The Employee Retention Tax Credit (ERTC) has transitioned from a pandemic-era relief measure into a significant regulatory battlefield in 2026. As the IRS intensifies its enforcement efforts, the focus has shifted from initial claim processing to the rigorous substantiation of eligibility during multi-year audit cycles. For organizations that utilized this credit to maintain their payroll during periods of economic instability, the current landscape demands a sophisticated understanding of the statutory limitations and the technical evidence required to survive a federal inquiry. The complexity of these audits is compounded by the retroactive nature of the review, where documentation must accurately reflect operational realities from years prior.

The primary challenge in 2026 is the recalculation of qualified wages in light of updated regulatory interpretations and judicial precedents. The IRS has moved beyond simple arithmetic checks, now employing advanced data analytics to identify “red flag” patterns in payroll data that suggest overclaiming or improper aggregation of related entities. Consequently, the burden of proof remains firmly on the taxpayer to demonstrate not only that they met the financial thresholds but that their internal controls were sufficient to prevent the double-counting of wages also funded by other federal programs. This necessitates a forensic approach to record-keeping that transcends basic accounting practices.

Navigating the limitations period for ERTC audits—which was specifically extended for certain quarters—requires a proactive defense strategy. Taxpayers must recognize that a processed refund is not a final determination of eligibility. In the current enforcement climate, the IRS is prioritizing “high-risk” claims, which include those filed by large employers or those utilizing complex “partial suspension” arguments. Professional stakeholders must therefore ensure that their contemporaneous records are not only preserved but organized in a manner that can be quickly distilled into a technical memorandum for an examining agent.

Deciphering the “Full or Partial Suspension” Technical Standard

One of the most litigated aspects of the ERTC is the definition of a partial suspension of operations due to a government order. In 2026, the technical standard for “partial suspension” requires more than a mere inconvenience; it demands proof of a nominal effect on business operations that can be directly traced to a specific federal, state, or local mandate. General voluntary shifts in consumer behavior or supply chain disruptions that were not the direct result of a government order are increasingly being rejected as valid grounds for eligibility. This distinction is critical, as the IRS looks for a clear causal link between the regulatory restriction and the specific operational decline.

The technical analysis of “nominal effect” typically hinges on whether the restricted portion of the business accounted for at least 10% of total gross receipts or 10% of the total hours of service performed by employees in a comparable prior period. In a 2026 audit environment, providing a narrative description of the impact is insufficient. Organizations must produce time-and-motion studies or detailed departmental revenue breakdowns that quantify the exact impact of the suspension on their unique business model. This level of granularity is essential to rebut the presumption that the business was able to continue comparable operations through telework or other modifications.

The legal threshold for a partial suspension is not met by a general decline in economic activity, but by a specific, mandatory government restriction that physically or operationally constrained the taxpayer’s ability to provide goods or services.

Furthermore, the “duration of the suspension” is a frequent point of contention. A claim is only valid for the specific period the government order was in effect. In 2026, the IRS is cross-referencing claim dates with jurisdictional databases of executive orders to identify periods where claims were filed after restrictions had been lifted. This temporal accuracy is the cornerstone of a defensible ERTC position, and any misalignment can lead to the immediate invalidation of the entire claim quarter and the assessment of accuracy-related penalties.

Quantitative Analysis of Gross Receipts Diminution

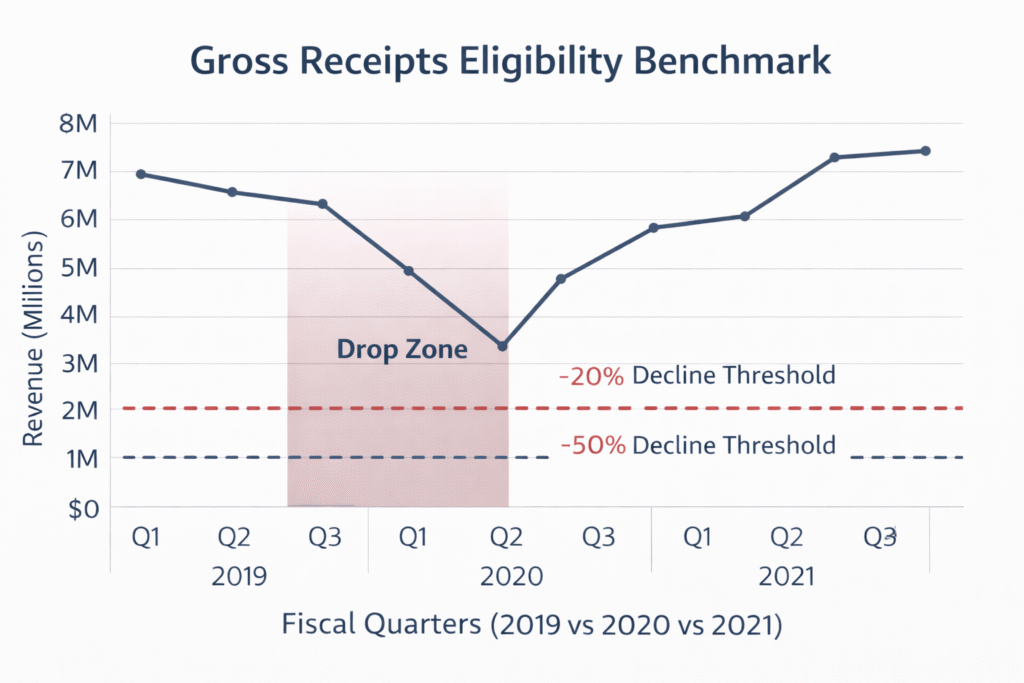

For many claimants, eligibility was established through the Significant Decline in Gross Receipts test. This purely quantitative path is often viewed as “safer” than the suspension argument, yet it carries its own technical pitfalls. In 2026, the definition of gross receipts for ERTC purposes must align strictly with Section 448(c) of the Internal Revenue Code, which includes total sales, all amounts received for services, and income from investments, regardless of the accounting method used. Miscalculating these figures by omitting non-operating income is a common technical error that can inadvertently push a taxpayer above the eligibility threshold.

The comparison typically involves measuring a 2020 or 2021 calendar quarter against the same quarter in 2019. To aid in the technical assessment of these windows, the following table outlines the Required Percentage Decline for different claim periods:

| Claim Year | Comparison Quarter | Eligibility Threshold (Decline) | Recovery Startup Business Cap |

| 2020 | Same Quarter 2019 | > 50% Reduction | N/A |

| 2021 (Q1, Q2, Q3) | Same Quarter 2019 | > 20% Reduction | $50,000 per Quarter |

| 2021 (Q4 – RSB Only) | N/A | Variable / Startup Rules | $50,000 Total |

A sophisticated maneuver often utilized by tax professionals is the Immediate Preceding Quarter Election. This allows a taxpayer to determine eligibility for a current quarter based on the gross receipts of the quarter immediately prior. In an audit scenario, the IRS will scrutinize the consistency of this election across all filed quarters. If a taxpayer switched methods to maximize the credit without proper documentation of the election, the recalculation risk becomes substantial, often resulting in a partial clawback of the credit plus interest.

The treatment of affiliated groups and “controlled groups” remains a high-density area of concern. Under the Aggregation Rules, all entities with common ownership must be treated as a single employer when testing for gross receipts. This means a decline in one subsidiary cannot be used to claim the credit if the consolidated group as a whole did not meet the reduction threshold. In 2026, the IRS is aggressively using entity mapping software to uncover undisclosed affiliations, making the “single employer” analysis a mandatory component of any ERTC compliance folder.

Interaction Between PPP Forgiveness and Qualified Wage Aggregation

The “no double-dipping” rule is perhaps the most rigid constraint in the ERTC framework. Wages used to justify Paycheck Protection Program (PPP) loan forgiveness cannot be used as qualified wages for the ERTC. This requires a meticulous “wage-to-program” mapping, where every dollar of payroll is assigned to a specific bucket. In a 2026 audit, the IRS will request the PPP Forgiveness Application (Form 3508) and compare the payroll costs reported there against the wages claimed for the tax credit. If the data is not reconciled, the IRS will default to assigning wages to the PPP first, often wiping out the ERTC eligibility for those specific weeks.

To optimize the remaining credit, technical experts utilize a strategy of “Excess Wage Identification.” This involves identifying non-payroll costs (such as rent, utilities, and operations expenditures) that were used for PPP forgiveness to “free up” more payroll for the ERTC. However, this re-allocation can only be done if the non-payroll costs were included on the original, filed forgiveness application. One cannot retroactively change the composition of the PPP forgiveness request during an ERTC audit. This highlights the importance of the original filing strategy and the permanence of the data submitted to the Small Business Administration.

Beyond PPP, other credits such as the Work Opportunity Tax Credit (WOTC) and Research and Development (R&D) credits must also be excluded from the ERTC calculation. The technical coordination of these various incentives requires a centralized payroll ledger that tracks each employee’s eligibility for different credits simultaneously. In 2026, the absence of such a ledger is often viewed by auditors as a sign of “negligent record-keeping,” which can escalate a standard audit into a more intensive examination of the taxpayer’s entire tax return.

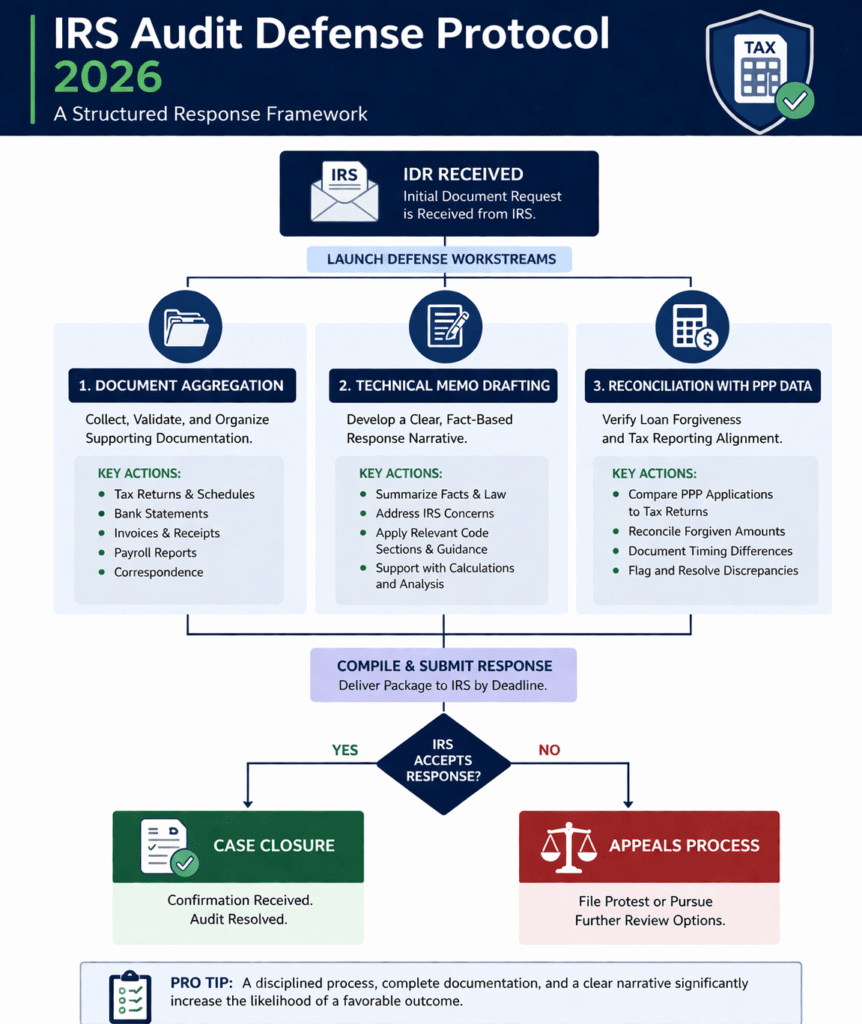

Mitigation Strategies for IRS Information Document Requests

When an audit begins, the IRS issues an Information Document Request (IDR), which serves as the roadmap for the examination. A technical and timely response to an IDR is the most effective way to limit the scope of the audit. In 2026, these requests are increasingly standardized, asking for payroll registers, government orders, and detailed workpapers. Providing a disorganized “document dump” is a strategic error; instead, the response should be a indexed compliance binder that leads the auditor through the eligibility logic, quarter by quarter.

The quality of the medical and legal research supporting a suspension claim is often the deciding factor in a successful defense. If a business was a “supplier” to an essential business and was impacted by their closure, the documentation must show a nominal disruption to the taxpayer’s own operations, not just the customer’s. This often requires third-party affidavits or shipping logs to prove that the “bottleneck” was insurmountable. Without this secondary evidence, the IRS will likely conclude that the business could have sourced materials elsewhere, thereby negating the suspension claim.

To ensure a robust defense, the compliance folder should contain a specific set of Technical Substantiation Artifacts:

- Copies of the specific Government Orders (State/Local) that mandated the suspension.

- A “Nominal Effect” memorandum with revenue-by-department spreadsheets.

- Detailed payroll records identifying qualified wages by employee and by day.

- Health insurance plan documents and proof of payment for qualified health plan expenses.

- A copy of the PPP Forgiveness Letter and the underlying application workpapers.

If the audit results in a proposed adjustment, the taxpayer has the right to appeal through the IRS Independent Office of Appeals. In 2026, the success rate at Appeals often depends on the taxpayer’s ability to present “newly discovered” evidence or a more refined legal interpretation of the suspension rules. However, the best outcome is always to close the audit at the examination level by providing such a dense and technically sound response to the initial IDR that the auditor finds no grounds for a deficiency.

FAQ: Advanced Tax Credits and Compliance

How does the “Aggregated Group” rule apply to entities that were acquired or sold mid-quarter during the 2021 claim periods?

In 2026, the IRS applies the “Successor Employer” and “Common Control” rules with high precision. When an acquisition occurs, the gross receipts of the acquired entity must typically be included in the consolidated group’s test for the entire quarter, including the pre-acquisition period, to ensure a consistent year-over-year comparison. If the acquisition resulted in a change in the controlled group’s status, the re-testing of the 20% decline must be performed using the combined 2019 data of both entities as the baseline, preventing the “artificial” creation of eligibility through corporate restructuring.

Under what circumstances can “Qualified Health Plan Expenses” be claimed as ERTC wages if the employees were furloughed and received no cash wages?

While the ERTC generally requires the payment of wages, a significant technical exception exists for health plan expenses. If an employer continued to provide health insurance to furloughed workers during a qualifying period of suspension or revenue decline, the employer’s portion of the premiums (and potentially the pre-tax employee portion) can be treated as qualified wages. This holds true even if the employee’s cash compensation was zero, provided the expenses are allocated to the period of leave. This is a vital “high-value” insight for businesses in the 2026 audit cycle that may have overlooked these non-cash costs.

What is the impact of the “Statute of Limitations” extension on the assessment of interest and penalties for ERTC clawbacks in 2026?

The American Rescue Plan Act of 2021 extended the statute of limitations for the IRS to assess taxes related to the ERTC to five years for certain quarters (specifically Q3 and Q4 of 2021). This means that even in 2026, the IRS remains within the legal window to audit and recapture these funds. If a credit is invalidated, the taxpayer is liable for the underpayment of employment taxes, which triggers interest from the original due date of the return. Furthermore, if the IRS determines the claim lacked a “reasonable basis,” a 20% accuracy-related penalty under Section 6662 is frequently applied, making the total cost of an unsuccessful audit significantly higher than the original credit received.