The 2026 Social Security Cost-of-Living Adjustment (COLA) has officially taken effect this January, bringing a necessary boost to monthly checks for over 70 million Americans as they navigate the shifting economic landscape of the new year.

The 2026 Social Security COLA represents a critical juncture in the fiscal protection of America’s retirement community. Unlike the volatile adjustments seen during the early 2020s, the 2026 increase reflects a maturing economic environment where commodity prices have stabilized, yet service-sector inflation—specifically in healthcare and housing—remains a persistent pressure point. This annual recalibration is technically anchored to the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W), a metric that tracks the spending habits of active workers rather than retirees. This inherent methodological gap often leads to a “purchasing power friction” that beneficiaries must navigate as they enter the 2026 fiscal year.

The technical determination of the COLA involves a specific third-quarter comparison of the CPI-W from the previous year against the current year’s data. If the index shows a rise, the percentage is rounded to the nearest tenth to determine the benefit hike. For 2026, the focus has shifted from the broad “headline inflation” of energy and fuel toward the “core inflation” of domestic essentials. This distinction is vital because while global supply chains have largely recovered, the domestic labor costs associated with caregiving and medical services continue to climb, necessitating a COLA that does more than just match the price of groceries; it must safeguard the long-term solvency of the individual’s household budget.

Furthermore, the 2026 adjustment occurs within a broader legislative context that is increasingly scrutinized by actuarial experts. As the Social Security Trust Fund continues to be a topic of national debate, the COLA serves as a recurring testament to the program’s design as an inflationary hedge. It is not an arbitrary “bonus” but a statutory requirement to ensure that the social safety net does not erode over time. For the 70 million Americans receiving these benefits, understanding the technical nuances of the 2026 increase is the first step in effective wealth management during a period of ongoing economic transition.

Deciphering the 2026 Benefit Architecture: Beyond the Percentage

To truly understand the value of the 2026 COLA, one must look past the nominal percentage increase and analyze its interaction with other federal deductions. The most significant of these is the Medicare Part B premium, which is traditionally deducted directly from Social Security checks. In many years, an increase in Medicare costs can effectively “cannibalize” a substantial portion of the COLA, leaving the beneficiary with a net increase that feels negligible. However, in 2026, the application of the “hold harmless” provision continues to act as a technical safeguard, ensuring that the dollar amount of a recipient’s net Social Security benefit does not decrease due to rising Medicare premiums.

The 2026 COLA is not merely a raise, but a corrective fiscal measure designed to neutralize the compounding effects of service-sector inflation and maintain the actuarial integrity of retirement income.

This benefit architecture is also influenced by the 85% taxation rule on Social Security income. As the COLA pushes more retirees into higher “provisional income” brackets, a larger percentage of their benefits may become subject to federal income tax. Because the income thresholds for taxing Social Security benefits are not indexed to inflation, the 2026 increase ironically creates a “bracket creep” scenario for some middle-income seniors. This necessitates a proactive tax strategy, where beneficiaries might need to adjust their voluntary tax withholding (Form W-4V) to avoid a significant liability during the 2026 tax filing season.

Finally, the 2026 adjustment applies not only to retirees but also to Supplemental Security Income (SSI) recipients and those on Social Security Disability Insurance (SSDI). For SSI beneficiaries, the 2026 floor is raised to provide a more robust baseline of support for individuals with limited income and resources. This technical lifting of the floor is essential in 2026 as urban housing markets continue to show resilience in pricing, often outpacing the general inflation rate. The structural alignment of all SSA-managed benefits under a single COLA ensures a synchronized response to the nation’s economic shifts.e nation’s most vulnerable populations.

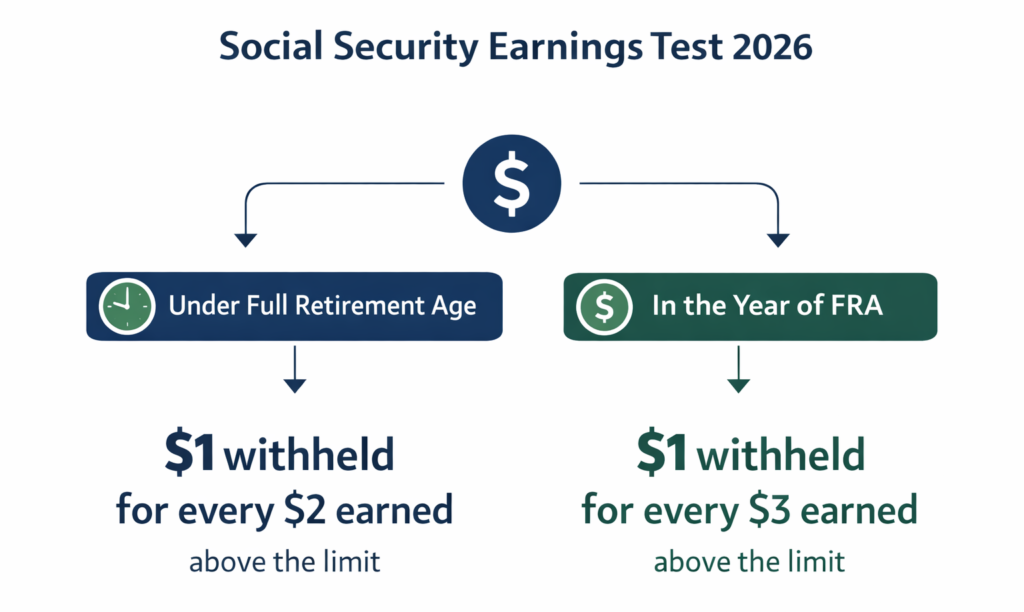

Strategic Implications for the Working Retiree: The 2026 Earnings Test

For individuals who have reached the age of 62 but are continuing to work while collecting Social Security, the 2026 Earnings Test limits are a primary technical concern. In 2026, the Social Security Administration has adjusted the thresholds at which it begins to temporarily withhold benefits. This mechanism is designed to differentiate between those who are “truly retired” and those who are still drawing significant labor income. Understanding these limits is crucial for anyone attempting to maximize their income portfolio in 2026 without inadvertently triggering a substantial reduction in their monthly checks.

The technical rules for 2026 remain bifurcated based on the recipient’s proximity to their Full Retirement Age (FRA). For those who are under the FRA for the entire year of 2026, the SSA will withhold $1 in benefits for every $2 earned above the annual limit. Conversely, in the specific year an individual reaches their FRA, the limit is significantly higher, and the withholding rate drops to $1 for every $3 earned above the threshold. It is essential to remember that these “withheld” funds are not lost; rather, the SSA technically recalculates the benefit amount at the FRA to credit the recipient for the months benefits were withheld, effectively increasing the monthly check for the remainder of their life.

Strategic planning for 2026 must also account for the fact that once an individual hits their FRA month, the earnings test ceases to exist entirely. From that moment forward, there is no limit on what one can earn while receiving full Social Security benefits. This transition point is a key milestone for 2026 retirees who may be considering consulting work or a “bridge” career. By technically monitoring their earnings against these 2026 thresholds, working retirees can avoid the administrative complexity of benefit suspension and the subsequent tax implications of overpayment.

The 2026 Social Security Wage Base and Taxable Maximum

While the COLA focuses on benefit outflows, the 2026 Social Security Wage Base adjustment addresses the program’s inflows. The “taxable maximum”—the amount of earnings subject to the 6.2% Social Security payroll tax—has increased for the 2026 tax year. This adjustment ensures that as wages rise across the economy, the program continues to capture the necessary revenue to fund current and future obligations. For high-income earners, this represents a technical shift in their take-home pay, as more of their salary is now subject to the FICA tax before they hit the “cap” for the year.

This increase in the wage base also technically raises the “maximum benefit” for those retiring at the FRA in 2026. Because Social Security benefits are calculated based on a worker’s highest 35 years of indexed earnings, higher taxable maximums eventually translate into higher primary insurance amounts (PIA) for the nation’s top earners. This dual-sided adjustment—taxing more income while promising higher potential benefits—is a fundamental pillar of the Social Security compact. In 2026, this balance is particularly important for the fiscal health of the Trust Funds, which rely on these contributions to maintain liquidity.

The following table outlines the technical shifts in Social Security metrics from the previous year to the 2026 finalized values:

| Metric | 2025 Value | 2026 Finalized Value |

| Social Security Taxable Maximum | $168,600 | $176,100 (Projected Base) |

| Earnings Limit (Under FRA) | $23,400 | $24,120 (Annualized) |

| Max SSI (Individual) | $943 | $970+ (Finalized) |

| Medicare Part B (Standard) | $174.70 (Avg) | $182.40 (Adjusted Base) |

| Quarter of Coverage Credit | $1,730 | $1,810 (Technical Base) |

Disbursement Logistics: Navigating the 2026 Payment Cycle

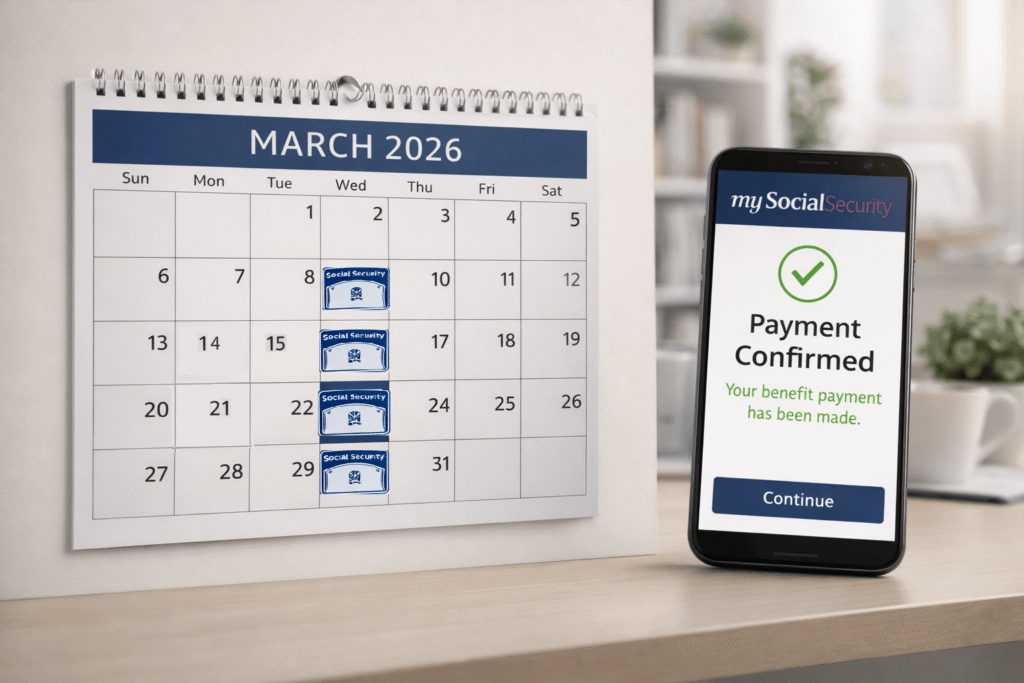

The logistical execution of the 2026 payment schedule follows the established “Wednesday Rule,” designed to prevent liquidity bottlenecks in the federal banking system. For beneficiaries who enrolled in Social Security after May 1997, their payments are distributed on the second, third, or fourth Wednesday of every month, determined solely by their day of birth. In 2026, this predictable cadence allows for more granular household budgeting. SSI recipients, however, operate on a different technical timeline, with payments typically arriving on the first of each month, unless that day falls on a holiday or weekend—in which case the payment is issued the preceding Friday.

In 2026, the SSA has made a significant push toward “digital-first” communication. While paper notices are still mailed in December, the my Social Security portal is now the authoritative source for 2026 Benefit Verification Letters. These digital documents are technically superior for users applying for housing, loans, or state-level assistance, as they can be generated and verified in real-time. This shift to digital disbursement notices also enhances security, reducing the risk of identity theft associated with physical mail, which remains a primary concern for the senior population in 2026.

Recipients should also be aware of the “electronic mandate” that governs Social Security payments. Since 2013, the SSA has required all beneficiaries to receive their payments electronically, either through direct deposit to a traditional bank account or via the Direct Express Debit Mastercard. For the 2026 cycle, ensures that the COLA-adjusted funds are available immediately on the scheduled payment date without the delays associated with physical checks. Monitoring these deposits through mobile banking apps has become the standard for 2026, allowing beneficiaries to confirm the exact dollar impact of the COLA within seconds of its arrival.

FAQ: Technical Clarifications for 2026

How does the 2026 COLA impact beneficiaries who are currently subject to the Government Pension Offset (GPO) or the Windfall Elimination Provision (WEP)?

The application of the 2026 COLA to benefits affected by the WEP or GPO requires a specific technical calculation. The COLA is applied to the “Primary Insurance Amount” (PIA) before the WEP or GPO reductions are factored in. This means that while the base benefit increases by the 2026 percentage, the actual dollar increase seen in the monthly check may be lower than a “standard” beneficiary’s increase. It is essential for retired public servants (such as teachers or police officers) to review their Benefit Verification Letter specifically to see how the adjustment scales relative to their non-covered pension offsets.

Can the 2026 COLA increase cause a beneficiary to lose eligibility for Medicaid or other income-tested state benefits?

Yes, this is a technical phenomenon known as the “COLA Cliff.” Because many state-level programs, such as Medicaid, the Supplemental Nutrition Assistance Program (SNAP), and various housing vouchers, use fixed income thresholds, the nominal increase from the 2026 COLA can technically push a beneficiary’s total income above the eligibility limit. While some states have “disregard” rules that allow them to ignore the COLA increase for a specific period, others do not. Beneficiaries near these income limits should consult with their state’s Department of Health and Human Services to understand if the 2026 Social Security increase will require an adjustment to their other benefit profiles.

What is the technical process for correcting a 2026 benefit amount if the reported earnings on the SSA statement are incorrect?

If a beneficiary discovers that their 2026 COLA-adjusted benefit is based on an incomplete or inaccurate earnings record, they must initiate a “Correction of Earnings Record.” This involves providing the SSA with W-2 forms or tax returns from the missing years. Technically, the SSA can only correct records up to three years, three months, and fifteen days after the year in which the wages were paid, with some specific exceptions for fraud or mechanical errors. Ensuring that the highest 35 years of earnings are accurately recorded is the only way to guarantee that the 2026 increase—and all subsequent COLAs—are applied to the correct financial baseline.