In 2026, the Medicaid landscape has shifted to a permanent state of high-frequency oversight, with states facing a federal deadline to automate renewals while many beneficiaries face new six-month eligibility checks.

The healthcare landscape of 2026 is currently defined by what experts call a “permanent state of audit.” Following the transition from the chaotic post-pandemic unwinding, the federal government has institutionalized a high-frequency oversight model for Medicaid and the Children’s Health Insurance Program (CHIP). This evolution marks a decisive shift from passive eligibility to an active compliance environment, where the burden of proof has technically intensified for the nearly 90 million Americans reliant on these programs. For the average beneficiary, 2026 is no longer about a simple annual check-in; it is about navigating an automated, data-driven gauntlet that prioritizes administrative precision over long-term continuity of care.

At the heart of this operational shift is a federal mandate requiring state agencies to demonstrate full compliance with renewal requirements by the end of the 2026 fiscal year. This has led to a surge in “real-time eligibility checks,” where state systems are now technically programmed to flag even minor income fluctuations reported by third-party data aggregators. This increased pressure on state administrative infrastructures often results in a higher risk of procedural disenrollments, a technical term for losing coverage not because you are ineligible, but because the bureaucratic paperwork failed to align with the system’s new, rigid timeline.

Furthermore, 2026 has introduced a heightened level of cross-platform data synchronization. State Medicaid offices are now technically linked with unemployment portals, the Social Security Administration’s death master file, and even private-sector new-hire registries. This interconnectedness means that a seasonal bonus, a temporary second job, or a change in household composition can now trigger a redetermination notice within weeks of the event. Consequently, beneficiaries must treat their Medicaid status as a dynamic financial account that requires constant monitoring, much like a credit score or a bank balance, to avoid a sudden interruption in medical access.

Mastering the “Ex Parte” Protocol: How the System Tracks You

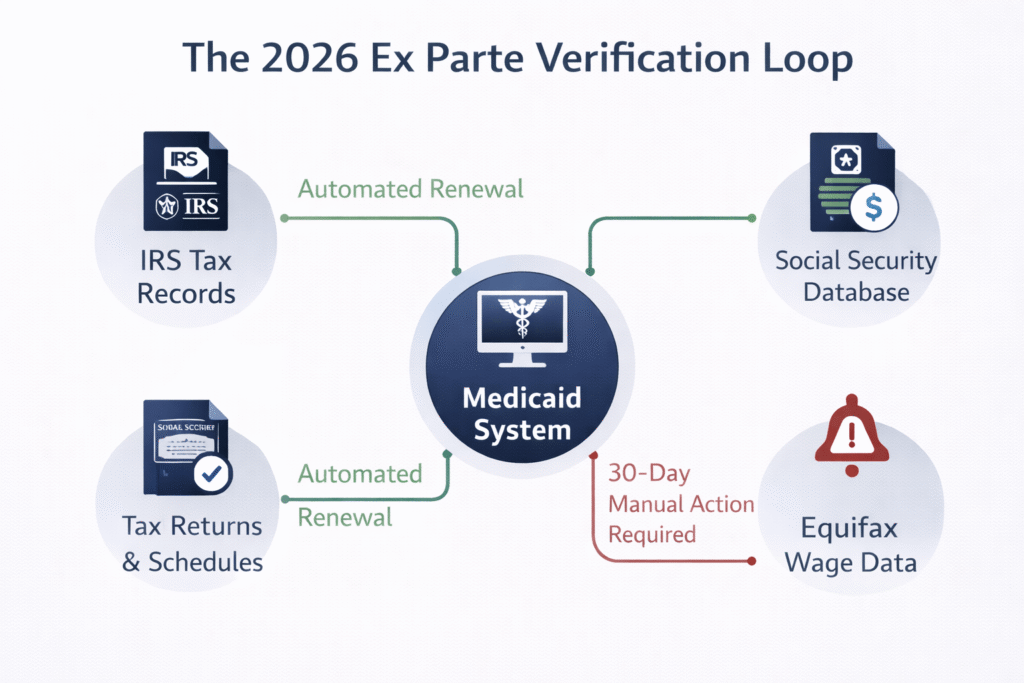

The “Ex Parte” renewal serves as the primary automated mechanism that state agencies must legally exhaust before requesting manual documentation from a beneficiary. In 2026, the technical success of an Ex Parte renewal hinges on the system’s ability to successfully verify a household’s Modified Adjusted Gross Income (MAGI) using electronic databases such as IRS tax records and the National Directory of New Hires (NDNH). If the data is consistent and falls below the 138% Federal Poverty Level (FPL) threshold common in expansion states, the coverage is renewed automatically, often without the user ever receiving more than a final confirmation notice.

However, the 2026 automated system is notably sensitive to “data mismatches” that occur when a beneficiary’s reported income on a tax return doesn’t align with more recent pay stubs flagged by the state’s labor department. These mismatches are the primary reason the Ex Parte success rate currently hovers around 60%, leaving millions to face the manual renewal process. When the algorithm fails to verify eligibility, the system automatically triggers a pre-populated renewal packet, which is mailed to the address on file. This marks the moment the beneficiary enters a “high-risk” administrative window where their coverage is no longer guaranteed by the algorithm.

In 2026, silence is the greatest threat to your health coverage; if the automated “Ex Parte” system fails due to a single data mismatch, your 30-day clock for manual verification begins immediately, regardless of whether you have physically received or opened the state’s notice.

For those in the self-employed or “gig” sectors, the 2026 Ex Parte protocol is particularly challenging. The system often struggles to calculate net income versus gross income for independent contractors, frequently leading to false “over-income” flags. To counter this, technical advisors recommend that beneficiaries proactively upload their most recent Schedule C or monthly profit-and-loss statements to their state’s online portal before their renewal month. By injecting accurate data into the system ahead of the automated check, beneficiaries can significantly increase their chances of a seamless, paperwork-free renewal.

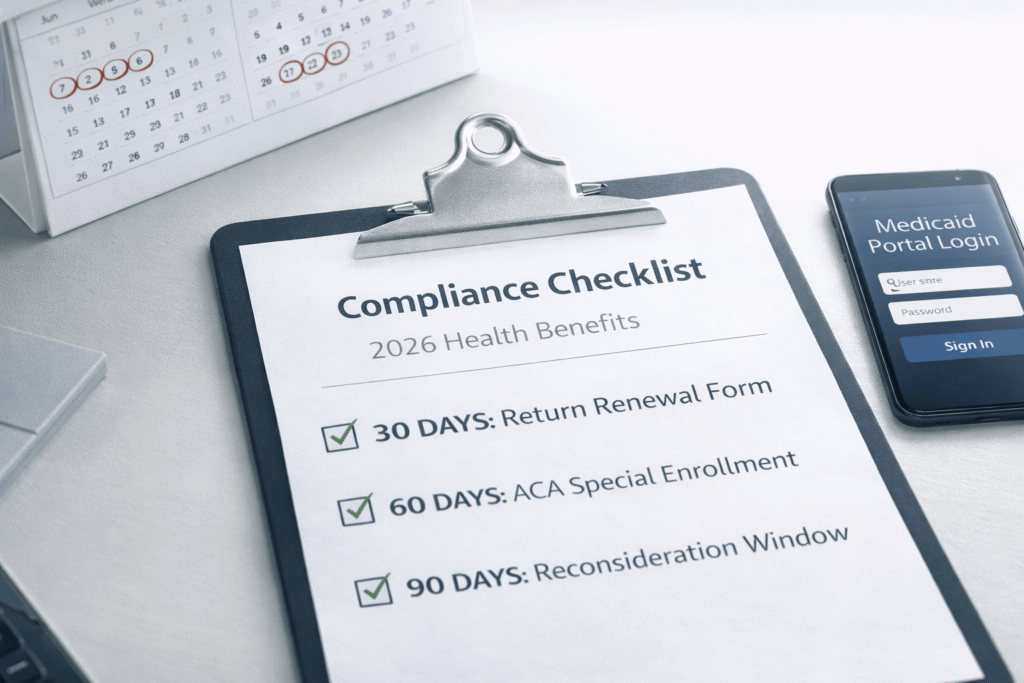

Critical Compliance Milestones: The 30, 60, and 90-Day Rule

Navigating a 2026 Medicaid redetermination notice requires a strict adherence to a specific chronological sequence. Missing even a single milestone in this technical chain can result in a coverage gap that lasts for months, potentially jeopardizing ongoing medical treatments or access to life-saving specialty drugs. In 2026, the state follows a standardized “countdown” once the manual renewal process is initiated:

- The 30-Day Response Window: Once a manual renewal packet is issued, you have exactly 30 calendar days to sign, correct, and return the form. In the 2026 digital era, many states have moved to “timestamped notifications,” meaning the 30-day clock begins the moment the notice is available in your digital inbox, often days before a physical letter arrives.

- The 60-Day Transition Window (SEP): If the state determines you are no longer income-eligible, you trigger a Special Enrollment Period (SEP). You have 60 days from the final day of your Medicaid coverage to select and enroll in a Health Insurance Marketplace (ACA) plan to avoid a total lapse in health security.

- The 90-Day Reconsideration Period: If you lose coverage for purely procedural reasons—such as failing to return a form—most states provide a technical “reconsideration window.” If you submit the required information within 90 days of losing coverage, the state can often reinstate your Medicaid retroactively, covering any medical bills incurred during the gap.

Understanding these milestones is essential because the 2026 system is largely automated and lacks the “administrative grace” found in previous years. Once the 30-day window closes without a response, the system is technically programmed to terminate the enrollment on the last day of the month. Recovery from this point is far more complex than a simple phone call; it requires a formal reconsideration or a brand-new application, both of which can take weeks to process through the state’s overburdened 2026 verification systems.

Navigating the 2026 “Subsidy Cliff” and Marketplace Transitions

For those who technically “earn their way out” of Medicaid in 2026, the transition to private insurance is significantly more expensive than in the previous three years. This is due to the official expiration of the enhanced premium tax credits that were a staple of previous federal health legislation. As of January 1, 2026, the “subsidy cliff” has returned, meaning that a modest increase in household income can now result in a disproportionately large jump in monthly premiums for Marketplace plans. For a family of four, transitioning from Medicaid to a Silver-level plan could now mean a new monthly expense of $400 to $700, representing a major technical shock to the household’s net liquidity.

Managing this transition requires a technical review of Silver-level “Cost-Sharing Reductions” (CSRs). In 2026, many individuals transitioning from Medicaid are still eligible for these CSRs, which technically lower out-of-pocket costs like deductibles and copayments. However, these benefits are only available if the user selects a Silver plan on the Marketplace. Choosing a “Bronze” plan because of a lower monthly premium can be a costly technical error, as the lack of CSRs could lead to thousands of dollars in unexpected medical expenses if a family member requires emergency care during the coverage year.

The “Network Gap”: Managing Clinical Continuity during Transition

The most significant risk during a 2026 Medicaid-to-Marketplace transition is not financial, but clinical. There is a persistent “Network Gap” where many physicians who accept Medicaid do not participate in the lower-cost private insurance networks offered on the Marketplace. For patients with complex conditions, such as cancer or chronic autoimmune disorders, this can mean a forced change of specialists mid-treatment, which can technically disrupt the therapeutic trajectory.

To mitigate this, beneficiaries must perform a “Provider Audit” before selecting their new 2026 plan. Most Marketplace portals now offer a technical search tool to see if your current doctors are “In-Network.” If a gap is identified, you can technically apply for a “Transition of Care” (TOC) waiver with the new insurance company. While not guaranteed, a TOC waiver can allow you to keep your existing Medicaid specialist for up to 90 days at the in-network rate while a permanent transition plan is established.

State-Specific Volatility: Managed Care vs. Fee-for-Service Redeterminations

The redetermination experience in 2026 varies significantly based on whether a state utilizes Managed Care Organizations (MCOs) or a traditional Fee-for-Service (FFS) model. In “Managed Care” states—such as Florida, Ohio, and Arizona—private insurance companies are technically responsible for managing the Medicaid population. In 2026, these MCOs have a vested financial interest in keeping eligible members on their rolls to maintain their capitation payments. Many have deployed sophisticated outreach technologies, including automated SMS reminders and mobile app notifications, to help members navigate the 30-day renewal window before the state triggers a disenrollment.

In contrast, “Fee-for-Service” states often rely on centralized, state-run bureaucracies that may lack the technological agility of private carriers. In these regions, the redetermination process remains heavily paper-dependent and prone to significant administrative backlogs. Beneficiaries in FFS states must be particularly vigilant about their physical mail, as they are less likely to receive the multi-channel digital reminders common in MCO-driven states. Furthermore, FFS states in 2026 are increasingly implementing “periodic income checks” every six months for the expansion population, technically doubling the frequency of the compliance burden compared to the traditional annual cycle.

To navigate these differences, it is essential to identify which model your state employs, as the technical support available to you will differ:

| Feature | Managed Care (MCO) Model | Fee-for-Service (FFS) Model |

| Outreach Method | Multi-channel (App, SMS, Web Portal). | Primarily physical mail & paper notices. |

| Audit Frequency | Standard annual cycle (mostly). | Higher risk of 6-month periodic checks. |

| Support Source | Private insurance carrier’s member services. | State Medicaid caseworker/Agency. |

| Data Accuracy | High (utilizes real-time carrier data). | Moderate (reliant on state-level lag data). |

| Response Flexibility | Often allows digital document uploads. | May require mail-in or in-person verification. |

Understanding your state’s specific 2026 compliance frequency is no longer optional—it is a requirement for continuous health security. If you live in a “high-audit” FFS state, maintaining a digital file of your last three months of income (pay stubs or bank statements) is the best technical defense against a sudden loss of coverage due to an administrative backlog.

FAQ: Advanced Troubleshooting for 2026 Disenrollments

What is the technical process for appealing an “Automated Disqualification” triggered by a data mismatch?

If the 2026 tracking system incorrectly flags you as “over-income,” you must file a Request for Fair Hearing within the specific timeframe listed on your denial notice (usually 10 to 90 days). Technically, if you file the appeal within the first 10 days, you can request to keep your Medicaid coverage active while the judge reviews the case. You will need to present “contemporaneous evidence,” such as a letter from your employer or recent profit-and-loss statements, to prove that the state’s electronic data (IRS/NDNH) is technically “stale” or inaccurate relative to your current financial reality.

How do I manage a “Medical Spend-Down” to maintain 2026 Medicaid eligibility?

For those whose income is slightly above the 138% FPL limit, some states offer a “Medically Needy” or Spend-Down program. This technically allows you to qualify for Medicaid if your monthly medical bills are high enough to “spend down” your income to the eligibility level. In 2026, this requires a meticulous ledger of liability, where you submit unpaid medical bills, pharmacy receipts, and even transportation costs to the state caseworker. Once you hit your specific “spend-down” goal for the month, Medicaid kicks in to cover the remaining costs, effectively acting as high-deductible catastrophic coverage.

Can I move between states and maintain my Medicaid status during a 2026 redetermination?

Medicaid eligibility is technically not portable between states. If you move from New York to Florida in 2026, you must close your case in your previous state and file a brand-new application in the new one. This creates a high risk for a coverage gap. Strategic beneficiaries handle this by requesting a “Letter of Termination” from their old state immediately upon moving, which serves as the technical proof needed to trigger a 60-day Special Enrollment Period or a fast-tracked application in the new state, ensuring that the 2026 redetermination cycle doesn’t catch them without a home state of record.

What happens if the state fails to process my 2026 renewal form before the deadline?

In 2026, federal “Administrative Continuity” rules generally prohibit a state from terminating your coverage if the delay is solely due to the state’s inability to process your timely submitted form. If you have proof that you returned your packet within the 30-day window (such as a digital confirmation number or a certified mail receipt), but your coverage is still suspended, you have the technical right to an immediate reinstatement. You should contact your state’s Medicaid Ombudsman office to flag the procedural error and request that your benefits be “manually bridge-funded” until the back-end processing is complete.