Starting January 1, 2026, Medicare beneficiaries will benefit from a historic $2,000 annual cap on out-of-pocket prescription drug costs, providing unprecedented financial protection for those with high-cost chronic conditions.

The landscape of American geriatric healthcare is currently undergoing its most significant legislative evolution since the Medicare Modernization Act of 2003. At the heart of this transformation is the full implementation of the Inflation Reduction Act’s drug pricing reforms, which culminate in a radical restructuring of the Medicare Part D benefit design for the 2026 plan year. This shift is not merely a quantitative adjustment of cost-sharing limits but a fundamental reimagining of the financial risk distribution between the federal government, private insurance carriers, and pharmaceutical manufacturers. By introducing a hard $2,000 annual out-of-pocket cap, the program effectively transitions from a model of shared vulnerability to one of comprehensive catastrophic protection for the nation’s most medically complex retirees.

Understanding the magnitude of this shift requires an analysis of the “donut hole” legacy and the subsequent catastrophic phase that previously left many seniors exposed to unlimited 5% coinsurance costs. Prior to these reforms, a beneficiary requiring high-cost specialty therapeutics for conditions such as multiple sclerosis or certain oncology profiles could easily face annual pharmacy bills exceeding $10,000. The 2026 mandate permanently closes these gaps, consolidating the benefit into three distinct phases: the deductible, the initial coverage, and a final, absolute ceiling. This provides a level of actuarial predictability that was previously non-existent in the Part D marketplace, allowing for more precise long-term financial planning within the retirement window.

The legislative intent behind this $2,000 threshold extends beyond simple consumer relief; it acts as a market-correcting mechanism designed to lower the net prices of high-tier medications. By shifting a larger percentage of the cost burden during the catastrophic phase from Medicare (the government) to the Part D sponsors and drug manufacturers, the system incentivizes more aggressive price negotiations and formulary management. For the beneficiary, this means the $2,000 limit is a “hard” stop—once reached, the cost-sharing for all covered Part D drugs drops to zero for the remainder of the calendar year. This structural integrity ensures that healthcare-induced bankruptcy becomes a significantly diminished risk for the Medicare population.

Redefining the Standard Benefit Architecture

The technical architecture of Part D benefits in 2026 represents a streamlined departure from the convoluted “coverage gap” models of the past decade. In the previous iteration, the transition between the initial coverage limit and the catastrophic threshold created a period of increased cost-sharing that often led to medication non-adherence among lower-income seniors. The 2026 model simplifies this by eliminating the 5% coinsurance in the catastrophic phase entirely, replacing it with a definitive exit point at the $2,000 mark. This re-indexing of the benefit stages forces insurance providers to recalibrate their premium structures and plan designs to accommodate a higher liability profile once a member hits the cap.

The role of the manufacturer discount program has also been overhauled to support this new architecture. Under the 2026 rules, drug manufacturers are required to provide significant discounts on both brand-name drugs and biologics throughout the coverage duration, a responsibility that was previously more fragmented. This ensures that the progress toward the $2,000 cap is subsidized by the industry rather than being solely dependent on the patient’s liquid assets or the government’s reinsurance subsidies. Consequently, the primary financial interaction for the patient is now confined to the early-year deductible and the subsequent copayments, which are systematically tracked against the new federal ceiling.

To visualize the magnitude of these changes, the following comparison highlights the technical differences between the expiring system and the 2026 reality:

| Feature | 2024 Legacy Framework | 2026 Restructured Framework |

| Annual Out-of-Pocket Cap | No hard limit (5% coinsurance remained) | Fixed $2,000 Maximum |

| The “Donut Hole” | Partially bridged via manufacturer discounts | Permanently Abolished |

| Catastrophic Co-pay | Approximately 5% for most drugs | $0 for all covered prescriptions |

| Plan Sponsor Liability | Lower (Government held majority risk) | Significantly Higher |

| Manufacturer Discounts | Primarily focused on the gap phase | Applied across all coverage phases |

Strategic Mechanisms of the Medicare Prescription Payment Plan

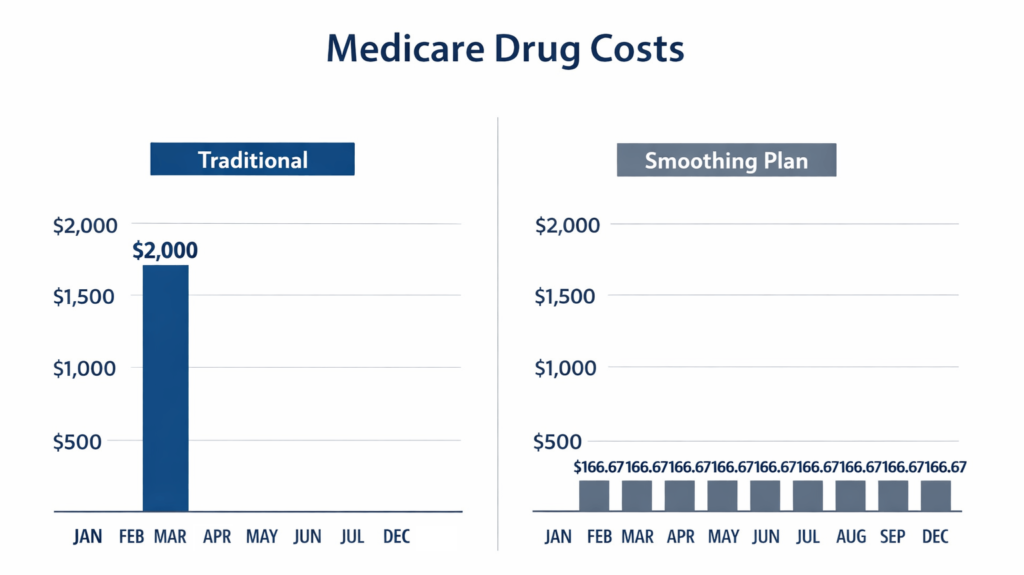

One of the most innovative technical additions accompanying the $2,000 cap is the Medicare Prescription Payment Plan, colloquially referred to as the “smoothing” option. This program addresses a critical UX flaw in previous Medicare iterations: the front-loading of costs. For patients on high-cost maintenance drugs, the entire $2,000 cap could historically be triggered in the very first month of the year, creating a “January shock” that destabilized household budgets. The smoothing mechanism allows for these out-of-pocket costs to be distributed into equitable monthly installments, effectively acting as a zero-interest line of credit for healthcare expenses.

The algorithm used to calculate these monthly payments is dynamic and recalibrates if the beneficiary is prescribed new medications mid-year. If a patient opts into the program in January and is expected to hit the $2,000 cap, their monthly payment would be roughly $166.67. However, if they join later or their spending patterns change, the system recalculates the remaining balance divided by the months left in the year. This prevents the accumulation of large, unmanageable debts and ensures that the financial protection of the $2,000 cap is felt consistently throughout the fiscal year rather than just in the latter quarters.

It is important to differentiate this program from a traditional loan or a credit card; there are no interest charges, no credit checks, and no impact on one’s credit score for participation. It is a strictly administrative re-tabulation of how the $2,000 is collected. However, the technical burden falls on the Part D sponsors to provide real-time tracking and clear communication regarding these balances. For the beneficiary, the decision to opt-in should be based on a technical review of their specific medication costs; those who only take low-cost generics may find the standard point-of-sale payment more efficient than managing a monthly billing cycle.

Impact on Specialty Tiers and High-Cost Therapeutics

The 2026 cap is most transformative for the “Specialty Tier” of medications, which includes biologics and sophisticated chemical entities used to treat autoimmune disorders, advanced cancers, and rare genetic conditions. These drugs often carry a list price of several thousand dollars per 30-day supply. Under the old system, even after reaching the catastrophic threshold, the 5% coinsurance could result in a monthly cost of several hundred dollars indefinitely. By capping the total annual exposure at $2,000, Medicare has effectively created a universal safety net for patients who require the most expensive medical interventions available in modern pharmacology.

This shift has profound implications for clinical outcomes and medication adherence. Research has consistently shown that as out-of-pocket costs rise, patient compliance drops, leading to secondary health complications and increased hospitalizations. By removing the financial barrier once the cap is met, the system promotes continuous therapy, which is particularly critical for chronic conditions where a lapse in medication can lead to irreversible disease progression. The technical relief provided here is not just financial; it is a clinical intervention that stabilizes the patient’s treatment trajectory.

The categories of medications that will see the most immediate benefit from this $2,000 ceiling include:

- Oncology treatments and oral chemotherapy agents that previously triggered high coinsurance.

- Biological response modifiers for Rheumatoid Arthritis and Psoriatic conditions.

- Advanced therapies for Multiple Sclerosis (MS) that involve high monthly maintenance costs.

- Sophisticated anticoagulants and cardiovascular drugs found on higher formulary tiers.

- Specialty medications for chronic pulmonary conditions and rare respiratory diseases.

Navigating Formulary Shifts and Plan Selection in 2026

While the $2,000 cap is a federal mandate, the specific way insurance carriers respond to this new liability is found in the “fine print” of their 2026 formularies. Because insurers now bear more of the financial risk when a patient reaches the cap, they may implement more rigorous utilization management tools. This includes expanded use of Prior Authorization (PA), Step Therapy (where a patient must try a cheaper drug first), and Quantity Limits. Beneficiaries must technically evaluate not just the premium of a plan, but the “formulary breadth”—ensuring their specific medications haven’t been moved to a “non-preferred” status or subjected to new clinical hurdles.

The 2026 enrollment period will require a more sophisticated analysis of the “Evidence of Coverage” (EOC) documents than in previous years. Data suggests that as the out-of-pocket cap tightens, plan sponsors may narrow their pharmacy networks or adjust their “tiering” logic to steer patients toward medications with higher manufacturer rebates. Technical literacy in reading these plan summaries is essential; a plan with a low monthly premium might have a highly restrictive formulary that makes it difficult to access the specific specialty drug a patient needs, even if the $2,000 cap still applies once the drug is approved.

Furthermore, the integration of real-time benefit tools (RTBT) into provider workflows is becoming a necessity. These digital tools allow physicians to see exactly what a medication will cost a patient based on their specific progress toward the $2,000 cap at the moment of prescription. For the user, monitoring this progress via the insurer’s mobile app or web portal is no longer optional—it is a core component of managing health-related cash flow in the post-reform era. Understanding where one stands in relation to the deductible and the final cap is the new standard for informed healthcare consumption.

Long-term Fiscal Implications for the American Retiree

The transition to a capped out-of-pocket system in 2026 represents a stabilizing force for retirement portfolios. For decades, the “wildcard” in retirement planning was the unpredictable nature of healthcare costs; one serious diagnosis could deplete a lifetime of savings through compounding medication expenses. By establishing a statutory maximum, Medicare has effectively “derisked” the healthcare component of retirement, allowing individuals to allocate their resources with greater confidence. This creates a more resilient financial foundation for the millions of Americans living on fixed incomes who are most sensitive to inflationary pressures in the medical sector.

As we look beyond 2026, the sustainability of this benefit will depend on the continued success of the government’s drug price negotiations. The $2,000 cap is part of a broader ecosystem that includes the federal government’s new authority to negotiate prices for the highest-spending drugs in the Medicare program. If these negotiations successfully lower the aggregate cost of drugs, the financial pressure on the Part D program—and by extension, the premiums paid by seniors—will remain manageable. It is a delicate balance of legislative pressure and market dynamics aimed at ensuring the long-term viability of the social safety net.

Ultimately, the 2026 revolution is about more than just saving money; it is about the dignity of the American retiree. The ability to access life-saving science without the specter of financial ruin is a landmark achievement in social policy. As beneficiaries navigate this new reality, the focus shifts from surviving the system to optimizing one’s health within a framework that finally prioritizes financial security alongside clinical efficacy. The restructured Medicare Part D stands as a testament to the possibility of aligning complex insurance mechanics with the fundamental needs of the human beings they are designed to serve.

Technical Clarifications: FAQ for the 2026 Transition

How does the $2,000 cap interact with physician-administered medications covered under Medicare Part B?

It is technically vital to distinguish between Part D and Part B drug coverage in the context of the 2026 reforms. The $2,000 out-of-pocket limit applies exclusively to medications covered under a Medicare Part D prescription drug plan (or the drug portion of a Medicare Advantage plan). Drugs administered in a clinical setting, such as intravenous chemotherapy or certain injectable biologics covered under Part B, typically remain subject to the 20% coinsurance unless the beneficiary has supplemental coverage (Medigap). Beneficiaries with complex treatment regimens involving both Part B and Part D medications must continue to calculate these financial silos separately, as the Part D cap does not provide a “cross-benefit” ceiling for medical-side expenses.

What happens to the accumulated True Out-of-Pocket (TrOOP) balance if a beneficiary switches plans mid-year?

The 2026 framework maintains the principle of TrOOP portability, but the technical execution requires administrative oversight. If a beneficiary transitions between Part D plans during a Special Enrollment Period (e.g., due to a move), their spending progress toward the $2,000 cap is legally required to transfer to the new plan sponsor via the Automated TrOOP Balance Transfer (ATBT) system. However, delays in data synchronization between private insurers can occasionally occur. It is strategically advisable for beneficiaries to retain their final “Explanation of Benefits” (EOB) from the previous carrier to ensure the new plan accurately reflects their position relative to the $2,000 threshold and the smoothing payment plan eligibility.

Are “out-of-network” pharmacy fills and non-covered medications counted toward the annual limit?

The $2,000 cap is strictly limited to “covered” Part D drugs filled at network pharmacies. Any expenditure on medications that are not on the plan’s formulary—or for which a formulary exception has not been granted—does not contribute to the $2,000 ceiling. Similarly, if a beneficiary fills a prescription at an out-of-network pharmacy without meeting the plan’s specific emergency criteria, those costs are typically borne entirely by the patient and are excluded from the TrOOP calculation. To maximize the protection of the 2026 cap, beneficiaries must ensure clinical alignment with their plan’s network and formulary requirements, utilizing the grievance and appeals process for any essential medications initially excluded from coverage.