dust” has settled.

The “Phantom” DTI: Why Lenders are Scrutinizing BNPL

For 2026 mortgage and auto lenders, the inclusion of BNPL in the credit report has solved the “Phantom DTI” (Debt-to-Income) problem. Previously, a borrower might have had $800 in monthly BNPL installments that never appeared in their DTI calculation, leading to higher default risks. In 2026, underwriters use Automated Debt Analyzers that pull every BNPL obligation into the DTI formula, ensuring that the “Real-Time Cash Flow” of the borrower is fully understood before a single dollar is lent.

This scrutiny has made BNPL a “High-Signal” metric for financial stability. A borrower with 10 active BNPL plans is technically viewed as a higher risk in 2026 than a borrower with a single, high-limit credit card, as it suggests a lack of liquidity for mid-sized purchases. The technical shift from 2024 to 2026 has moved BNPL from a “shopping hack” to a “financial health indicator” that is as scrutinized as any traditional bank statement.

| Feature | BNPL 2024 (Legacy) | BNPL 2026 (Regulated) |

| Credit Reporting | Sporadic / Optional | Standardized Tradelines |

| Consumer Rights | Merchant-dependent | Full Regulation Z Protections |

| Scoring Impact | Minimal / Invisible | Direct FICO 10T / Vantage Factor |

| DTI Visibility | “Phantom” (Hidden) | Fully Integrated / Transparent |

| Late Fees | Variable / Opaque | Capped and Disclosed |

FAQ: Mastering the New BNPL Rules

Does every BNPL purchase trigger a hard credit pull in 2026?

Most 2026 providers still utilize a “Soft-Inquiry” for initial approval to protect your score. However, once the plan is accepted, the “New Account” is technically reported as a tradeline. This means while the application doesn’t hurt your score, the existence of the new debt will be visible and factored into your credit trend.

Can I use BNPL to “Fix” a low credit score in 2026?

Yes. BNPL is one of the most effective “Credit Rehabilitation” tools in 2026. Because it has a lower barrier to entry than a premium credit card, completing “Pay-in-4” plans on time creates a consistent history of positive installments. For those with a “Thin-File,” this is the technically fastest way to build a reliable credit foundation.

What happens to my 2026 score if I return an item bought with BNPL?

Technically, the “Tradeline” will show as “Closed – Paid” once the merchant processes the return and the provider zeros the balance. However, if the merchant takes 30 days to process the return and you miss a payment in the meantime, your score will be dinged. In 2026, you must continue making payments until the return is technically verified by the provider to protect your score.

Is there a limit to how many BNPL plans I should have open?

The 2026 technical benchmark for “Credit Health” is no more than two concurrent plans. Beyond this, scoring algorithms may flag your profile for “Credit Hunger” or “Financial Instability.” If you find yourself needing four or five BNPL plans to manage cash flow, it is a technical signal that your primary liquidity is insufficient, which will be reflected in your FICO 10T trend.

Can BNPL be used for Business-to-Business (B2B) purchases in 2026?

Yes, “B2B-BNPL” has exploded in 2026. Small business owners use it to manage inventory cash flow. These plans are technically reported to business credit bureaus like Dun & Bradstreet, helping startups build an “Entity Credit Score” without personal guarantees, provided they use specialized business-BNPL platforms.

How do I “Consolidate” BNPL debt in 2026?

If you have multiple BNPL installments causing “Context-Drag” on your finances, many 2026 banks now offer “BNPL Consolidation Loans.” These take all your scattered installments and turn them into a single, fixed-rate personal loan. Technically, this improves your score by replacing several “New Accounts” with one “Installment Loan,” which is viewed more favorably by 2026 algorithms.