The American retirement landscape has entered a “Super-Cycle” in 2026, defined by the full technical implementation of the SECURE 2.0 Act‘s most disruptive provisions. For high-earning professionals and those nearing the conclusion of their primary career arc, the rules for wealth accumulation have been fundamentally rewritten. No longer is retirement planning a simple matter of maximizing a pre-tax 401(k); it now requires a sophisticated understanding of Roth mandates, age-specific contribution tiers, and the integration of new emergency liquidity vehicles. In 2026, the primary objective is to navigate these “tax-diversification” requirements while capitalizing on significantly higher contribution ceilings.

The most profound shift in 2026 is the mandatory “Rothification” of catch-up contributions for certain high-paid participants. This regulatory change forces a pivot from immediate tax deduction toward long-term tax-free growth—a transition that requires a total re-evaluation of late-stage career cash flows. Simultaneously, the IRS has introduced a unique “Super Catch-up” tier for a specific age bracket, creating a four-year window of maximum accumulation potential that surpasses any previous retirement vehicle. Mastering this cycle is essential for any professional looking to bridge the gap between their current earnings and a tax-efficient retirement.

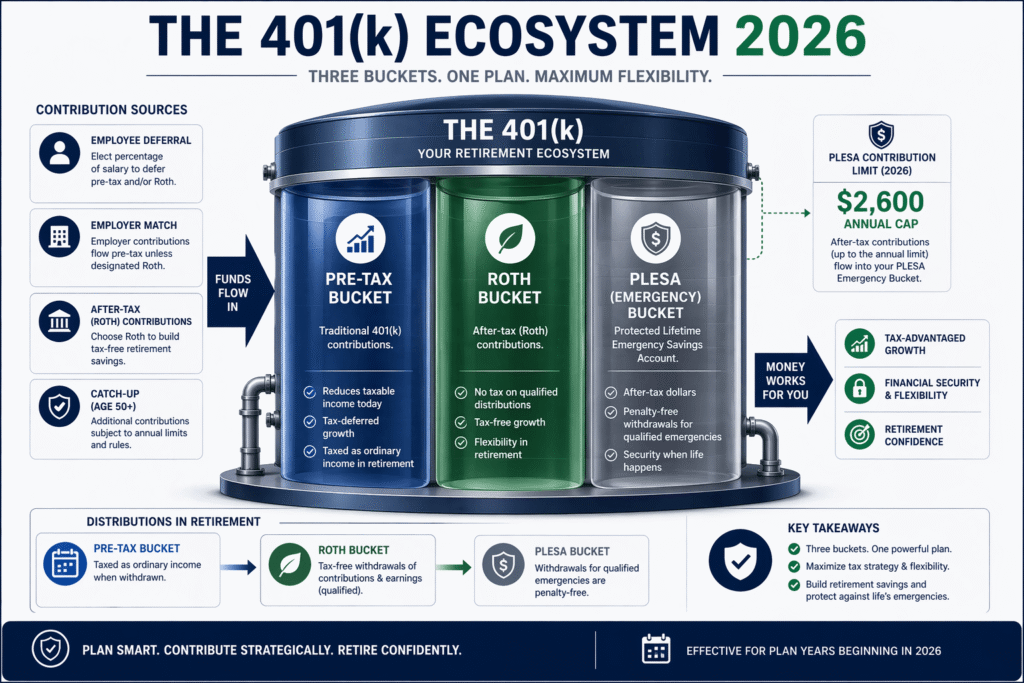

As we move through 2026, the integration of Pension-Linked Emergency Savings Accounts (PLESA) into the 401(k) ecosystem has also matured. These accounts offer a new hybrid of retirement saving and immediate liquidity, primarily designed to prevent the “leakage” of long-term assets during short-term financial shocks. For the strategic investor, 2026 is about orchestrating these various “buckets”—Pre-tax, Roth, and PLESA—to create a resilient, multi-layered financial infrastructure that can withstand both market volatility and legislative shifts.

The $11,250 “Super Catch-up”: Technical Eligibility for Ages 60-63

A cornerstone of the 2026 retirement cycle is the specialized “Super Catch-up” provision. While the standard catch-up limit for those aged 50 and older has increased to $8,000, individuals who reach ages 60, 61, 62, or 63 in 2026 are eligible for a significantly higher threshold of $11,250. This “super” tier is designed to allow those in their peak earning years to make a final, aggressive push toward their retirement targets. It effectively creates a four-year “accumulation zone” where a single professional can defer up to $35,750 into their workplace plan in a single year ($24,500 base + $11,250 catch-up).

Eligibility for this higher limit is strictly tied to the participant’s age at the end of the calendar year. However, the technical implementation depends on whether the employer’s plan has been updated to support these SECURE 2.0 enhancements. For professionals within this “golden window,” the strategic imperative is to ensure their payroll deferrals are calibrated early in the year to hit this higher ceiling without exceeding the Section 415(c) annual additions limit, which for 2026 has increased to $72,000 (combined employer and employee contributions, excluding catch-ups).

In 2026, the “Super Catch-up” represents the most powerful tool for late-stage wealth acceleration, but its effectiveness is entirely dependent on the participant’s ability to manage the Roth Mandate if their income exceeds the federal threshold.

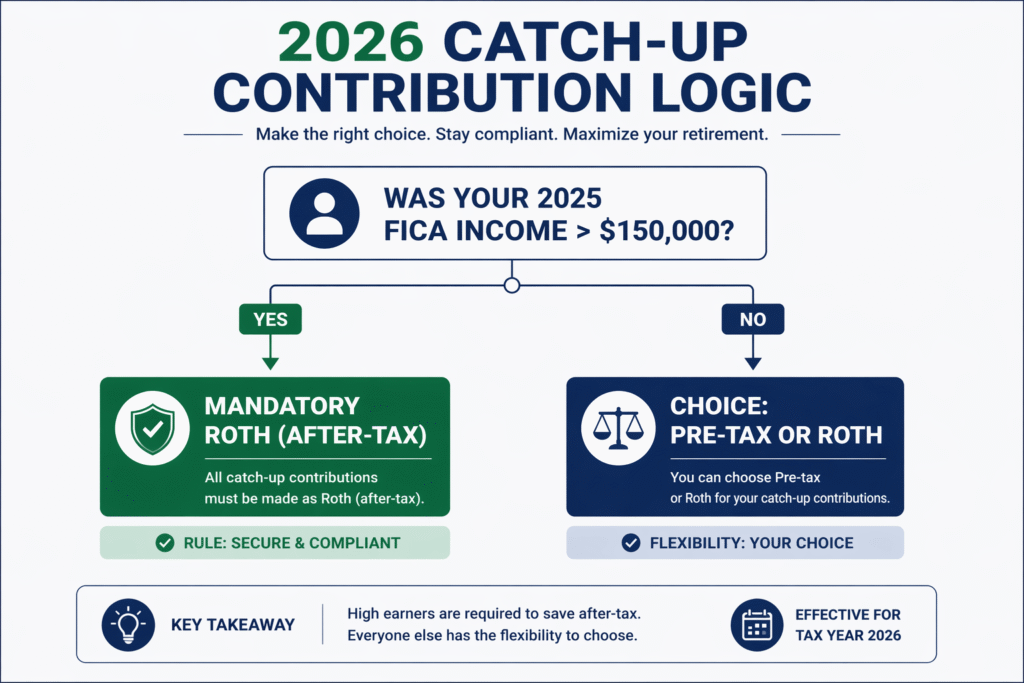

The Mandatory Roth Shift: Navigating the $150,000 Wage Threshold

Beginning January 1, 2026, a critical technical mandate takes effect: all catch-up contributions (both standard and “super”) made by participants whose prior-year FICA wages from their current employer exceeded $150,000 must be made on a Roth (after-tax) basis. This rule effectively eliminates the pre-tax deduction for catch-up amounts for high-earning professionals. If a participant’s wages in 2025 were $150,001 or higher, their plan administrator is legally required to redirect any catch-up elections to a Roth account.

This shift requires a radical adjustment in tax-liability forecasting. While the base contribution of $24,500 can still be made on a pre-tax basis to lower current taxable income, the additional catch-up must be funded with post-tax dollars. This creates a “mixed-tax” contribution profile that, while increasing the immediate tax bill, significantly improves the long-term tax-free withdrawal potential of the account. To visualize the 2026 landscape, the following table summarizes the updated contribution limits across various account types:

| Plan Type | Standard Limit (2026) | Catch-up (Age 50+) | Super Catch-up (60-63) |

| 401(k) / 403(b) | $24,500 | $8,000 (Roth if >$150k) | $11,250 (Roth if >$150k) |

| IRA (Trad/Roth) | $7,500 | $1,100 | N/A |

| SIMPLE IRA | $17,000 | $4,000 | $5,250 |

| HSA (Individual) | $4,400 | $1,000 (Age 55+) | N/A |

For those earning above the $150,000 threshold, the “Roth Mandate” is not optional. If a plan does not offer a Roth feature, it cannot legally accept catch-up contributions from high-earning participants at all. This has forced a widespread adoption of Roth 401(k) features across the corporate world in late 2025 and early 2026 to ensure that senior executives and high-level specialists remain able to maximize their retirement savings.

Quantitative Impact of Accelerated Compounding in Late-Stage Careers

The move toward Roth catch-ups in 2026 actually serves as a powerful catalyst for long-term wealth, despite the loss of the immediate tax deduction. By paying the taxes now at current rates, the entire $11,250 “Super Catch-up”—and all the compound growth it generates over the subsequent 10 to 20 years—is entirely exempt from federal income tax upon withdrawal. For a professional in the 60-63 age window, this represents a massive infusion of tax-free capital that can be used to manage their tax bracket in retirement, particularly when coordinating with Social Security and Required Minimum Distributions (RMDs).

Furthermore, the higher Annual Additions Limit ($72,000 in 2026) allows for a more aggressive total contribution strategy. When a professional maximizes both their elective deferrals and their catch-up amounts, their total “ceiling” in a 401(k) for 2026 can reach $83,250 (including employer match and catch-ups). This level of capital infusion into a tax-advantaged environment creates a “compounding engine” that can significantly alter the trajectory of a retirement portfolio in just a few years.

Strategically, this requires a shift in Asset Location. Because Roth accounts provide tax-free growth, they are the ideal location for assets with the highest expected returns (such as equities). The pre-tax portion of the 401(k) can then be used for lower-growth, income-generating assets. This dual-track approach allows the professional to maximize the “tax-alpha” of their 2026 contributions, ensuring that the most productive capital is also the least taxed at the point of distribution.

Strategic Coordination with Pension-Linked Emergency Savings Accounts (PLESA)

For “Non-Highly Compensated Employees” (those earning under $160,000 in 2026), a new technical feature has emerged: the Pension-Linked Emergency Savings Account (PLESA). These accounts allow employees to contribute up to $2,600 (adjusted for 2026) on a Roth-like basis within their 401(k) plan. Unlike standard retirement funds, PLESA funds can be withdrawn at least once a month for any reason without the 10% early withdrawal penalty, making them a perfect liquidity buffer for short-term needs.

For the 2026 professional, the PLESA acts as a “gateway” to retirement saving. Contributions to a PLESA are treated as elective deferrals for the purpose of employer matching. This means an employee can secure their full company match while keeping their own contributions accessible for emergencies. Once the $2,600 cap is reached, any additional contributions are automatically directed into the employee’s regular Roth 401(k). This integration ensures that the “Super-Cycle” of saving continues even after the emergency fund is fully capitalized.

To ensure total compliance with the 2026 Retirement Super-Cycle, professionals should follow this Roth Catch-up Audit Checklist:

- Prior-Year Wage Verification: Review your 2025 Form W-2 (Box 3) to see if FICA wages exceeded $150,000.

- Plan Document Audit: Confirm your employer’s 401(k) has been amended to include Roth catch-up and Super Catch-up features.

- Age-Target Calibration: Verify if you attain age 60, 61, 62, or 63 at any point in 2026 to qualify for the $11,250 limit.

- Tax Bracket Forecasting: Adjust your quarterly tax estimates or payroll withholdings to account for the loss of the catch-up tax deduction.

- Beneficiary Update: Ensure your Roth and Pre-tax “buckets” have clearly defined beneficiaries, as they may follow different inheritance tax rules.

FAQ: Retirement Planning and Legislative Compliance

What happens if I make a catch-up contribution in 2026 but my income was exactly $150,000 in 2025?

The “Roth Mandate” only triggers if your prior-year FICA wages were greater than $150,000. If you earned exactly $150,000 or less, you retain the choice to make your catch-up contributions on a pre-tax or Roth basis, assuming your plan offers both options. This $150,000 threshold is scheduled to be indexed for inflation in future years, but for 2026, it is a “hard” limit based on your 2025 W-2 from your current employer.

If I change jobs mid-year in 2026, how do my wages from the previous employer affect the Roth Mandate?

This is a critical technical nuance. The $150,000 threshold applies to wages received from the employer sponsoring the plan. If you move to a new company in 2026, your wages from your previous employer in 2025 generally do not trigger the Roth mandate at your new company’s plan. You would effectively be treated as having $0 in prior-year wages with the new employer, allowing you to make catch-up contributions on a pre-tax basis for the remainder of 2026.

Can I still do a “Backdoor Roth IRA” if I am also making mandatory Roth catch-up contributions to my 401(k)?

Yes. The 2026 rules for Roth IRAs are separate from workplace 401(k) rules. While your income may be too high for a direct Roth IRA contribution (2026 phase-outs start at higher levels), the “Backdoor Roth” strategy remains a viable technical path. Making mandatory Roth catch-ups in your 401(k) does not disqualify you from executing a non-deductible Traditional IRA contribution and subsequent conversion to a Roth IRA.

What is the penalty if my company fails to implement the Roth catch-up rule on time in 2026?

The IRS has provided a “good faith” administrative transition period, but by January 1, 2026, plans are expected to be operationally compliant. If a plan fails to correctly categorize catch-up contributions as Roth for a high-earner, it could jeopardize the qualified status of the entire plan. In practice, most payroll systems have been updated to “auto-detect” this based on the previous year’s W-2 data to prevent accidental non-compliance.