The tax landscape of 2026 has finally reached a state of equilibrium following years of administrative delays and legislative pivots regarding digital payment reporting. The primary catalyst for this stability was the One Big Beautiful Bill Act (OBBBA), enacted in late 2025, which definitively halted the IRS’s planned transition to a $600 reporting threshold. For taxpayers in 2026, this means the federal requirement for receiving a Form 1099-K has returned to the traditional standard: $20,000 in gross payments and more than 200 transactions within a single calendar year.

This legislative reversal was a direct response to the massive “informational noise” and administrative burden that a lower threshold would have imposed on both the IRS and casual users of apps like Venmo and PayPal. In 2026, the OBBBA ensures that millions of Americans who use these platforms for splitting dinner bills, paying rent to roommates, or selling occasional used items on marketplaces are technically shielded from receiving unnecessary tax forms. The focus of federal reporting has returned to high-volume commercial activity, preserving the “casual use” nature of digital wallets.

However, it is critical for the 2026 professional to distinguish between reporting and taxability. While the TPSO (Third-Party Settlement Organization) may not be technically required to issue a 1099-K for amounts under the $20,000 threshold, any income earned through these apps for services or goods remains legally taxable. The IRS has shifted its strategy in 2026 toward high-level data matching and bank-level scrutiny rather than relying solely on the 1099-K “dragnet” that defined the early 2020s.

TPSO Technicalities: Why Venmo Reports but Zelle Does Not

A common technical point of confusion in 2026 remains the distinction between different payment architectures. TPSOs (Third-Party Settlement Organizations), such as Venmo, PayPal, and Cash App, are legally classified as entities that facilitate payments between two parties who do not have a direct bank-to-bank relationship. Because they act as intermediaries that hold or move funds through internal ledgers, they fall under the 1099-K reporting mandate once the $20,000/200 transaction threshold is breached.

In contrast, Zelle operates as a direct bank-to-bank transfer network. When you send money via Zelle, the funds move directly from one financial institution to another without being “settled” by a third-party organization. Consequently, Zelle is technically exempt from 1099-K reporting requirements, regardless of the amount sent. In 2026, this structural difference makes Zelle a preferred tool for many small landlords and high-value service providers who want to avoid the administrative complexity of 1099-K reconciliation, provided they are accurately reporting their income elsewhere.

This technical divide means that a freelancer receiving $25,000 through Venmo will receive a 1099-K in 2026, while a freelancer receiving the same $25,000 through Zelle will not. However, the IRS’s Automated Underreporting (AUR) systems have become significantly more advanced. In 2026, large, consistent deposits from Zelle into a personal bank account are often flagged for a “Nexus Audit,” where the taxpayer must prove that the deposits are not undisclosed business revenue.

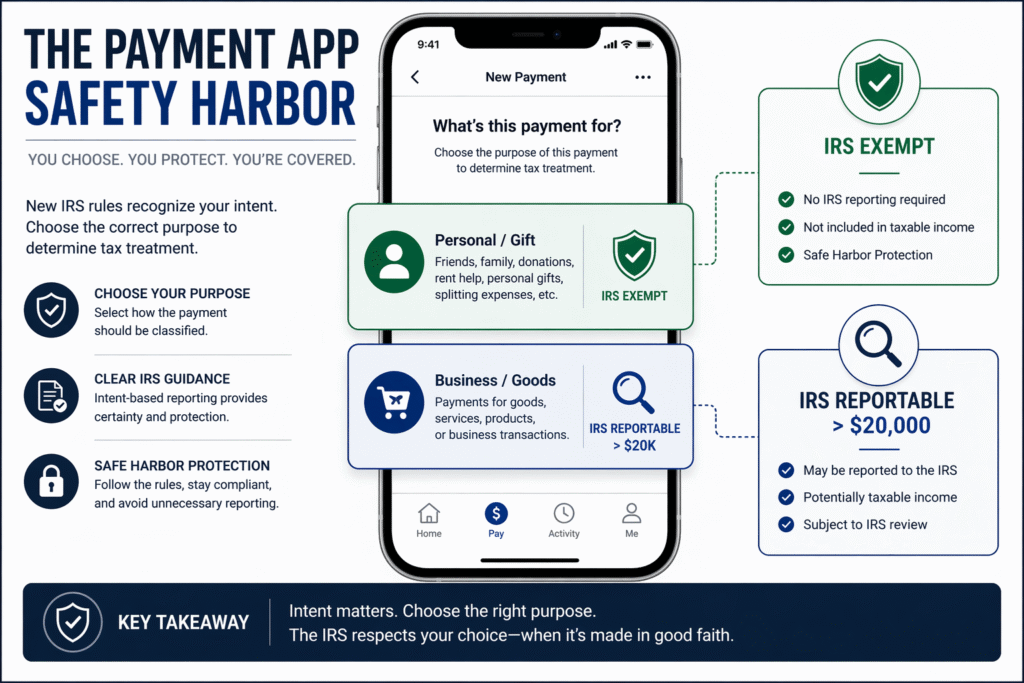

The “Friends & Family” Safe Harbor vs. Business Tags

The primary technical defense against a 1099-K error in 2026 is the correct use of Transaction Tags. Most payment platforms have standardized the choice between “Personal” (Friends & Family) and “Business” (Goods & Services). In 2026, the OBBBA clarified that only transactions tagged as “Business” contribute toward the $20,000/200 transaction reporting threshold. Personal transfers are technically held in a “Safe Harbor,” meaning they are invisible to the IRS’s 1099-K data ingestion stream.

Problems arise in 2026 when users mislabel transactions. If a user receives $21,000 in personal reimbursements but has them erroneously tagged as “Business,” the platform is technically required to issue a 1099-K. Correcting this after the fact is a bureaucratic hurdle, as it requires the platform to issue a “Corrected 1099-K” to the IRS. To maintain a clean digital audit trail, 2026 users must be disciplined in ensuring that non-taxable reimbursements are never processed through a “Business” profile or with a commercial tag.

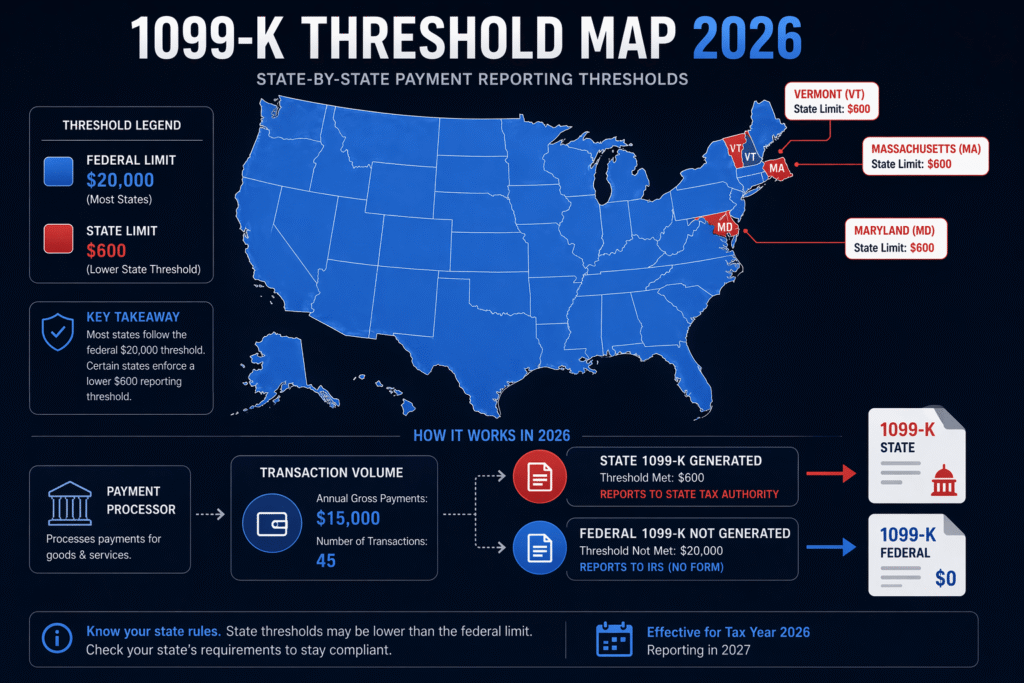

State-Level Variance: The 2026 Local Reporting Trap

While the OBBBA restored the federal $20,000 threshold, many states in 2026 have chosen to maintain their own Lower Reporting Thresholds. This creates a technical trap for taxpayers living in states like Massachusetts, Vermont, or Maryland, where the state-level requirement for a 1099-K remains as low as $600 or $1,000. In these jurisdictions, the payment app will issue a state-specific 1099-K even if a federal form is not generated.

This creates a “Reporting Mismatch” that the 2026 professional must navigate during tax filing. If you receive a state 1099-K for $5,000, that data is shared with the state’s revenue department. If you do not reflect that income on your federal return, the IRS may receive a “State Data Trigger,” prompting an inquiry into the discrepancy. In 2026, “Federal Compliance” does not automatically mean “State Compliance,” requiring a localized view of digital asset and payment reporting.

Furthermore, some platforms in 2026 have streamlined their systems to issue a “Unified 1099-K” that lists both federal and state data. If you live in a low-threshold state, you must be prepared to provide a “Form 1099-K Reconciliation” on your federal Schedule C or Schedule 1. This technically explains to the IRS that while a form was issued due to state law, the activity does not meet the federal threshold or is not taxable (e.g., selling a personal item at a loss).

The New 1099-NEC Integration ($2,000 Threshold)

A critical shift in 2026 is the tighter integration between the 1099-K and the Form 1099-NEC (Non-Employee Compensation). Under the OBBBA, while the 1099-K threshold returned to $20,000, the 1099-NEC threshold for direct payments to contractors was technically adjusted to $2,000 (up from the legacy $600). This was designed to reduce the “form fatigue” for small businesses while still capturing significant independent labor.

| Feature | Form 1099-K (TPSO) | Form 1099-NEC (Direct) |

| 2026 Threshold | $20,000 + 200 Transactions | $2,000 |

| Applicability | Payments via Apps/Marketplaces | Direct Bank/Check/Cash payments |

| Primary Trigger | Commercial Tagging | Business-to-Business Service |

| OBBBA Impact | Reverted to legacy high limits | Permanent inflation adjustment |

This distinction is vital for 2026 business owners. If you pay a contractor $5,000 through a business credit card or Venmo Business, you technically do not need to issue a 1099-NEC, as the 1099-K reporting burden falls on the payment processor. However, if you pay that same $5,000 via a direct Zelle transfer or a paper check, you are technically required to issue a 1099-NEC because the Zelle transfer is not covered by the 1099-K “Safety Net.”

FAQ: Mastering the 2026 Payment App Tax Season

I sold a used couch for $800 on Venmo. Will I get a 1099-K in 2026?

No. Under the 2026 federal rules, $800 is well below the $20,000 threshold. Even if you live in a state with a $600 threshold and receive a state-level form, selling a personal item for less than you originally paid (a capital loss) is technically not taxable income. You would simply report the sale and the “Cost Basis” (original price) on your return to show a $0 gain.

Does Zelle affect my “Debt-to-Income” (DTI) ratio for a 2026 mortgage?

It can. While Zelle doesn’t trigger a 1099-K, 2026 mortgage underwriters often perform an “Electronic Cash Flow Audit” on your last 12 months of bank statements. If they see $3,000 in monthly Zelle deposits, they will technically count that as business income and may require a Profit & Loss (P&L) statement to verify your DTI, regardless of whether a tax form was issued.

Can the IRS audit me if I don’t receive a 1099-K?

Yes. The 1099-K is just a reporting tool for the IRS; it is not the sole basis for an audit. In 2026, the IRS uses “Lifestyle-to-Income Matching.” If your public spending, property records, or social media presence suggests a lifestyle that exceeds your reported income, they may use a “John Doe Summons” to pull your Venmo or PayPal records to find untaxed revenue.

Why is my Venmo account asking for my SSN in 2026?

This is due to “Backup Withholding” regulations. Even if you aren’t near the $20,000 threshold, the platform is technically required to have your Taxpayer Identification Number (TIN) on file once you reach a certain level of activity (often $600 in aggregate business sales). If you fail to provide it, they are legally required to withhold 24% of your future payments and send them to the IRS.

What is the “Business Profile” trap in 2026?

In 2026, many apps have “Business Profiles” that offer extra features. Once you create a Business Profile, the platform technically assumes every payment received there is commercial. If you use your Business Profile to receive a “Friends & Family” reimbursement, it will be counted toward your $20,000 threshold, potentially triggering an unnecessary 1099-K.

How do I contest an incorrect 1099-K in 2026?

You must contact the platform’s Tax Compliance Department to request a correction. If they refuse, the IRS provides a technical workaround: you can report the amount on your tax return as “Other Income” and then enter an offsetting negative amount labeled “Form 1099-K received in error – non-taxable reimbursement.” This alerts the IRS’s matching system so it doesn’t trigger an automatic “Underreporter” notice..