The legal framework surrounding Paid Family and Medical Leave (PFML) in the United States has reached a point of unprecedented complexity in 2026. As more states transition from traditional unpaid leave models to robust, payroll-funded social insurance programs, the jurisdictional overlap creates a challenging environment for both beneficiaries and administrators. This evolution is driven by a recognition that economic stability is inextricably linked to the ability of the workforce to manage health crises and caregiving responsibilities without total income loss. Consequently, understanding the nuanced differences between state-level statutory requirements and broader federal guidelines is no longer optional for those seeking to maximize their available benefits while ensuring job security.

Beyond the basic premise of income replacement, the current landscape is defined by its focus on “equitable access,” which in 2026 translates into lower earning thresholds and broader definitions of “family member.” Unlike the early iterations of these programs, modern PFML statutes increasingly include chosen family and non-traditional domestic partnerships within their scope of coverage. This shift necessitates a sophisticated analysis of how individual state trust funds are capitalized and the long-term solvency projections that dictate the annual adjustment of contribution rates and maximum weekly benefit amounts. For the individual, this means that the “effective” benefit may vary significantly depending on the timing of the claim and the specific legislative session preceding it.

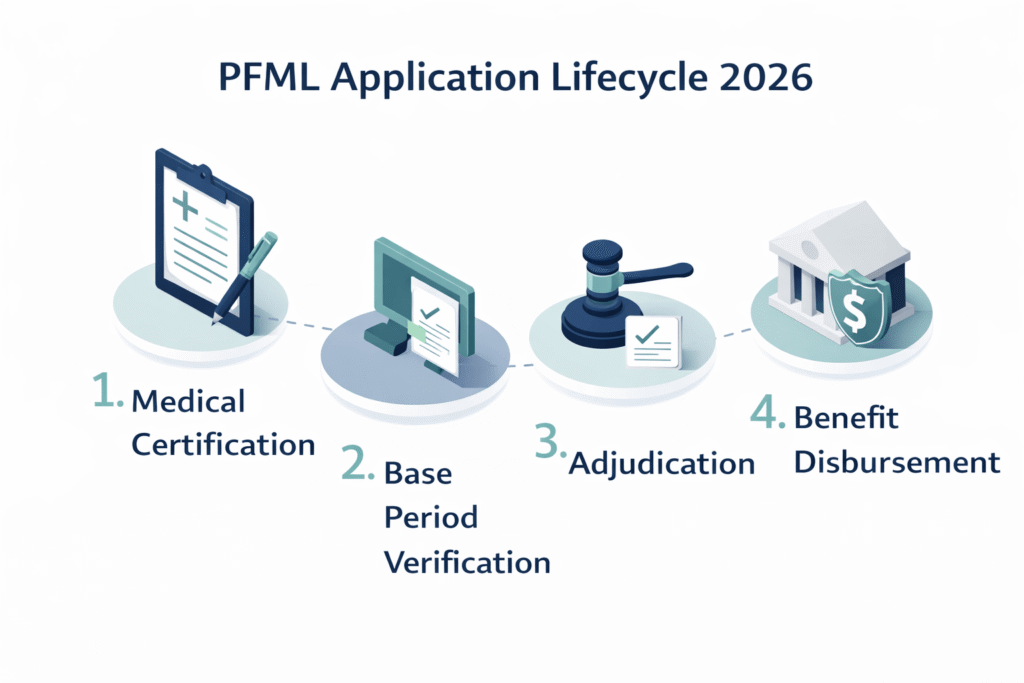

Technical sophistication in the administration of these programs has also surged, with most states now utilizing automated verification systems linked directly to tax and employment records. This integration reduces the friction of the application process but simultaneously increases the risk of denial due to data mismatches or incomplete documentation of medical necessity. As we move further into 2026, the emphasis remains on the “totality of the claim,” where the narrative provided by the healthcare professional must align perfectly with the statutory definitions of a “serious health condition.” This alignment is the primary hurdle for applicants, requiring a deep dive into the regulatory language that governs medical certifications and the specific duration of authorized leave.

The Interplay Between FMLA and State-Mandated Paid Programs

A common point of friction in the benefits ecosystem is the coordination between the federal Family and Medical Leave Act (FMLA) and state-specific paid leave laws. While the federal FMLA provides up to 12 weeks of unpaid, job-protected leave for eligible employees of covered employers, it does not provide any wage replacement. State PFML programs, conversely, focus primarily on the financial aspect but often include their own independent job protection clauses that may or may not run concurrently with federal law. Navigating this intersection requires a granular understanding of which statute offers the “greater” protection in any given scenario, as employers are generally required to adhere to the standard most favorable to the employee.

The mechanics of “concurrent leave” are particularly sensitive when it comes to the depletion of available time. If an employee is eligible for both FMLA and state PFML, the leave periods typically run at the same time; however, if the state law defines a “serious health condition” more broadly than the federal statute, an employee might exhaust their state paid benefits while still retaining a balance of federal unpaid leave, or vice versa. This discrepancy often leads to administrative errors where employees are prematurely cleared for return to work or, conversely, find themselves without job protection despite having remaining paid benefits in their state account.

The cardinal rule of 2026 leave management is that financial eligibility for state benefits does not automatically confer federal job protection; these are distinct legal mechanisms that must be qualified for independently to ensure total socioeconomic security.

Strategic planning for extended leave must therefore account for the specific “benefit year” definitions used by both state and federal entities. Some jurisdictions utilize a “rolling” 12-month period measured backward from the date leave is used, while others use a fixed calendar year or a “forward-looking” year triggered by the first day of leave. This distinction is critical for individuals managing chronic conditions that require multiple periods of leave throughout a single year, as it dictates the exact moment when the “clock” resets for both payment and job reinstatement rights.

Eligibility Thresholds and Benefit Calculation Matrices

Determining the exact dollar amount of a PFML benefit requires an analysis of the “Base Period” earnings, a technical window that typically looks at the first four of the last five completed calendar quarters. In 2026, most progressive states have adopted a multi-tiered replacement rate, where lower-income earners receive a higher percentage of their Average Weekly Wage (AWW) compared to high-income earners. This progressive structure is designed to provide a meaningful safety net for those who would otherwise be disproportionately impacted by any reduction in take-home pay. The following data points illustrate the typical variance in the 2026 regulatory environment:

| State Category Type | Wage Replacement Rate | Max Weekly Benefit (2026 Est.) | Minimum Participation Period |

| Tier 1 (High Progressivity) | 90% of AWW | $1,250 – $1,400 | 18 – 26 weeks |

| Tier 2 (Moderate) | 60% – 75% of AWW | $1,000 – $1,200 | 26 – 52 weeks |

| Tier 3 (Basic/New Programs) | 50% of AWW | $800 – $950 | 12 months |

The calculation of the “Average Weekly Wage” is itself a potential pitfall, as it often includes bonuses, overtime, and commissions which can fluctuate. If a claimant’s earnings were uncharacteristically low during the base period due to illness or industry-wide layoffs, the resulting benefit might not accurately reflect their current financial needs. To mitigate this, some jurisdictions allow for an “Alternative Base Period” (ABP), which looks at the most recent four completed quarters. Requesting an ABP calculation is a sophisticated maneuver that can significantly increase the weekly benefit amount for those with rising income trajectories.

Finally, one must consider the taxability of these benefits at both the state and federal levels. While state-level treatment varies, the IRS generally views PFML benefits as taxable income if they are considered a substitute for wages, though the specific classification (e.g., as unemployment compensation or disability pay) can lead to different reporting requirements. Failure to set aside a portion of the weekly benefit for year-end tax obligations is a frequent oversight that can lead to unexpected liabilities during the following filing season.

Critical Compliance Nuances for Intermittent Leave and Job Protection

Intermittent leave represents the most complex iteration of the PFML framework, allowing employees to take leave in small increments—sometimes as short as one hour—to manage treatments like chemotherapy or physical therapy. From a technical standpoint, managing an intermittent claim requires rigorous tracking of hours and a clear “medical necessity” statement from a provider that specifies the expected frequency and duration of the episodes of incapacity. In 2026, the burden of proof for intermittent leave has tightened, as agencies look to prevent the “blurring” of leave with standard vacation time or general absenteeism.

Job protection during these periods is not universal and often hinges on the size of the employer and the employee’s tenure. Even in states with robust PFML, “small employer exceptions” may still exist, meaning an employee could be eligible for the money but not the right to return to their specific position. This creates a precarious situation where an individual must weigh the financial benefit against the potential loss of their career path. Understanding the “reinstatement” rights—specifically the requirement that an employee be returned to the same or an equivalent position with the same pay and benefits—is the cornerstone of any successful leave strategy.

Furthermore, the “maintenance of health benefits” is a critical protection that is often misunderstood. Under most PFML and FMLA regulations, an employer must continue the employee’s health insurance coverage during the leave period under the same conditions as if the employee had continued to work. However, the employee is still responsible for their portion of the premiums. If the employee fails to make these payments, the employer may, under certain strict conditions, terminate the coverage, provided they give adequate notice. This highlights the importance of maintaining a clear line of communication with the HR or benefits department regarding the logistics of premium payments during an extended absence.

The documentation required to solidify these protections is extensive and must be handled with precision to avoid administrative “red flags” that trigger audits or delays. The essential components of a robust medical certification include:

- The date on which the serious health condition commenced and its probable duration.

- A concise statement of the appropriate medical facts regarding the condition.

- An explicit confirmation that the employee is unable to perform the functions of their position.

- In the case of intermittent leave, a statement of the medical necessity for such leave and an estimate of the schedule.

- The signature and credentials of a licensed healthcare provider within a valid jurisdiction.

Failure to provide a “complete and sufficient” certification within the statutory timeframe (usually 15 days) can lead to a retroactive denial of leave, leaving the employee vulnerable to disciplinary action for unexcused absences. This underscores the need for a proactive approach, where the employee coordinates with their medical provider well in advance of the anticipated leave date to ensure all regulatory “boxes” are checked.

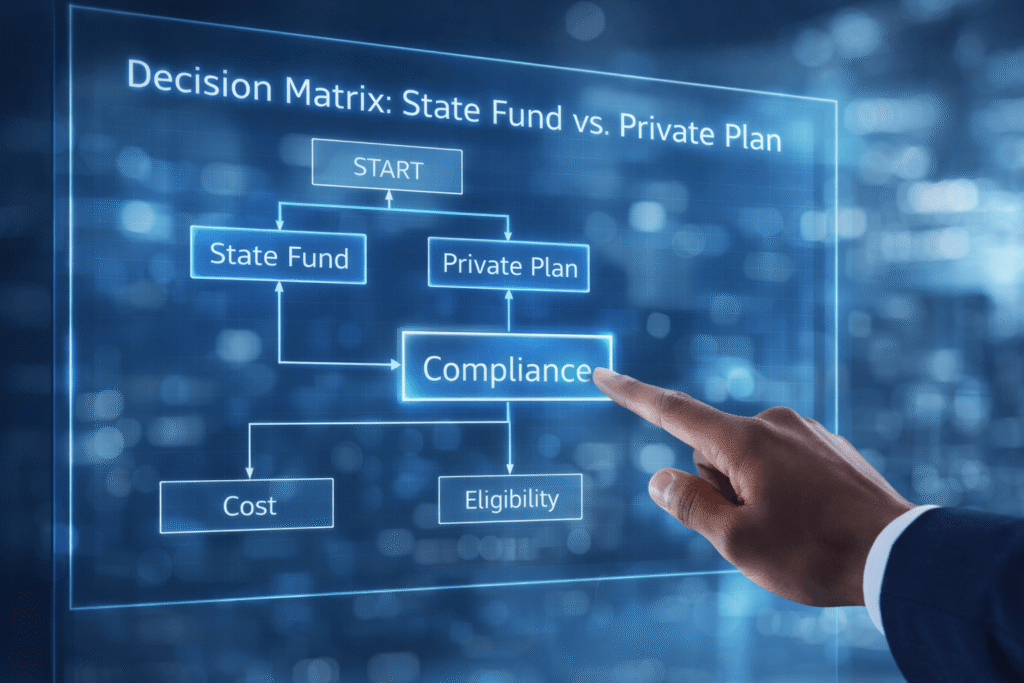

Private Plan Exemptions and Employer Self-Insurance Risks

In several states, employers are permitted to “opt-out” of the state-run PFML plan if they provide a private plan that offers benefits equal to or greater than the state’s statutory requirements. These private plans, often referred to as “Voluntary Plans,” are frequently managed by third-party insurers and may have different filing procedures and adjudication timelines than the state agency. For the employee, this means their claim will not be processed through the standard state portal, but rather through a corporate-specific insurance carrier. It is vital to verify whether an employer is utilizing the state fund or a private exemption, as the “appeals process” for a denied claim can differ drastically between the two.

The risk of “self-insurance” by employers—where the company pays benefits directly from its own assets rather than through an insurance policy—adds another layer of scrutiny. While self-insured plans must still meet state standards, they are sometimes more aggressive in their “Independent Medical Examination” (IME) requirements. An IME allows the employer or the insurer to require the claimant to be examined by a doctor of their choosing to verify the disability. In 2026, the use of IMEs has become a strategic tool for managing the costs of long-term claims, making it imperative for claimants to have a well-documented primary medical record to counter any conflicting opinions.

Ultimately, the goal of navigating these private exemptions is to ensure that no “coverage gaps” occur during the transition between different types of leave or when changing employers. If an employee moves from a company with a private plan to one that uses the state fund, they must understand how their “accrued” earnings from the previous employer will be treated by the state agency. Most modern statutes allow for “portability” of earnings, meaning the state will look at the total wages earned across all employers during the base period, but the administrative lag in verifying these records can lead to significant delays in the first benefit payment.

FAQ: Integrated Compliance and Claims Management

How does the “Substitution of Paid Leave” rule affect the total duration of PFML benefits when an employer requires the use of accrued PTO?

In 2026, the interaction between employer-provided Paid Time Off (PTO) and state PFML is governed by specific “anti-stacking” or “integration” clauses. If a state law allows for the “integration” of benefits, an employer can require an employee to use their accrued PTO concurrently with PFML to “top off” the state benefit to 100% of their normal salary. However, the employer generally cannot force the exhaustion of PTO before PFML begins if doing so would effectively shorten the total period of protected leave available to the employee under the law.

In the context of “Successive Periods of Leave,” what technical criteria determine if a new claim is a continuation of a prior one or a separate “Benefit Year” event?

The determination hinges on the “Recovery Period” and the “Cause of Incapacity.” If an employee returns to work for a period (often 14 to 30 days, depending on the state) and then requires leave again for the same underlying medical condition, it is typically treated as a single claim, and the “Waiting Period” is not reapplied. However, if the subsequent leave is for a different qualifying reason, or if the return-to-work period exceeds the statutory threshold, it may be classified as a new claim, potentially triggering a new waiting period and a re-evaluation of the Base Period earnings.

What are the legal implications of “Interstate Telecommuting” on PFML eligibility when the employer is headquartered in a state with benefits but the employee resides in one without?

The “Localization of Work” test is the primary determinant here. Generally, PFML eligibility is tied to where the work is performed and where unemployment insurance taxes are paid, not where the company is headquartered. If a remote worker is physically performing services in a state that does not have a PFML program, they are usually ineligible for the benefits of the employer’s home state, unless a specific “reciprocal agreement” exists or the employer has opted into the program for their out-of-state workforce. This makes the physical location of the “home office” for a remote worker a critical data point in benefit litigation.