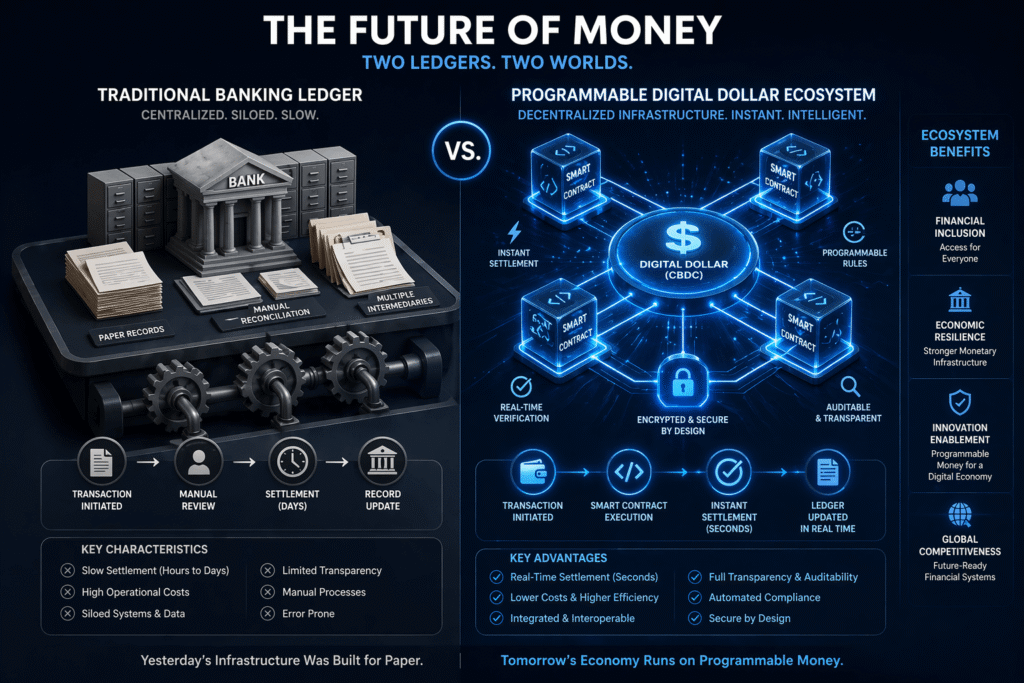

The global financial architecture has reached a pivotal inflection point in 2026 as Central Bank Digital Currencies (CBDCs) transition from experimental pilots to integrated components of the monetary system. While the United States has maintained a cautious stance regarding a direct retail “Digital Dollar,” the rapid expansion of the FedNow Service and the tokenization of traditional assets have created a functional equivalent for many high-net-worth investors. In this new landscape, personal wealth management is no longer just about asset allocation; it is about managing the programmability of money and navigating the real-time transparency required by modern regulatory frameworks.

This digital evolution is driven by the convergence of Traditional Finance (TradFi) and Decentralized Finance (DeFi). By 2026, entire asset classes—from real estate to private equity—have become tradable on-chain, reshaping investment liquidity and global capital flows. For the individual investor, this means that “cash” is becoming a dynamic, tokenized asset that can be embedded directly into smart contracts for automated management. Understanding how these digital rails interact with your existing portfolio is essential to maintaining financial agility in an economy that now moves at sub-second speeds.

Furthermore, the introduction of global standards like CRS 2.0 and the Crypto-Asset Reporting Framework (CARF) has effectively ended the era of “analog” financial privacy. As of January 1, 2026, financial institutions and digital asset service providers are required to report transaction-level data in real-time, closing long-standing visibility gaps for tax authorities. Consequently, wealth management in 2026 requires a “compliance-first” mindset, where every movement of capital is documented by design within the digital ledger architecture.

Understanding the Programmability of CBDC: Smart Contracts in Daily Finance

The technical defining feature of a CBDC or a tokenized deposit is its programmability. Unlike traditional fiat, which is a static medium of exchange, a programmable digital dollar allows for specific rules and conditions to be embedded directly into the currency’s code via smart contracts. This means that a payment can be made automatically contingent on the completion of another transaction or the occurrence of a verified event, such as a stock price hitting a certain threshold or a legal document being digitally signed.

In 2026, this automation is being utilized to streamline complex financial instruments that previously required multiple intermediaries. For example, a wealth manager can now set up automated inheritance triggers or tax-withholding protocols that execute the moment a dividend is paid. This reduces settlement risk and operational costs, but it also places a premium on the “code-level” security of your financial directives. For the elite investor, the ability to audit and verify these self-executing contracts is becoming as important as the ability to read a traditional balance sheet.

The most significant risk in 2026 digital finance is “algorithmic entrapment,” where poorly coded smart contracts execute irreversible transactions based on faulty data triggers, necessitating a new tier of technical audit for personal wealth.

Managing these programmable assets also involves navigating the “logic layers” of different digital wallets. While some central banks are rolling out interest-bearing digital wallets, others are focusing on streamlining collateral management for credit guarantees. The strategic choice of where to hold your digital cash now dictates not just your interest rate, but also the types of automated financial services you can access across the global digital economy.

Real-Time Tax Reporting and the End of Annual Filing Latency

The activation of the CARF and CRS 2.0 reporting regimes on January 1, 2026, has fundamentally expanded global tax transparency. Under these new rules, Specified Electronic Money Products (SEMPs) and CBDCs are included in automatic exchange regimes, meaning that tax authorities now have near-instant visibility into cross-border digital movements. This shift effectively eliminates the “latency” of annual reporting, as financial institutions are now mandated to report transaction-level data, sale values, and precise customer identifiers as they occur.

For personal wealth management, this means that tax-loss harvesting and capital gains optimization must happen in real-time. To understand the impact of this increased visibility, the following table compares the compliance and liquidity characteristics of the primary 2026 digital assets:

| Asset Type | Regulatory Framework | Tax Reporting Latency | Liquidity / Settlement |

| Retail CBDC / SEMP | CRS 2.0 (Automatic) | Real-Time / Atomic | T+0 (Instant) |

| Private Crypto | CARF (Global) | Annual / Transactional | Varies by Network |

| Stablecoins | GENIUS Act (US) | Quarterly / Audited | T+0 (Fungible) |

| Tokenized Stocks | TradFi / SEC | Standard Brokerage | T+1 (Standardized) |

This “data-rich” environment is designed to reduce illegal transactions, but it also creates a massive administrative burden for individuals with complex, high-frequency portfolios. Leading wealth management firms in 2026 have responded by launching AI-augmented advisors that act as the “last-mile” human, helping clients navigate these real-time compliance requirements. These advisors use unified client brains—large data models that consolidate a client’s entire financial footprint—to ensure that every transaction is optimized for both tax efficiency and regulatory “green-flag” signaling.

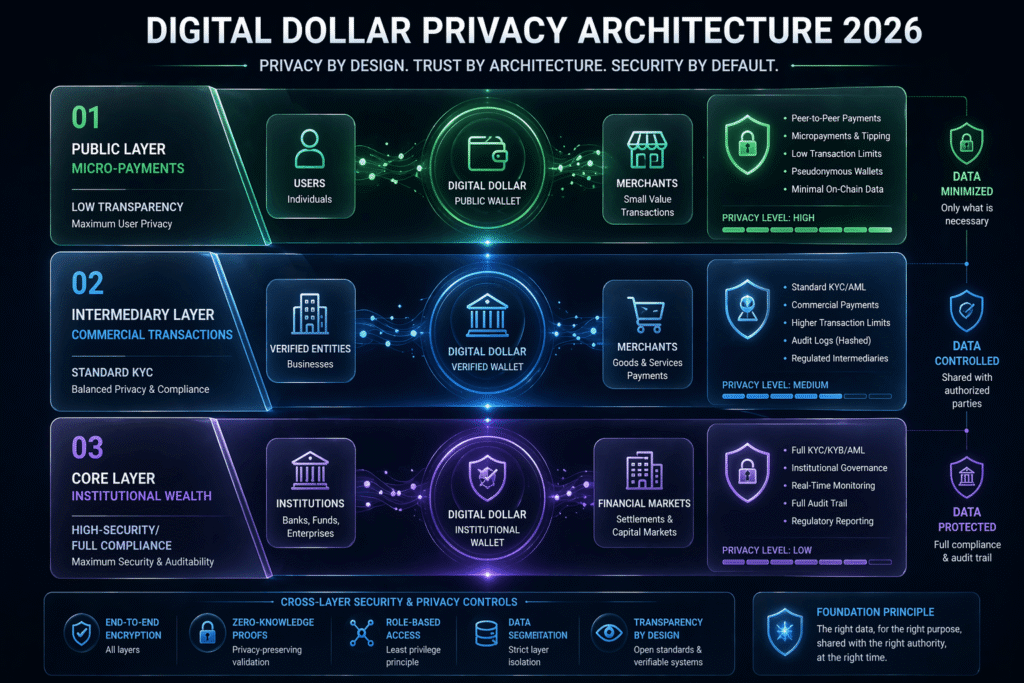

Privacy Tiers and the Technical Architecture of the FedNow Nexus

A common point of technical confusion in 2026 is the distinction between the FedNow Service and a CBDC. While a CBDC is a form of currency—a digital means of storing value—FedNow is an instant payment infrastructure, similar to a highway system that allows funds to move between existing bank accounts in real-time. Because FedNow operates through traditional depository institutions, it maintains a layer of intermediary privacy that a direct retail CBDC might lack.

However, the “data-rich” nature of the ISO 20022 messaging standard used by FedNow means that even traditional bank transfers now carry significantly more metadata than in the past. This metadata can include detailed invoices, purpose-of-payment codes, and even AI-readable tags that categorize the transaction for the bank’s internal risk-assessment algorithms. For the wealth manager, this requires a strategic approach to “transaction narrative” management, ensuring that large-scale capital movements are clearly labeled to avoid triggering automated AML (Anti-Money Laundering) freezes.

The privacy architecture of 2026 is increasingly tiered based on the size and frequency of the transaction. Small, daily payments may enjoy a higher degree of anonymity, while large transfers are subject to the full suite of Know Your Customer (KYC) and reporting protocols. Navigating these tiers requires a multi-wallet strategy, where high-liquidity, lower-privacy accounts are used for standard operations, while high-privacy, cold-storage assets are reserved for long-term wealth preservation.

Strategic Liquidity Management in a High-Velocity Digital Economy

In a high-velocity economy where funds can be settled instantly 24/7/365 through FedNow or CBDCs, the traditional concept of “idle cash” has been replaced by tokenized cash economics. Wealth managers are now focusing on “embedded wealth,” where cash is automatically swept into yield-bearing digital tokens that remain as liquid as cash but provide a market-rate return. This eliminates the trade-off between liquidity and yield, allowing an investor to remain 100% invested while still having “instant” access to capital for opportunistic trades or unforeseen expenses.

However, this high-velocity environment also increases the risk of market contagion. Because transactions are now frictionless and data-rich, “shock weeks” can unfold in hours rather than days, as algorithms react instantly to geopolitical or economic shifts. Preparing for these scenarios in 2026 involves baking Lombard stress scenarios and downturn-ready protocols directly into your digital asset management system. This ensures that your portfolio can automatically de-risk or hedge itself during periods of extreme volatility without requiring manual intervention during the crisis.

To ensure your wealth management strategy is ready for the Digital Dollar era, consider the following CBDC Readiness Checklist:

- Wallet Interoperability Audit: Ensure your primary wallets can interact with both private stablecoins and central bank infrastructure.

- Smart Contract Verification: Review the code and audit reports for any “programmable” assets or automated yield protocols in your portfolio.

- Real-Time Tax Syncing: Connect your digital asset platforms to automated tax-reporting software that supports CARF and CRS 2.0.

- Emergency Liquidity “Kill-Switches”: Set up automated triggers to move assets to secure, non-custodial environments during periods of high systemic risk.

- FedNow/CBDC Fee Optimization: Review the 2026 fee schedules for instant payment services to ensure high-frequency rebalancing remains cost-effective.

FAQ: Central Bank Digital Currencies and Personal Sovereignty

What is the “Clarity Act” and how does it impact the market structure for digital assets in 2026?

The Clarity Act is a major piece of US legislation focused on providing a stable regulatory framework for the digital asset market. It aims to resolve long-standing jurisdictional disputes between the SEC and CFTC, giving businesses the confidence to scale tokenized asset products and helping to unify the rules for stablecoin issuers. For the individual investor, this provides greater policy certainty and ensures that “responsible innovation” is protected within the US financial system.

If the US has taken a stance against a “Retail CBDC,” why should I still care about CBDC trends in 2026?

Even without a direct US retail CBDC, the global financial order is being reshaped by CBDC launches in other major jurisdictions, such as Singapore and the ECB. Because global finance is increasingly interconnected through cross-border digital payment rails, a US investor’s international holdings and payments are already being processed through these new digital architectures. Furthermore, the technical standards established by CBDCs—such as ISO 20022 and smart contract protocols—are being adopted by private US banks to improve their own internal “Digital Dollar” and FedNow offerings.

How does “Tokenization” change the way cash is held on a corporate or personal balance sheet?

Tokenization allows cash and other assets to be embedded directly into a company’s or individual’s core balance-sheet infrastructure. Instead of cash sitting in a static bank account, it exists as a “deposit token” on a blockchain that can be used as collateral or programmed to execute payments automatically. This “rewires” cash economics by making every dollar “smarter” and more productive, but it also shifts the focus of governance from supervising people to supervising algorithms and entitlements.