The 2026 landscape for Supplemental Security Income (SSI) has been fundamentally reshaped by major regulatory shifts that eliminate historic “food penalties” and streamline the path to eligibility through digital modernization.

The 2026 fiscal year marks the most significant administrative transformation of the SSI program since its inception in 1974. Following a series of regulatory overhauls enacted by the Social Security Administration (SSA) between 2024 and 2025, the program has reached a state of technical maturity that prioritizes beneficiary stability over punitive auditing. The core of this modernization lies in the systemic deconstruction of In-Kind Support and Maintenance (ISM) rules, which historically penalized recipients for receiving basic help from family or friends. For the over 7 million Americans relying on SSI in 2026, these changes represent a vital shift toward economic inclusion and administrative transparency.

Historically, the SSI program was notorious for its intrusive “living arrangement” audits, which required beneficiaries to report every meal or grocery bag provided by outside sources. In 2026, the SSA has officially pivoted away from this model, recognizing that the “administrative friction” caused by these micro-audits often cost the government more in labor hours than it saved in benefit reductions. This shift is part of a broader federal effort to synchronize the SSI program with other modern welfare initiatives, moving toward a “trusted data” model where the SSA utilizes automated electronic verification rather than manual, paper-based self-reporting.

Furthermore, the 2026 updates have addressed the “marriage penalty” and “cohabitation friction” that once plagued the system. By simplifying how the SSA evaluates shared living expenses, the agency has made it technically easier for beneficiaries to live with family members without fear of an automatic one-third reduction in their monthly checks. This is particularly crucial in the 2026 housing market, where multi-generational living has become an economic necessity for many low-income disabled individuals and seniors.

As we move through 2026, the SSA is also focusing on “active outreach” to those who are technically eligible but not yet enrolled. With the full implementation of the iApp system, the initial barrier to entry has been lowered, reducing the average application processing time by nearly 30%. This digital-first approach, combined with the new, more lenient ISM rules, ensures that SSI remains a robust and accessible safety net for the nation’s most vulnerable populations in an increasingly complex financial era.

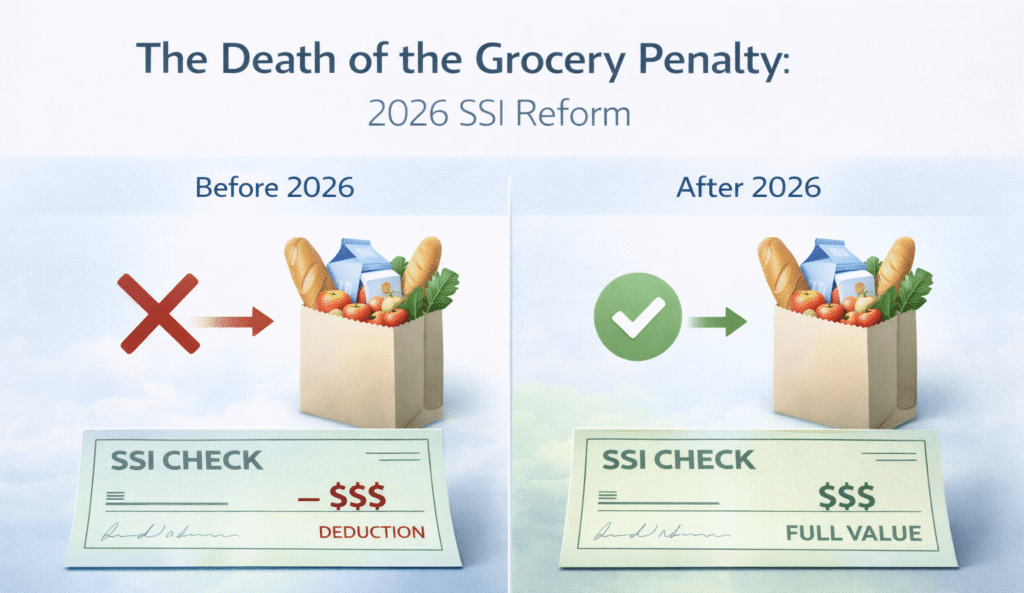

Decoupling Food from ISM: The Death of the “Grocery Penalty”

Perhaps the most celebrated technical change in 2026 is the finalized removal of food from the ISM calculation. Previously, if a family member bought groceries for an SSI recipient, that help was technically considered unearned income, triggering an automatic reduction in the recipient’s monthly benefit. In 2026, food is no longer a factor in these calculations. This means that beneficiaries can now accept meals, groceries, and dining assistance from friends or nonprofit organizations without it impacting their SSI check in any way.

The removal of food from the ISM calculation in 2026 is a milestone for dignity; it ends the “grocery penalty” and acknowledges that nutritional support from the community should not be treated as a taxable financial asset.

This decoupling has a direct impact on the Value of the One-Third Reduction (VTR) rule. Because food is no longer “countable support,” the SSA now only looks at shelter costs (rent, mortgage, property taxes, heating, and water) when determining if a recipient is receiving significant in-kind maintenance. This technical narrowing of the ISM scope simplifies the reporting process for both the beneficiary and the SSA caseworker, as the complex documentation of “grocery receipts” has been completely eliminated from the 2026 compliance handbook.

For many recipients, this change effectively acts as an “invisible raise.” By allowing families to provide nutritional support without financial penalty, the 2026 rules allow SSI checks to be dedicated entirely to other fixed costs, such as non-covered medical expenses or personal care. It is estimated that this change alone has restored the full benefit amount to over 600,000 households that were previously subject to the standard ISM reduction.

The Expanded Public Assistance Household Definition

Another technical pillar of the 2026 reform is the expansion of the “Public Assistance (PA) Household” definition. In the past, for a household to be classified as a PA household, every single member had to be receiving some form of means-tested public income. In 2026, the SSA has lowered this threshold, now requiring only one SSI recipient and at least one other member who receives a “means-tested” benefit—most notably, SNAP (Supplemental Nutrition Assistance Program).

This expansion is technically significant because if you live in a PA household, the SSA automatically assumes you are not receiving ISM from other members of the house. This assumption removes the need for the intrusive “Who pays for what?” questioning during annual redeterminations. In 2026, if you live with a roommate or family member who receives SNAP, you are technically shielded from the VTR reduction, ensuring that your SSI payment remains at the maximum allowable federal rate regardless of how household bills are split.

Nationalizing the Rental Subsidy Rule: Protecting the 2026 Benefit Floor

A major win for equity in 2026 is the national expansion of the Rental Subsidy Rule. Previously available in only seven states due to various court rulings, this rule now applies to all 50 states. It addresses the technical problem of “discounted rent.” If a beneficiary pays an amount for rent that is less than the market value—but equals or exceeds the Presumed Maximum Value (PMV)—the SSA no longer treats the “discount” as unearned income.

In practical 2026 terms, this means that if a parent charges their disabled adult child a “fair share” of the rent (based on the PMV) even if that amount is lower than what a stranger would pay, the child’s SSI check remains protected. This prevents the SSA from cutting the benefit simply because a landlord or family member is offering a charitable rate. The expansion of this rule provides a consistent national standard, ending the “geographic lottery” that previously dictated benefit amounts based on where a recipient lived.

Furthermore, this rule encourages the creation of “Business Arrangements” between family members. In 2026, as long as there is a written agreement stating that the recipient is liable for a specific portion of the rent that meets the SSA’s technical thresholds, the benefit is safe from ISM deductions. This provides a clear legal and financial framework for families to support their loved ones without inadvertently triggering a reduction in their government-provided income.

The 2026 Digital Leap: iApp and the Paperless Application Stack

The SSA has officially retired the “burden of paper” in 2026 with the full launch of the iApp (Integrated Application) platform. This new interface uses “plain language” questions and intuitive logic to guide applicants through the process, automatically skipping sections that are not relevant to their specific disability or age. In 2026, the iApp is the primary entry point for all adult SSI claims, significantly reducing the “manual entry” errors that historically led to months-long delays and technical denials.

This digital leap is supported by the paperless application stack, which allows the SSA to pull medical records and financial data directly from participating providers and banks (with the applicant’s consent). By automating the “Evidence Collection” phase, the 2026 system can often issue an initial determination in as little as 60 to 90 days. For those in urgent need, the system also identifies “Presumptive Disability” triggers more accurately, allowing the SSA to start paying benefits immediately while the final medical review is still being conducted.

The Math of SSI 2026: Calculating Your Adjusted Benefit

Understanding the 2026 SSI check requires a look at the interaction between the Federal Benefit Rate (FBR) and the Value of the One-Third Reduction (VTR). If a recipient is found to be receiving both shelter and support without paying their fair share, the SSA applies the VTR. In 2026, the formula for the VTR is technically expressed as:

Where FBR is the current Federal Benefit Rate for 2026. The $20.00 represents the “General Income Exclusion” that the SSA applies to the first twenty dollars of any unearned income. Because food has been removed from the ISM calculation, achieving the “full FBR” is technically more attainable in 2026 than in any previous year.

| Metric | 2025 Value | 2026 Adjusted Value |

| Max Individual SSI | $943 | ~$970 (Finalized) |

| Max Couple SSI | $1,415 | ~$1,455 (Finalized) |

| PMV (Presumed Max Value) | $334.33 | ~$343.33 |

| VTR (One-Third Reduction) | $314.33 | ~$323.33 |

| Asset Limit (Individual) | $2,000 | $2,000 (Unchanged) |

FAQ: Advanced SSI Compliance and Appeals

Does help with utility bills still count as ISM in 2026?

Yes. While the “grocery penalty” is gone, the SSA still considers help with shelter-related utilities (heating, water, electricity, and trash) as ISM. However, help with a cell phone bill or internet service is technically excluded. If a family member wants to help you without affecting your SSI check in 2026, paying your internet or phone bill is the most “compliance-safe” strategy, as these are not defined as essential shelter costs by the SSA.

How does an ABLE account interact with my 2026 SSI asset limit?

The asset limit for SSI remains at $2,000 for individuals in 2026. However, funds held in a Section 529A (ABLE) account are technically “invisible” to the SSA for the first $100,000. This is the ultimate technical tool for 2026 beneficiaries to save for long-term needs—such as a down payment on a home or a specialized vehicle—without losing their monthly SSI income or their Medicaid eligibility.

What is the “Business Arrangement” for rent, and how do I document it for 2026?

A Business Arrangement exists when a beneficiary agrees to pay an amount for rent that equals the PMV or the “fair market value,” whichever is less. To document this for 2026, you should have a signed, dated agreement between you and the landlord (or family member). It must state the monthly rent amount and acknowledge that you are legally obligated to pay it. Having this document on file during your 2026 redetermination is the best way to prevent an automatic one-third reduction in your benefits.

How do I report my monthly earnings in 2026 to ensure my SSI is adjusted correctly?

In 2026, the most efficient method is the SSA Mobile Wage Reporting App. This allows you to snap a picture of your pay stub and upload it directly to the SSA’s servers. By reporting by the 6th day of the following month, you ensure that the SSA adjusts your 2026 check accurately, preventing “Overpayments” that can lead to stressful collection actions and benefit suspensions later in the year.

Is SSI back pay (retroactive) taxable in 2026?

SSI payments, including large “back pay” installments, are not federally taxable. However, if you receive a large lump sum in 2026, you must be careful about the asset limit. The SSA technically gives you 9 months to spend down a retroactive SSI payment before it counts toward your $2,000 limit. Strategic use of an ABLE account or purchasing “exempt assets” (like a primary residence or a car) is the standard 2026 advice for managing these windfalls.

What is the “Direct Messaging” feature in the 2026 my Social Security portal?

Starting in 2026, beneficiaries can use the Secure Message Center in their online portal to communicate directly with their local field office. This technically replaces the need for hours spent on hold or unnecessary office visits. You can upload documents, check the status of a redetermination, or report a change of address with a digital “paper trail” that proves you met your reporting obligations on time.