The full implementation of Secure Act 2.0 provisions in 2026 is reshaping how Americans save for retirement, introducing mandatory automatic enrollments and innovative ways to build wealth while paying off debt.

The financial landscape of 2026 has reached a pivotal milestone with the full-scale implementation of the SECURE Act 2.0. While the legislation was signed into law years ago, its most transformative provisions were staggered to allow payroll systems and plan providers to modernize their infrastructures. In 2026, we are finally seeing the “pico” of this transition, where the default relationship between employees and their retirement accounts has shifted from passive participation to an automated, high-velocity wealth-building engine.

The technical maturity of SECURE 2.0 in 2026 has effectively dismantled the “procrastination barrier” that historically plagued mid-career professionals. With the mandate for automatic enrollment and escalation now applying to nearly all new 401(k) and 403(b) plans, the “inertia” that once kept participation rates low has been reversed. For the 2026 professional, retirement planning is no longer an item on a to-do list; it is a background process that scales in lockstep with their career progression.

However, this automation comes with a new layer of complexity, particularly for high-earning individuals and those navigating the transition between pre-tax and Roth contributions. In 2026, the strategy is no longer just about “how much” you save, but “where” that capital is technically categorized to minimize future tax drag. Navigating the 2026 retirement rules requires a surgical understanding of the new IRS thresholds and the specific catch-up mandates that now define the upper echelons of the workforce.

High-Earner “Rothification”: The New Mandatory Catch-up Rules

Perhaps the most disruptive technical change to take effect in 2026 is the Mandatory Roth Catch-up Rule for high earners. After a multi-year “administrative grace period” from the IRS, any employee who earned more than $145,000 in the previous calendar year is now technically prohibited from making pre-tax catch-up contributions. Instead, these additional funds must be directed into a Roth account, meaning they are taxed at your current 2026 marginal rate in exchange for tax-free growth and withdrawals in the future.

This “Rothification” of catch-up contributions represents a significant shift in tax-diversification strategy. For the professional earning $200k+, the immediate tax deduction of the catch-up is gone, which might increase their current year tax liability. However, the technical benefit is the creation of a massive “tax-free bucket” that is not subject to the same Required Minimum Distributions (RMDs) in the future. In 2026, the strategy is to embrace this mandate as a forced hedge against the potential for higher tax rates during the 100-year life era. The mandatory Rothification brings four specific technical impacts that you must audit:

- Net-Pay Impact: Expect a slightly lower take-home pay as catch-up contributions no longer lower your current taxable base.

- Tax-Bracket Management: High earners near the top of a bracket must be more precise with other deductions to avoid “bracket creep.”

- Employer Matching: Even if your catch-up is Roth, your employer’s “match” may still be pre-tax, requiring a split-accounting view of your total balance.

- RMD Shielding: Roth 401(k) balances no longer require RMDs during the owner’s lifetime, providing a long-term technical advantage for legacy planning.

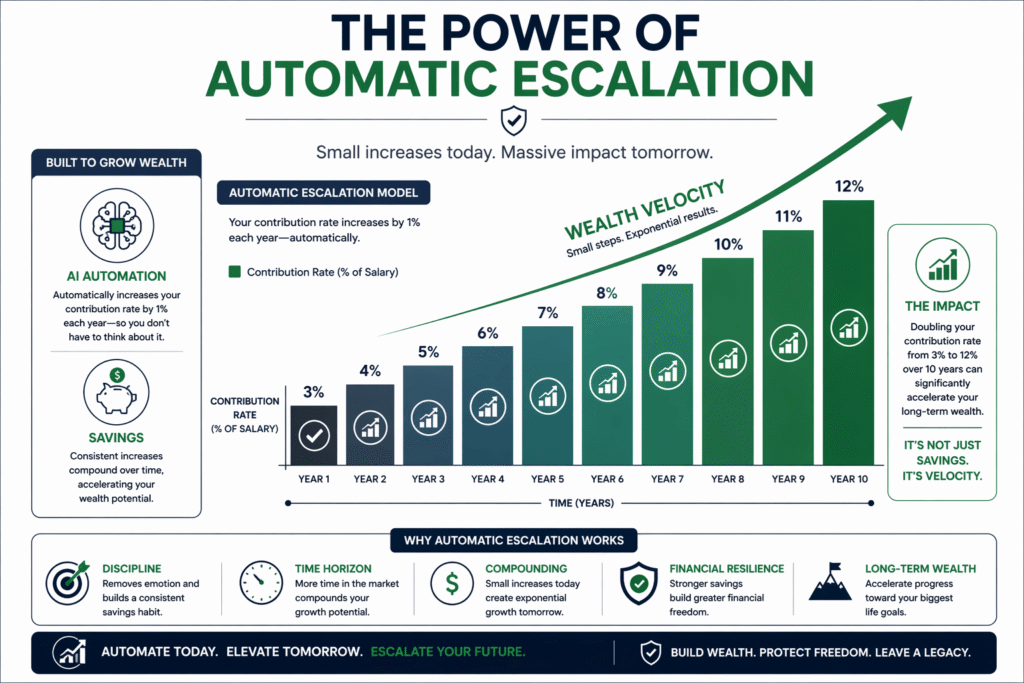

Automatic Enrollment and Escalation: The New Default in 2026

In 2026, the burden of “starting” a retirement plan has technically been shifted from the employee to the employer. Under SECURE 2.0, nearly all new 401(k) and 403(b) plans established after late 2022 must now automatically enroll employees at a rate between 3% and 10% of their salary. Furthermore, these plans feature “Automatic Escalation,” which technically increases your contribution rate by 1% each year until it reaches a cap of at least 10% (but no more than 15%).

This structural change has effectively institutionalized the “pay yourself first” philosophy. While employees still have the technical right to opt-out, the psychological power of the “default” has led to a record-breaking surge in total market liquidity. In 2026, we are witnessing the first generation of workers who will likely never experience a year of “zero savings,” regardless of their initial financial literacy levels.

The 2026 retirement landscape has successfully replaced human willpower with systemic automation, ensuring that the “default path” for every worker is one of compounding wealth rather than eventual insolvency.

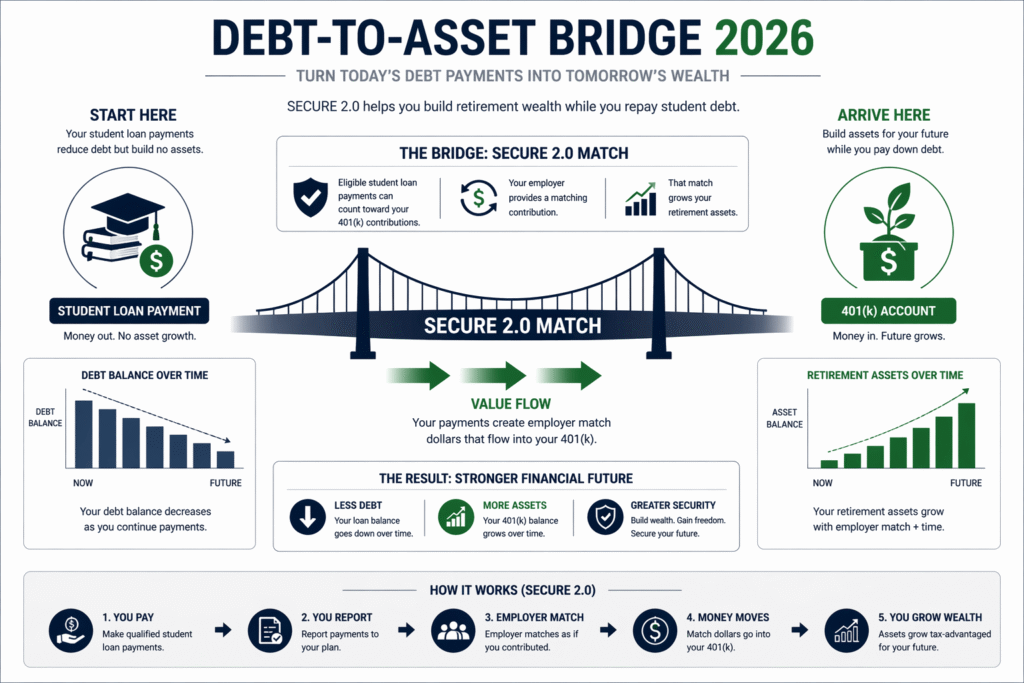

Turning Debt into Wealth: Mastering the Student Loan Match

For the 2026 professional still carrying student debt, SECURE 2.0 has introduced a revolutionary technical bridge: the Student Loan Matching provision. In the past, young professionals often had to choose between paying down high-interest loans or receiving their employer’s 401(k) match. In 2026, your employer can technically treat your student loan payments as if they were contributions to your retirement plan, allowing them to deposit the “matching” funds directly into your 401(k) even if you didn’t contribute a single dollar of your own.

This mechanism is a game-changer for long-term Capital Accumulation. It allows the borrower to simultaneously reduce their debt principal while the employer builds the foundation of their retirement portfolio. To utilize this, you must technically certify your loan payments with your HR department annually. In 2026, the “Choice between Debt and Savings” is no longer a zero-sum game; it is an integrated strategy for total net worth optimization.

Furthermore, the 2026 integration of these matches is largely automated via payroll-to-servicer APIs. This ensures that the “match” occurs with minimal administrative lag, allowing your retirement funds to start compounding early. For the professional navigating the SAVE Plan, this match represents a “double-win”: the government subsidizes the loan interest while the employer builds the 401(k) asset, effectively accelerating the professional’s “Net Worth Pivot” by several years.

The “60-63 Boost” and Higher Catch-up Limits

One of the most powerful technical “kicker” provisions to reach full visibility in 2026 is the specialized catch-up limit for those aged 60 to 63. While the standard catch-up limit for those 50+ remains indexed to inflation, SECURE 2.0 has introduced a higher tier for those in the final stretch of their primary career. In 2026, individuals in this age bracket can contribute the greater of $10,000 or 150% of the standard catch-up limit.

This “Last-Mile Boost” is a technical gift for those who may have under-saved in their earlier stages or those who simply want to maximize their tax-sheltered growth. When combined with the mandatory Roth rules for high earners, this creates a high-velocity “Roth Conversion” event in the years immediately preceding retirement. In 2026, a 62-year-old high-earner is technically capable of shielding a massive amount of capital from future taxation through this optimized catch-up window.

| Age Bracket | Standard Limit | Catch-up Provision | Total Max Contribution (2026 Est.) |

| Under 50 | $23,500 | N/A | $23,500 |

| 50 – 59 | $23,500 | +$7,500 | $31,000 |

| 60 – 63 (The Boost) | $23,500 | +$11,250* | $34,750 |

| 64+ | $23,500 | +$7,500 | $31,000 |

*Calculated as 150% of the standard catch-up; exact 2026 figures are subject to IRS inflation adjustments.

FAQ: Optimizing Your 2026 Retirement Plan

What happens if I earn over $145k in a “commission-heavy” year, but less the next?

The mandatory Roth catch-up rule is based on your previous year’s FICA wages. If you earned $150k in 2025, your 2026 catch-ups must be Roth. If your income then drops to $140k in 2026, your 2027 catch-ups can technically revert to pre-tax. You must perform an “Annual Income Audit” every January to ensure your payroll withholding is technically compliant with the current year’s mandate.

Can I still do a “Backdoor Roth IRA” in 2026?

Yes. As of early 2026, the Backdoor Roth IRA and the “Mega Backdoor Roth” strategies remain technically legal and are more important than ever. Given the mandatory Rothification of 401(k) catch-ups, many 2026 professionals are finding that their total “Roth-to-Pre-tax” ratio is naturally shifting toward a more tax-efficient balance, reducing the need for aggressive conversions elsewhere.

Does my employer have to offer the Student Loan Match in 2026?

No. While the law allows employers to offer this match, it is not a technical mandate. However, in the competitive 2026 talent market, nearly 60% of Fortune 500 companies have already integrated this benefit. If your company doesn’t offer it, you should advocate for it as a “no-cost” retention tool, as it technically uses the same budget as the standard 401(k) match.

What is the “Emergency Savings Account” (PLESA) linked to my 401(k)?

In 2026, your employer may offer a Pension-Linked Emergency Savings Account. This allows you to technically “save” up to $2,500 in a Roth-style account within your 401(k) plan that remains highly liquid. You can withdraw from this account at least once a month without the 10% early-withdrawal penalty, providing a technical “safety valve” for those who are afraid of locking their money away.

When do the new RMD (Required Minimum Distribution) ages stop increasing?

SECURE 2.0 pushed the RMD age to 73 in 2023, and it will technically jump to 75 in 2033. For the professional in 2026, this means you have a significantly longer “Tax-Free Growth Window” than previous generations. This extra time allows for a more patient “Roth Conversion Ladder” strategy, potentially saving hundreds of thousands in lifetime taxes.

Are there tax credits for small businesses starting a plan in 2026?

Absolutely. For companies with 50 or fewer employees, SECURE 2.0 provides a tax credit that can cover 100% of the administrative costs of starting a new plan, up to $5,000 per year for three years. In 2026, there is technically no financial excuse for even the smallest startup to lack a high-quality, auto-enrolled retirement plan for its team.