The Consolidated Omnibus Budget Reconciliation Act (COBRA) remains a cornerstone of the American social safety net in 2026, providing a critical bridge for individuals transitioning between employment cycles. This federal mandate requires most group health plans to offer a temporary extension of health coverage—at the full cost to the participant—when coverage would otherwise be lost due to specific qualifying events. As the healthcare landscape becomes increasingly fragmented with the rise of nomadic work and gig-economy structures, the technical execution of COBRA elections has become a high-stakes administrative process. Understanding the statutory obligations of the plan sponsor and the precise rights of the qualified beneficiary is essential to avoiding costly gaps in medical protection.

In 2026, the strategic value of COBRA is often weighed against the availability of subsidized plans through the Affordable Care Act (ACA) Marketplace. While COBRA allows for the seamless continuation of the exact same network of providers and deductible accumulation, it is frequently the more expensive option because the employer typically ceases to contribute toward the premium. Consequently, the decision to elect COBRA must be predicated on a forensic analysis of one’s current medical consumption, the status of met deductibles, and the specific limitations of alternative “Special Enrollment Period” (SEP) options. A failure to navigate these timelines with precision can lead to a “permanent” loss of coverage options until the next general open enrollment period.

Furthermore, the regulatory oversight by the Department of Labor (DOL) regarding COBRA notices has intensified. Plan administrators are now held to a rigorous standard of clarity, ensuring that election notices are not only delivered on time but are also “easily comprehensible” to the layperson. This includes detailed disclosures regarding the impact of COBRA election on future Marketplace eligibility. For the beneficiary, this means that the documentation received upon termination of employment is not merely a formality but a legally binding framework that dictates their healthcare trajectory for the subsequent 18 to 36 months.

Qualifying Events and the Multi-Tiered Notification Timeline

The trigger for COBRA eligibility is the occurrence of a Qualifying Event, which, combined with a loss of coverage, creates the right to elect continuation. For employees, the most common triggers are voluntary or involuntary termination (except for “gross misconduct”) and a reduction in hours that falls below the plan’s eligibility threshold. For dependents, events such as the death of the covered employee, divorce, or a child “aging out” at 26 create independent election rights. In 2026, the technical distinction between a “termination” and a “reduction in hours” is particularly relevant for employees moving to part-time roles while seeking to retain high-tier corporate health benefits.

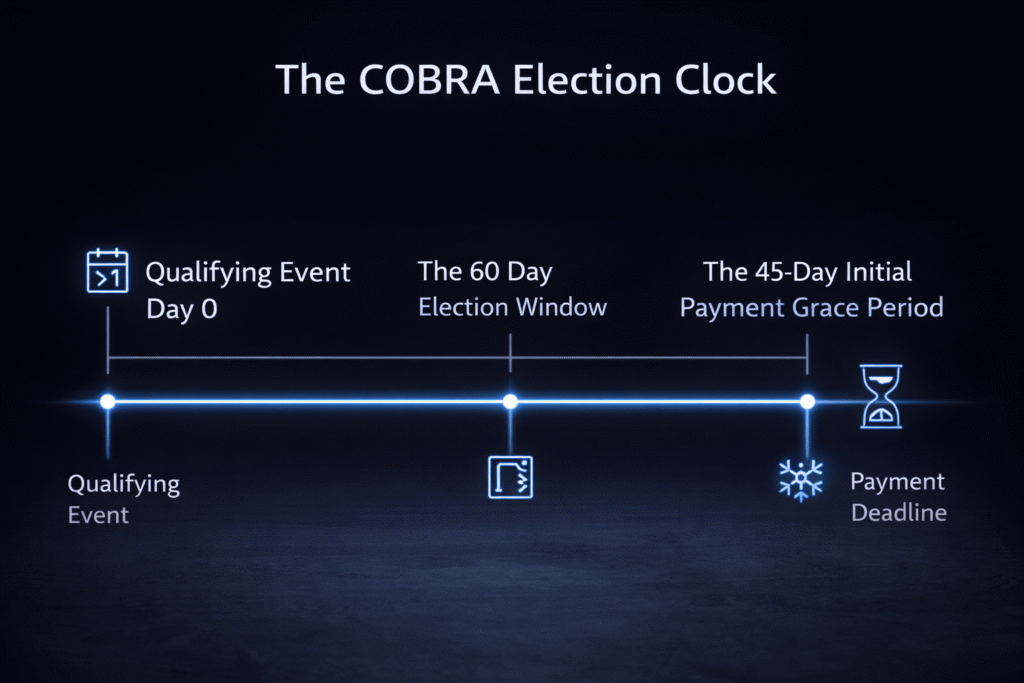

The timeline for COBRA is governed by a strict 60-day election window, which begins on the later of the date the qualifying event occurs or the date the COBRA Election Notice is provided. Once an election is made, the participant has an additional 45 days to make the initial premium payment. This “grace period” logic is often misunderstood; while coverage is retroactive to the date of loss, insurers will typically suspend claim payments until the first premium is received. This creates a temporary “shadow period” where a participant is technically covered but may face point-of-service challenges at pharmacies or hospitals until the administrative activation is reflected in the carrier’s system.

Secondary qualifying events can extend the initial 18-month coverage period to a total of 36 months. For instance, if a former employee is on COBRA due to termination and then passes away or gets divorced during that 18-month window, their covered dependents may be entitled to an extension. This requires the qualified beneficiary to notify the plan administrator within 60 days of the secondary event. In the 2026 regulatory environment, the IRS and DOL closely monitor these extensions, as they represent a prolonged liability for the group health plan’s risk pool.

Premium Calculations and the 2% Administrative Surcharge Logic

The cost of COBRA is perhaps its most daunting feature, as the participant is usually responsible for 102% of the total plan premium. This includes both the portion previously paid by the employee and the portion subsidized by the employer, plus a 2% administrative surcharge permitted under federal law to cover the costs of managing the continuation of the policy. In the case of a Disability Extension, the surcharge can legally increase to 50% for the 19th through the 29th month of coverage, reflecting the increased actuarial risk associated with long-term disability beneficiaries.

To visualize the fiscal impact of these choices in 2026, consider the following comparison of average monthly costs and network flexibility:

| Coverage Metric | COBRA (Group Plan) | ACA Marketplace (Silver Plan) | Short-Term Limited Duration |

| Monthly Premium | 102% of Total Cost | Subsidized (based on income) | Low / Non-Subsidized |

| Provider Network | High (Existing Network) | Moderate (Varies by State) | Low / Restricted |

| Deductible Status | Carries Over | Resets to Zero | N/A (New Policy) |

| Max Duration | 18–36 Months | Unlimited (while eligible) | < 12 Months |

While the ACA Marketplace often offers lower premiums through “Premium Tax Credits,” COBRA remains the technically superior choice for individuals who have already met their Annual Out-of-Pocket Maximum, as a switch to a Marketplace plan would effectively reset all cost-sharing accumulators to zero.

The “initial payment” requirement is a frequent point of technical failure. This first payment must cover the entire period from the loss of coverage up to the current month. If a participant waits until the 45th day of their election period to pay, they may find themselves responsible for three or four months of premiums simultaneously. In 2026, many automated payroll and benefit systems are programmed to terminate the COBRA right immediately if the initial payment is short by even a nominal amount, making exact balance reconciliation a mandatory task for the beneficiary.

Disability Extensions and Social Security Integration

A critical but often overlooked technical nuance of COBRA is the Disability Extension. If a qualified beneficiary is determined by the Social Security Administration (SSA) to have been disabled at any time during the first 60 days of COBRA coverage, they (and their covered family members) may be eligible for an additional 11 months of coverage, totaling 29 months. This 29-month period is specifically designed to align with the Medicare waiting period, providing a continuous thread of coverage until the individual becomes eligible for federal healthcare due to their disability.

To secure this extension, the beneficiary must provide the plan administrator with a copy of the SSA Determination Letter within 60 days of its issuance and before the initial 18-month COBRA period expires. In 2026, the integration between the SSA and private insurers has become more digitized, yet the manual notification requirement remains a statutory hurdle. If the beneficiary fails to provide the letter within the 60-day window, the plan is not legally obligated to grant the extension, regardless of the severity of the medical condition.

Furthermore, if the SSA later determines that the individual is no longer disabled, the beneficiary is required to notify the plan administrator within 30 days of that determination. The extra 11 months of coverage can then be terminated. This highlights the “temporary” nature of the disability extension and the need for constant regulatory alignment between federal disability status and private insurance continuation rights.

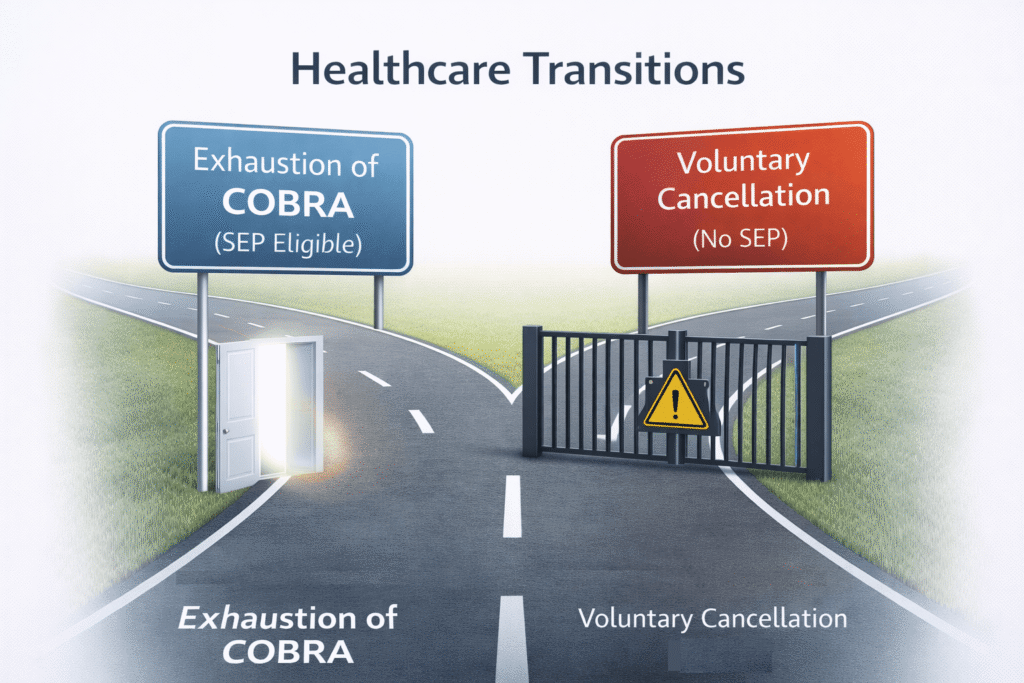

Termination Nuances: Exhaustion vs. Voluntary Cancellation

There is a profound legal difference between “exhausting” COBRA and “voluntarily canceling” it. If a participant reaches the end of their 18 or 36-month period, this is considered exhaustion of benefits, which triggers a Special Enrollment Period (SEP) for the ACA Marketplace. However, if a participant stops paying their premiums or chooses to cancel COBRA mid-stream because they found it too expensive, this does not typically qualify as a “loss of coverage” for SEP purposes. This technical distinction can leave an individual uninsured and unable to purchase a new plan until the next January.

The “timely payment” rule is the most common cause of involuntary termination. After the initial payment, subsequent premiums are due on the first of the month, though federal law mandates a 30-day grace period. In 2026, the IRS has clarified that if a payment is “insignificant” (often defined as the lesser of $50 or 10% of the premium), the plan must either accept it or provide the participant a reasonable time to pay the difference. However, relying on this “insignificance” rule is a high-risk strategy, as carrier-level terminations are often automated and difficult to reverse once a lapse is recorded.

To avoid the pitfalls of benefit termination, beneficiaries should maintain a checklist of compliance triggers. The following factors can lead to the immediate cessation of COBRA rights:

- Failure to make a full and timely premium payment within the grace period.

- The employer ceases to provide any group health plan to any of its employees.

- The participant becomes covered under another group health plan (subject to pre-existing condition rules).

- The participant becomes entitled to Medicare benefits (Part A or B) after electing COBRA.

- The participant engages in fraud or conduct that would justify termination for a similarly situated active employee.

FAQ: Healthcare Portability and Regulatory Compliance

Can an employer offer a “COBRA Subsidy” as part of a severance package without violating non-discrimination rules under the ACA?

Yes, but with caveats. In 2026, employers often provide “subsidized COBRA” for a set number of months (e.g., 6 months of premiums paid by the company). While this is a common benefit, it must be structured carefully to avoid violating Internal Revenue Code Section 105(h). If the subsidy is only offered to “highly compensated individuals,” it may create a taxable event for those employees. Furthermore, the COBRA notice must clearly state when the employer subsidy ends and when the employee’s 102% payment obligation begins to ensure there is no lapse in coverage due to administrative confusion.

How does “Open Enrollment” within the former employer’s group plan work for a COBRA participant?

Qualified beneficiaries have the same rights as active employees during the annual Open Enrollment period. This means a COBRA participant can switch between different health plan options (e.g., moving from an HMO to a PPO), add or drop dependents, and benefit from any changes in the plan’s design. This is a critical technical right in 2026, as it allows a participant to “shop” within the employer’s menu of plans to find a lower premium option while still maintaining the continuity of their COBRA election.

If I move to a different state while on COBRA, can my coverage be terminated if my current plan’s network does not exist in my new location?

This is a “localized network” issue. COBRA requires the employer to provide the same coverage that is available to similarly situated active employees. If the employer has employees in your new location and offers a plan there, you may be entitled to switch to that “regionally appropriate” plan. However, if the employer only operates in your old location and you move out of the service area, the plan is not necessarily required to provide a different network. In such cases, the move itself would trigger a Special Enrollment Period for the Marketplace in your new state, which is often the more practical solution.

Is it possible to “waive” COBRA and then change my mind later?

Yes, provided it is done within the 60-day election window. If you waive COBRA in writing but then decide you need it (perhaps due to an unexpected medical event), you can revoke your waiver and elect coverage as long as the 60 days have not passed. However, in this scenario, the coverage is not retroactive to the date of the waiver; it only becomes effective starting from the date you revoked the waiver and elected coverage, potentially creating a “gap” in coverage for the days between the waiver and the election.