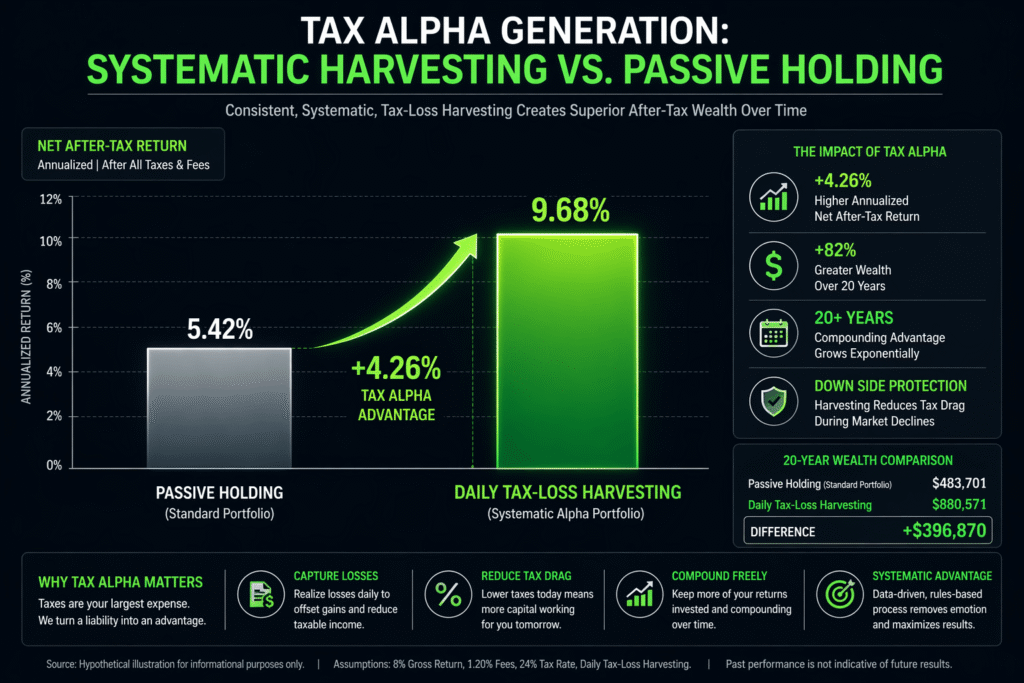

In the fiscal landscape of 2026, tax-loss harvesting has evolved from a simple year-end ritual into a high-frequency, year-round strategic necessity. This technique involves the deliberate sale of securities at a loss to offset capital gains liabilities, thereby lowering the investor’s overall Adjusted Gross Income (AGI). However, as the IRS adopts more sophisticated data-matching algorithms, the margin for error has narrowed significantly. Modern investors must now contend with a regulatory environment where the velocity of transactions and the correlation between diverse asset classes are under intense scrutiny, making the technical execution of these trades as important as the underlying investment logic.

The fundamental objective of harvesting in 2026 is the generation of “Tax Alpha”—the additional return achieved through proactive tax management. By realizing losses today, investors can defer tax payments to future years, effectively receiving an interest-free loan from the government that can be reinvested to achieve compound growth. Yet, this strategy is not without its pitfalls. The interaction between short-term capital gains (taxed at ordinary income rates) and long-term capital gains (taxed at preferential rates) requires a granular netting process that must be meticulously documented to survive an automated IRS audit.

Furthermore, the 2026 tax year is marked by the looming sunset of several provisions from the Tax Cuts and Jobs Act (TCJA). This shift has created an urgent need for investors to re-evaluate their cost-basis methods and harvesting thresholds. As tax brackets are projected to rise, the value of a harvested loss increases, but so does the risk of falling foul of the Wash Sale Rule. Successfully navigating these waters requires a deep understanding of the technical constraints that govern the replacement of assets and the specific timelines that define a legal tax-loss transaction.

The “Substantially Identical” Technical Trap: Cross-Asset Analysis

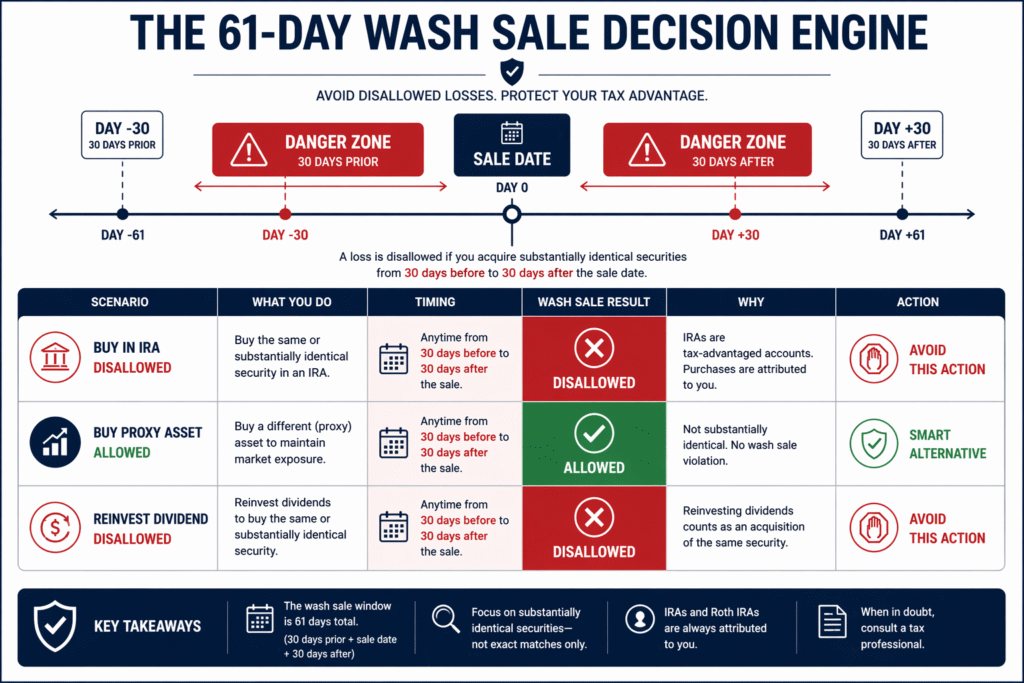

The Wash Sale Rule (Internal Revenue Code Section 1091) remains the most significant technical hurdle in the harvesting process. It prohibits an investor from claiming a loss on the sale of a security if they purchase a “substantially identical” security within 30 days before or after the sale. In 2026, the definition of “substantially identical” has been functionally expanded through revenue rulings to address modern financial products. For example, selling an S&P 500 ETF from one provider and immediately buying an S&P 500 ETF from another may now be flagged as a wash sale if the underlying indices and weightings are nearly identical.

This technical trap extends across different account types, including IRAs and 401(k)s. A common mistake in 2026 is selling a stock in a taxable brokerage account for a loss while simultaneously purchasing it within a tax-advantaged retirement account. The IRS treats this as a violation, permanently disallowing the loss and preventing the investor from adding the disallowed loss to the basis of the new shares in the IRA. This “permanent loss” scenario is a catastrophic outcome for a tax-optimization strategy and underscores the need for a holistic view of the investor’s entire portfolio across all custodians.

The cardinal rule of 2026 harvesting is that the 61-day wash sale window (30 days before, the day of, and 30 days after the sale) is absolute and indifferent to the investor’s intent; technical compliance is the only defense.

To avoid these traps, sophisticated investors utilize “Asset Class Proxies”—securities that are highly correlated but not “substantially identical.” For instance, an investor might sell a Large-Cap Growth ETF at a loss and replace it with a Total Stock Market ETF. While the price movements may be similar, the underlying portfolios are legally distinct enough to satisfy the current regulatory interpretations. This requires a precise quantitative analysis of tracking error and factor exposure to ensure the investor maintains their desired market position without triggering a disallowed loss.

Quantitative Optimization: Netting Capital Gains against Losses in 2026

The arithmetic of the 2026 tax code requires a specific sequence for netting gains and losses. First, short-term losses are used to offset short-term gains. Second, long-term losses offset long-term gains. If a net loss remains in either category, it can be used to offset the remaining gain of the other type. This “netting hierarchy” is critical because short-term gains are typically taxed at much higher rates (up to 37% or more depending on the bracket). The following table illustrates the Tax Rate Arbitrage available in the 2026 fiscal environment:

| Gain/Loss Category | 2026 Est. Tax Rate (Top Bracket) | Netting Priority | Strategic Value of Loss |

| Short-Term Capital Gain | ~37% – 39.6% | Offset by ST Loss first | High (Direct Income Offset) |

| Long-Term Capital Gain | ~20% | Offset by LT Loss first | Moderate (Preferential Rate) |

| Ordinary Income | Up to 39.6% | Offset by remaining loss | Maximum ($3,000 limit) |

| Net Investment Income | +3.8% (Surtax) | Integrated into totals | High (Surtax Avoidance) |

If an investor has more losses than gains, they can use up to $3,000 of the excess loss to offset their ordinary income (like salary or interest). Any remaining loss beyond that amount is “carried forward” to future tax years indefinitely. In 2026, the Carryforward Ledger is a vital asset, especially as investors anticipate higher tax rates in the future. Managing this ledger requires consistent tracking of the “character” of the loss (short-term vs. long-term) to ensure it is applied most efficiently in subsequent years.

The integration of the Net Investment Income Tax (NIIT) of 3.8% adds another layer of complexity. Strategic harvesting can keep an investor’s Modified Adjusted Gross Income (MAGI) below the thresholds ($200k for individuals, $250k for couples), effectively saving an additional 3.8% on all investment income. This “threshold management” is a primary focus for high earners in 2026, making the timing of loss realization a pivotal factor in the overall annual tax liability.

Strategic Harvesting in Digital Assets and Crypto-to-Equity Correlates

The year 2026 has seen the finalization of rules regarding the Wash Sale Rule for Digital Assets. Previously, cryptocurrencies were treated as “property” rather than “securities,” allowing investors to sell at a loss and immediately buy back. However, new legislative amendments have closed this loophole, bringing crypto-assets under the 30-day wash sale umbrella. This has forced a shift toward “Cross-Correlation Harvesting,” where an investor might sell Bitcoin at a loss and temporarily move into a highly correlated Bitcoin Mining stock or a Crypto-ETF to maintain exposure.

Furthermore, the Specific Identification method for cost-basis has become the technical gold standard. In a volatile market, an investor may have multiple “lots” of the same digital asset purchased at different prices. By selecting the highest-cost lots to sell, the investor can maximize the realized loss. In 2026, most major exchanges provide API-linked tax software that automates this “High-Cost, First-Out” (HIFO) logic, but the burden remains on the taxpayer to ensure the data reconciles with their 1099-DA forms.

The interaction between decentralized finance (DeFi) and traditional equity portfolios also presents new opportunities. Investors are increasingly using “Synthetic Assets” to hedge positions while they wait for the 30-day wash sale clock to reset. However, the IRS has signaled that it will look through these synthetic hedges if they lack economic substance and are used solely for tax avoidance. Maintaining a clear “investment thesis” for every swap is essential for surviving a 2026 audit of crypto-heavy portfolios.

Automated Rebalancing and the Risks of Direct Indexing

To manage these complexities, many investors have turned to Direct Indexing. This strategy involves owning the individual stocks that make up an index rather than the index fund itself. In 2026, AI-driven platforms can scan a portfolio of 500 stocks daily, selling individual losers even when the overall index is up. This creates a constant stream of Tax Alpha. However, direct indexing creates a “data explosion” in tax reporting, with some investors generating hundreds of pages of Form 8949 attachments.

The risk of “Basis Washout” is a concern with automated rebalancing. If a system is too aggressive in harvesting, the investor may end up with a very low cost-basis across their entire portfolio. While this saves taxes today, it creates a massive “tax bomb” for the future when the assets are eventually sold. Therefore, a technical audit of “rebalancing frequency” is necessary to ensure the system is not sacrificing long-term capital efficiency for short-term tax wins.

Before finalizing any year-end transactions, investors should execute the following Harvesting Compliance Checklist:

- Consolidated Account Review: Check for purchases of the same or “substantially identical” assets in IRAs or spouse’s accounts.

- Cost-Basis Method Verification: Ensure the broker is using “Specific ID” or “HIFO” as intended.

- Dividend Reinvestment Audit: Disable “Auto-Reinvest” for 30 days around the sale to prevent a “replacement purchase” wash sale.

- Alternative Asset Selection: Identify “Proxy Assets” with at least a 0.90 correlation but distinct legal structures.

- Income Threshold Check: Project MAGI to determine if harvesting will trigger or avoid the 3.8% NIIT.

FAQ: Portfolio Taxation and Capital Gains Optimization

Does the Wash Sale Rule apply if I sell a stock at a loss and my spouse buys it in their separate account?

Yes. In 2026, the IRS continues to apply the “Related Party” rules strictly. Transactions by a spouse are treated as if they were made by the taxpayer. This includes purchases in the spouse’s individual brokerage accounts or their employer-sponsored retirement plans. To avoid a disallowed loss, the entire household must remain out of the security for the full 61-day window.

How does the “De Minimis” rule affect small-scale harvesting of fractional shares in 2026?

While some have argued for a “De Minimis” exception for very small losses (e.g., under $10), the IRS does not officially recognize such a threshold for the wash sale rule. Even a fractional share purchase triggered by a dividend reinvestment can technically “wash” a portion of a large loss. In 2026, the technical solution is to ensure all dividend reinvestments are paused across the entire household during the harvesting window to prevent even a few cents from invalidating a multi-thousand-dollar loss.

If I sell a security at a loss and then sell a “Put Option” on that same security, have I triggered a wash sale?

This is a high-complexity “edge case.” Under current 2026 interpretations, selling a “Deep-in-the-Money” Put Option is considered a contract to acquire the stock and therefore triggers the Wash Sale Rule. If the option is “Out-of-the-Money” and there is a significant chance it will expire worthless, it may not trigger the rule, but the IRS uses a “facts and circumstances” test. Sophisticated traders avoid selling puts on harvested assets during the 30-day window to eliminate this regulatory risk.

Can I use losses from a “Personal Use Asset,” such as a primary residence or a vehicle, to offset investment gains?

No. This remains a rigid boundary in the tax code. Losses on personal use assets are not deductible and cannot be used to offset capital gains from investments. Only losses from assets held for “investment or the production of income” are eligible for harvesting. Attempting to claim a loss on a personal vehicle or home as a capital loss is a major “red flag” that often triggers an immediate manual audit of the entire tax return.