In the 2026 real estate landscape, assumable mortgages have emerged as a powerful strategic tool, allowing savvy buyers to inherit a seller’s low-interest rate and bypass current market volatility.

The real estate market of 2026 is defined by a massive divergence between “legacy” financial assets and current market realities. While the Federal Reserve’s long-term stabilization efforts have kept new mortgage rates hovering in the 6% to 7% range, millions of homes still carry underlying debt from the “Golden Era” of 2020-2021, when rates were technically bottomed out near 3%. This discrepancy has transformed the Assumable Mortgage from an obscure contractual clause into the most powerful arbitrage tool available to the 2026 homebuyer. By “assuming” a seller’s existing loan, a buyer can technically inherit their low interest rate, effectively bypassing the current inflationary cost of capital.

This strategy is particularly effective in 2026 because the interest-rate spread is so wide that it fundamentally alters a property’s affordability. For a standard $500,000 loan, the difference between a 3% assumed rate and a 7% market rate represents a monthly savings of nearly $1,200 in interest alone. In the competitive 2026 landscape, a home with an assumable mortgage is no longer just a piece of real estate; it is a structured financial product that offers a guaranteed ROI from day one. Buyers are increasingly ignoring “turn-key” renovations in favor of “turn-key financing,” prioritizing the technical yield of the loan over the aesthetic of the kitchen.

However, the 2026 market for these loans is highly technical and requires a sophisticated understanding of equity gaps. Because home prices have continued to appreciate since those low-rate loans were originated, the “Assumable Balance” is often significantly lower than the current “Sale Price.” This creates a capital hurdle that the modern buyer must solve through strategic financing. Success in 2026 requires more than just finding an assumable loan; it requires the financial engineering to bridge the difference without eroding the long-term interest savings that make the deal viable in the first place.

Eligibility and Loan Types: FHA, VA, and USDA Rules

To navigate the 2026 assumable landscape, one must technically distinguish between different loan types, as not all mortgages allow for this maneuver. Most conventional loans—those backed by Fannie Mae or Freddie Mac—contain “Due-on-Sale” clauses that prevent a buyer from taking over the seller’s rate. Conversely, government-backed loans are technically “assumable by default,” provided the buyer meets the original lender’s credit and income requirements. In 2026, these government-backed instruments represent the “hidden inventory” that savvy investors and first-time buyers are targeting. The eligibility criteria for these loans in 2026 are governed by three distinct technical frameworks:

- FHA Loans (Federal Housing Administration): These are the most common assumable loans. The buyer must undergo a full credit check and prove they meet the same debt-to-income (DTI) ratios as the original borrower to release the seller from liability.

- VA Loans (Department of Veterans Affairs): While technically assumable by anyone (including non-veterans), there is a specific technicality regarding the “entitlement.” If a non-veteran assumes the loan, the original veteran’s entitlement remains tied to the house, preventing them from using it elsewhere until the loan is paid off.

- USDA Loans (U.S. Department of Agriculture): These are assumable for rural properties, but they often require the buyer to meet specific income limits, making them a technical niche for lower-to-middle-income professionals looking for suburban or rural 2026 retreats.

For the 2026 professional, the VA loan assumption is often the most lucrative but complex. Sellers who are veterans are increasingly hesitant to “leave their entitlement behind” unless the buyer is also a veteran who can “substitute” their own entitlement. This has led to the rise of Entitlement Exchanges in 2026, where veteran buyers and sellers trade VA loans to preserve their borrowing power. Understanding these nuances is the difference between a failed offer and a successful technical acquisition of a sub-market interest rate.

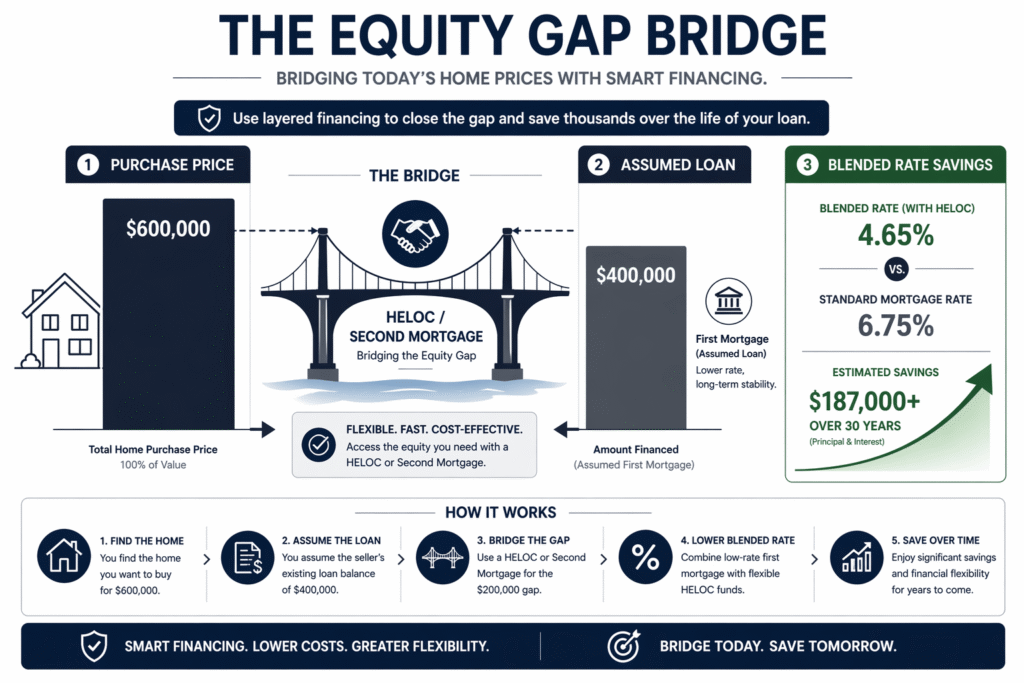

Bridging the “Equity Gap”: The Mid-Career Challenge

The primary technical barrier to an assumable deal in 2026 is the Equity Gap. For example, if a seller is listing their home for $600,000 but their assumable loan balance is only $400,000, the buyer must come up with $200,000 in cash to “close the gap.” In 2026, very few buyers have that level of liquid capital on hand, leading to the resurgence of “Piggyback” Second Mortgages and HELOCs (Home Equity Lines of Credit). The goal is to finance the gap at 2026 rates while keeping the bulk of the debt at the 3% assumed rate.

In 2026, the “Equity Gap” is the final boss of the assumable mortgage deal; if you cannot bridge it technically through a second lien or liquid capital, the interest rate arbitrage remains out of reach regardless of your credit score.

This financing requires a “Blended Rate” analysis. If you assume $400,000 at 3% and take a $200,000 second mortgage at 9%, your blended interest rate is approximately 5%—still significantly lower than the 7% market average. In 2026, mortgage brokers have specialized in these Hybrid Assumptions, providing the documentation necessary to convince the primary lender that the buyer has the technical capacity to service both the assumed debt and the new second lien simultaneously.

The Assumption Process: Documentation and Timelines

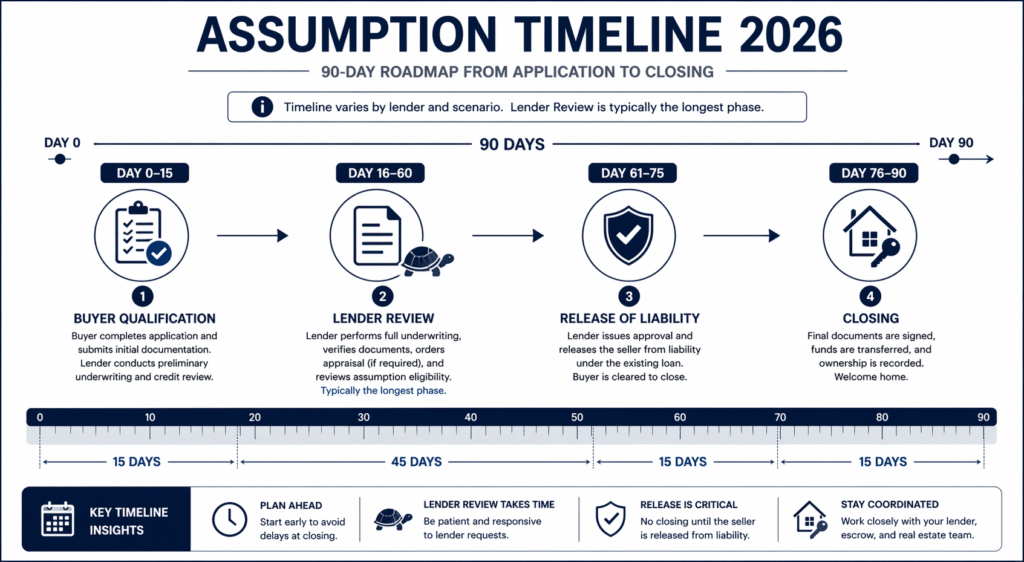

One of the most frustrating technical realities of 2026 is that the original lender has very little incentive to process an assumption. Since the bank would prefer the buyer to take out a new loan at current 7% rates, assumption applications are often pushed to the bottom of the pile. In 2026, a standard assumption takes 60 to 90 days to close, nearly double the time of a traditional purchase. Buyers must technically account for this delay in their “Rate Lock” strategy and move-in timelines.

The documentation required is nearly identical to a new loan application, but the “Release of Liability” is the most critical technical artifact. Without a formal release, the seller remains legally responsible for the debt even after the buyer takes the title. In 2026, no savvy seller will close an assumption without a HUD-authorized release, as it would destroy their “Credit Tendency” if the buyer were to default in the future.

Furthermore, the buyer must pay an “Assumption Fee,” which in 2026 is typically capped at $900 for FHA and VA loans, plus standard closing costs. While this is significantly cheaper than the points and origination fees of a new mortgage, the technical overhead of managing the process requires a dedicated “Assumption Coordinator.” Many 2026 real estate teams now include a specialist whose only job is to harrass the original servicer’s compliance department to ensure the paperwork doesn’t stall in the “legacy systems” that many banks still use for these rare transactions.

ROI Analysis: Monthly Savings vs. Upfront Capital

The true measure of a 2026 assumption is the Time-to-Recoup. Because bridging the equity gap often requires higher upfront cash or a more expensive second mortgage, the buyer must calculate how many months of “Interest Savings” it takes to break even on the acquisition costs. In 2026, most successful assumptions pay for themselves within 18 to 24 months, providing a massive long-term wealth-building effect as the principal on the 3% loan is paid down much faster than on a 7% loan.

| Metric | New Market Mortgage (2026) | Assumed Hybrid Deal (3% + 9%) |

| Primary Rate | 7.25% (Fixed) | 3.00% (Assumed) |

| Monthly P&I Payment | $3,410 | $2,350 (Blended) |

| Annual Interest Paid | $36,200 | $18,400 |

| 10-Year Equity Growth | Baseline | +45% Faster Amortization |

| Closing Costs | ~3% of Loan | <$2,000 (Assumption Fee) |

FAQ: Mastering the Assumable Deal

What happens to the VA Entitlement if I’m not a veteran?

Technically, if you assume a VA loan as a non-veteran, the seller’s entitlement remains “bound” to that property until the loan is paid off in full. In 2026, this is a major negotiation point. You may have to pay a “Premium Price” for the home to compensate the veteran for losing their ability to use a $0-down VA loan on their next purchase.

Can I assume a 2026 mortgage if the seller is in foreclosure?

Yes, this is known as an “Assumption in Lieu of Foreclosure.” In 2026, many distressed sellers are using assumptions as a “bailout” strategy. You take over the payments and the low rate, and the seller saves their credit score. However, you must technically pay off any “arrears” (overdue payments) upfront, which can add to your “Equity Gap” costs.

Are there specialized “Assumption Loans” for the equity gap in 2026?

Yes. Several 2026 fintech firms now offer “Assumption Gap Loans.” These are short-term, interest-only liens specifically designed to cover the difference between the assumption balance and the purchase price. They often have higher rates (8-10%), but because the underlying 3% loan is so large, the total monthly payment remains lower than a standard 7% mortgage.

Do I need a specific credit score for a 2026 assumption?

Technically, you must meet the original lender’s current standards. In 2026, this usually means a FICO 10T score of at least 620-640 for FHA/VA, but many lenders “overlay” stricter requirements (up to 680) because they aren’t making much profit on the 3% loan. You should have your “Credit Tendency” report ready before even approaching the seller.

Does an assumable mortgage affect my property taxes in 2026?

No. Your property taxes are technically based on the new purchase price (the value of the home in 2026), not the original loan amount or the assumed rate. While your mortgage payment stays low, you must still budget for 2026 tax assessments, which have risen significantly alongside home values.

Where do I find these “Assumable” listings in 2026?

While the MLS (Multiple Listing Service) now has a “Assumable” filter, many 2026 buyers use specialized platforms like Roam or Assume-It. These AI-driven scrapers identify FHA and VA loans by their “recording data” and alert buyers to properties with high-balance, low-rate loans even before the seller mentions it in their marketing.