Contrary to long-standing fears of a 2026 “tax cliff,” the recently enacted One Big Beautiful Bill Act (OBBBA) has made the Child Tax Credit permanent and expanded it to $2,200 per child, providing a new level of certainty for American families.

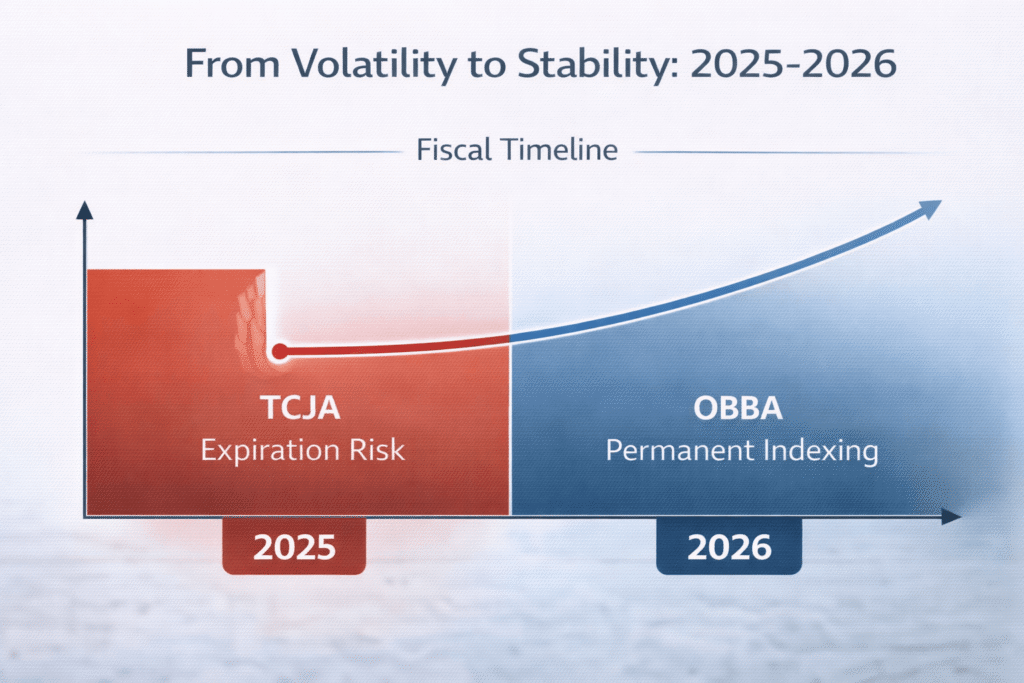

The fiscal landscape of 2026 is defined by the successful implementation of the OBBBA, a legislative landmark that effectively neutralized the much-feared “Tax Cliff” of late 2025. Following the expiration of the Tax Cuts and Jobs Act (TCJA) provisions, American families faced a technical regression to pre-2017 credit levels, which would have slashed the Child Tax Credit (CTC) by half and reinstated restrictive refundability caps. The OBBBA intervened by permanently codifying an enhanced CTC structure, ensuring that the credit remains a robust tool for middle-class stability and poverty reduction in an era of stabilized but elevated living costs.

Unlike previous temporary expansions, the 2026 framework provides a long-term predictable baseline for tax planning. By decoupling the credit from the volatile annual appropriations process, the new law has allowed the IRS to build a more sophisticated distribution infrastructure. This technical stability is vital for households that rely on the CTC not just as a year-end windfall, but as a calculated component of their annual net liquidity. In 2026, the credit is fully indexed to inflation, meaning the maximum per-child amount is automatically adjusted without requiring additional legislative intervention, a critical safeguard for the purchasing power of young families.

Furthermore, the 2026 updates have addressed the “administrative friction” that previously plagued taxpayers with complex filing statuses. The OBBBA simplified the definitions of qualifying children and residency requirements to align more closely with other federal benefits like the EITC (Earned Income Tax Credit). This synchronization reduces the likelihood of automated IRS audits and “math error” notices, which were the leading causes of refund delays in previous cycles. For the 2026 tax season, the focus has shifted from mere “eligibility” to the optimization of the credit through the newly enhanced IRS digital ecosystem.

Refundability and the “Full Credit” Architecture

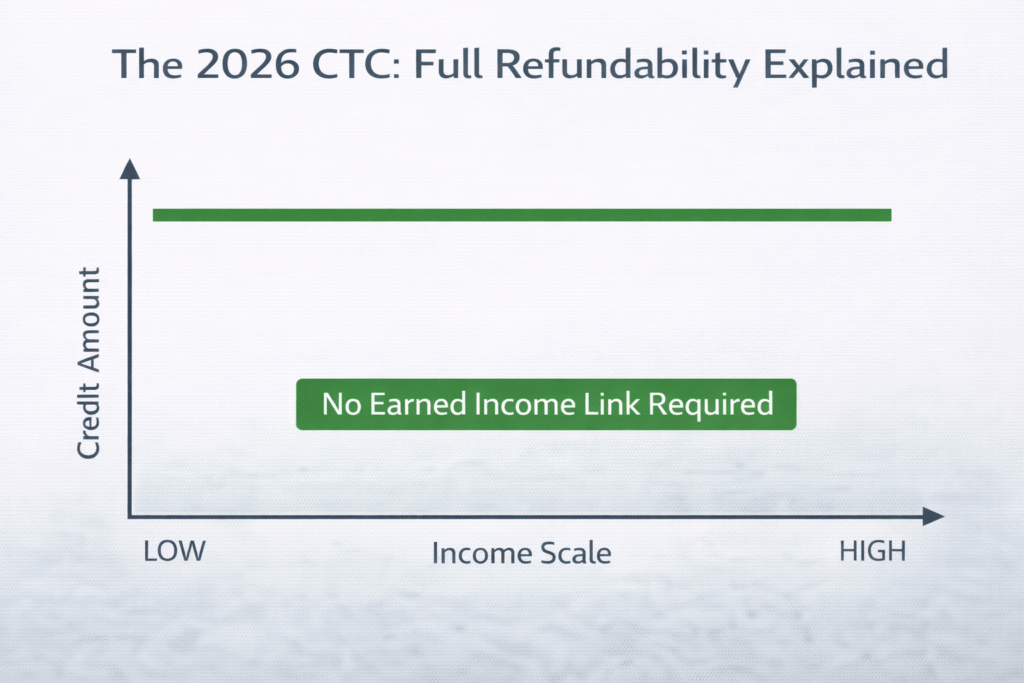

The most significant technical achievement of the OBBBA in 2026 is the permanent establishment of Full Refundability. Historically, the CTC was limited by an “earned income formula,” which meant that the lowest-income families—those who arguably needed the support most—were technically disqualified from receiving the full value of the credit because they didn’t earn enough to trigger the refund. In 2026, this barrier has been completely removed. The credit is now “fully refundable,” meaning a family receives the entire per-child amount even if their tax liability is zero, effectively turning the CTC into a guaranteed floor of support for every qualifying child.

The permanent shift to full refundability in 2026 represents a fundamental change in the American social contract, ensuring that a child’s access to nutritional and developmental resources is no longer technically tethered to their parents’ current tax liability.

This change eliminates the need for the complex “Phase-in” calculation that utilized the 15% earned income threshold. In the 2026 system, the credit is treated as a direct investment rather than a tax offset. This technical nuance is particularly important for households experiencing temporary unemployment or those in the “gig economy” with fluctuating annual revenues. By removing the earned income link, the OBBBA has made the CTC a reliable counter-cyclical tool that maintains its value even during personal or national economic downturns.

From a compliance perspective, the removal of the refundability cap simplifies the Form 1040 significantly. Taxpayers no longer need to navigate the labyrinth of Schedule 8812 to calculate the “Additional Child Tax Credit” (ACTC), as the distinction between the non-refundable and refundable portions has been technicaly abolished. This streamlining not only reduces the cost of professional tax preparation for low-income families but also allows the IRS to process refunds with higher algorithmic speed, as the primary variable—earned income—is no longer a gating factor for the credit’s payout.

Finally, the 2026 architecture ensures that this refundability is protected from “benefit offsetting.” In many states, federal refunds were previously subject to various intercepts for state-level debts. However, under the OBBBA’s 2026 protections, the enhanced portion of the CTC is technically shielded from most administrative offsets, ensuring that the funds reach the household for their intended purpose: the support and care of the child. This protection is a key pillar of the 2026 financial security model for American families.

The 2026 Phase-out Calculus: Protecting Middle-Class Benefits

While the OBBBA expanded access for the lowest earners, it also recalibrated the “Phase-out Calculus” for high-income households to ensure the program’s long-term fiscal sustainability. In 2026, the credit remains generous for the middle class, but it begins to technically diminish once a taxpayer’s Adjusted Gross Income (AGI) crosses specific thresholds. This reduction is not a “cliff” but a gradual taper, designed to avoid the sharp marginal tax spikes that can occur when a small raise leads to a large loss of benefits.

The technical formula used by the IRS in 2026 to calculate the reduced credit (C) for households exceeding the AGI threshold is expressed as:

In this formula, Cmax is the maximum credit per child (adjusted for 2026 inflation), and the “Threshold” is determined by the taxpayer’s filing status. For most families, this means that for every $1,000 of income earned over the limit, the total credit is reduced by $50. Because the thresholds in 2026 are set high—typically starting at $200,000 for single filers and $400,000 for married couples filing jointly—the vast majority of American families continue to receive the full, unreduced benefit.

Strategically, this phase-out structure rewards “incremental earning.” Because the taper is gradual, parents can accept promotions or overtime without fearing a technical “net loss” in their total household income. For tax planners in 2026, the focus is often on utilizing pre-tax contributions—such as 401(k) or HSA deposits—to lower the AGI just enough to stay below the phase-out threshold. This “threshold management” is a common 2026 strategy for households on the edge of the upper-middle-class bracket.

Comparison of Tax Eras: Stability vs. Volatility

The technical superiority of the 2026 OBBBA framework is best understood when compared to the volatility of the “Tax Cliff” era. Before the current law, the tax code was a patchwork of expiring provisions that forced families into a cycle of fiscal uncertainty. In 2025, without a legislative deal, the credit would have technically reverted to only $1,000 per child, with a significant portion being non-refundable, potentially pushing millions of children back into poverty.

The 2026 standards have replaced this uncertainty with a permanent, indexed model. By looking at the technical specifications of the current law versus previous eras, we can see how the OBBBA prioritized both the amount of the credit and the ease of access.

| Feature | Pre-2025 (TCJA) | The 2025 “Cliff” (No Deal) | OBBBA (2026 Reality) |

| Max Credit | $2,000 | $1,000 | ~$3,000+ (Indexed) |

| Refundability | Limited (Partial) | Highly Limited | Fully Refundable |

| Income Link | Required Earned Income | Required Earned Income | No Link Required |

| Age Limit | Under 17 | Under 17 | Under 18 |

| IRS System | Legacy Manual Audit | Legacy Manual Audit | IRS Direct File Sync |

Filing Synergy: Integrating the CTC with IRS Direct File 2026

For the 2026 tax season, the IRS has fully integrated the Child Tax Credit into the IRS Direct File platform. This free, government-run filing system has moved beyond its pilot phase and is now the standard recommendation for families with straightforward W-2 income and CTC claims. The technical synergy between the IRS databases and the Direct File interface allows for “pre-verification” of qualifying children, which virtually eliminates the “Dependency Disputes” that used to delay refunds for weeks.

The 2026 Direct File system uses a “Step-Up Verification” process. If a child was claimed on the previous year’s return and the social security data matches, the system technically “green-lights” the credit for immediate processing. This integration is part of a larger federal push to treat tax credits more like digital transfers and less like traditional tax reconciliation. For the user, this means that the time from “Click to Cash” has been technically reduced to an average of 7 to 10 business days for those choosing direct deposit.

Furthermore, the 2026 system is designed to catch “missed credits.” If a taxpayer’s data suggests they have a qualifying child but they haven’t claimed the CTC, the Direct File algorithm will technically prompt the user to review the eligibility criteria. this proactive “nudge” architecture is a key reason why the 2026 participation rate for the CTC has reached record highs. By removing the need for expensive third-party software to navigate the CTC rules, the IRS has technically lowered the cost of compliance for the entire American population.

FAQ: Advanced CTC Tax Planning

What happens if my child turns 18 during the 2026 tax year?

Under the 2026 OBBBA rules, the “age-out” threshold has been technically standardized. To qualify for the full CTC, the child must be under the age of 18 for at least one day of the tax year. If your child turns 18 in 2026, they no longer qualify for the standard CTC, but they may still qualify for the Credit for Other Dependents (ODC), which provides a smaller, non-refundable credit. This is a common technical trap for parents of high school seniors, and it is vital to adjust your 2026 withholding to account for this $3,000+ drop in credit value.

Can both parents claim the CTC in 2026 if they are divorced?

No. The IRS has a strict “one-child, one-credit” rule. In 2026, the credit technically belongs to the custodial parent—the one with whom the child lived for more than half the year. However, the custodial parent can technically “waive” the credit to the non-custodial parent by signing IRS Form 8332. If both parents attempt to claim the child without this form, the 2026 automated audit system will freeze both refunds until a manual residency verification is completed.

How does the 2026 CTC affect my eligibility for SNAP or SSI?

This is a critical technical protection: Under federal law, the Child Tax Credit is not considered income for the purpose of determining eligibility for means-tested programs like SNAP, SSI, or Medicaid. Receiving a $3,000 CTC refund in 2026 will not cause a “benefit cliff” or lead to a reduction in your other assistance. However, it is important to remember that if the refund is not spent and remains in your bank account for more than 12 months, it may technically begin to count toward the “asset limits” of programs like SSI.

Is the 2026 Child Tax Credit subject to the “Child Support Offset” program?

Yes. While the OBBBA protected the CTC from many administrative offsets, it did not exempt it from past-due child support collections. If the IRS receives a notice from a state child support agency that a taxpayer is in arrears, the 2026 CTC refund can technically be “intercepted” to pay those obligations. This process is automated, and taxpayers usually receive a “Notice of Offset” explaining exactly how much of their CTC was diverted to the state agency.

What is the “Direct File Sync” feature for 2026 state tax returns?

One of the most useful technical updates in 2026 is the ability to synchronize your federal CTC data with your state tax return through the IRS Direct File interface. Since many states now have their own “State Child Tax Credits” that mirror the federal eligibility rules, this sync feature ensures that you don’t have to enter the same data twice. This “Single-Entry Compliance” model is a key feature of the 2026 effort to reduce the “tax-time burden” for American families.