High-Yield Savings Accounts have become the primary tool for Americans to combat inflation in 2026, offering interest rates that far outpace traditional brick-and-mortar banks and providing a safe haven for emergency funds.

In the financial landscape of 2026, the strategy for managing cash has undergone a technical revolution. For over a decade, “cash was trash” as near-zero interest rates forced investors into risky assets just to preserve purchasing power. Today, however, the stabilization of the federal funds rate has solidified High-Yield Savings Accounts (HYSA) as the primary anchor for liquidity. In 2026, an efficient portfolio is no longer just about stock and bond allocations; it is about the “Yield Optimization” of every idle dollar sitting in a settlement account.

The opportunity cost of financial inertia has reached a record high in 2026. Traditional “zombie accounts” at legacy banks still offer insulting rates of 0.01%, while elite HYSAs are yielding significantly more, creating a massive spread that penalizes the unoptimized. For a household with a $50,000 emergency fund, the difference between a legacy account and a top-tier HYSA can represent thousands of dollars in lost annual income. In 2026, allowing money to sit in a standard checking account is technically considered a “leak” in your financial ship.

This surge in HYSA adoption is also driven by the rise of Automated Cash Sweeps. Most 2026 brokerage platforms and fintech apps now feature “Smart Liquidity” algorithms that automatically move excess cash into the highest-yielding insured account available in real-time. This has transformed savings from a static habit into a dynamic, tech-driven operation. To navigate 2026 finances, one must stop viewing a savings account as a digital shoebox and start treating it as a high-performance liquidity engine.

Technical Mechanics: APY vs. Compounding Frequency

To truly optimize returns in 2026, a professional must look beyond the headline Annual Percentage Yield (APY). While the APY is the standard metric, it is technically a reflection of both the interest rate and the Compounding Frequency. A 5.00% APY compounded daily will yield more actual cash than a 5.00% APY compounded monthly. In 2026, the most competitive institutions utilize “Daily Continuous Compounding,” ensuring that today’s interest begins earning its own interest within 24 hours.

Understanding this nuance is vital for large-scale liquidity management. If you are parking six figures for a short-term goal, such as a 2026 tax payment or a real estate down payment, the compounding delta becomes non-trivial. Furthermore, one must distinguish between the APY (which includes compounding) and the APR (Annual Percentage Rate), which does not. In the 2026 market, high-yield transparency is a legal mandate, but the sophisticated saver still verifies the math before moving capital. When selecting an HYSA in 2026, you must technically audit these four criteria:

- Compounding Frequency: Prioritize daily over monthly to maximize effective yield.

- Transfer Speed (Settlement): Look for accounts integrated with the FedNow or RTP networks for instant liquidity access.

- Platform Security: Ensure the use of passkeys and hardware-level multi-factor authentication (MFA) to protect your “Cash Anchor.”

- Fee Transparency: Verify there are zero maintenance or “excessive transaction” fees, which are becoming obsolete in 2026.

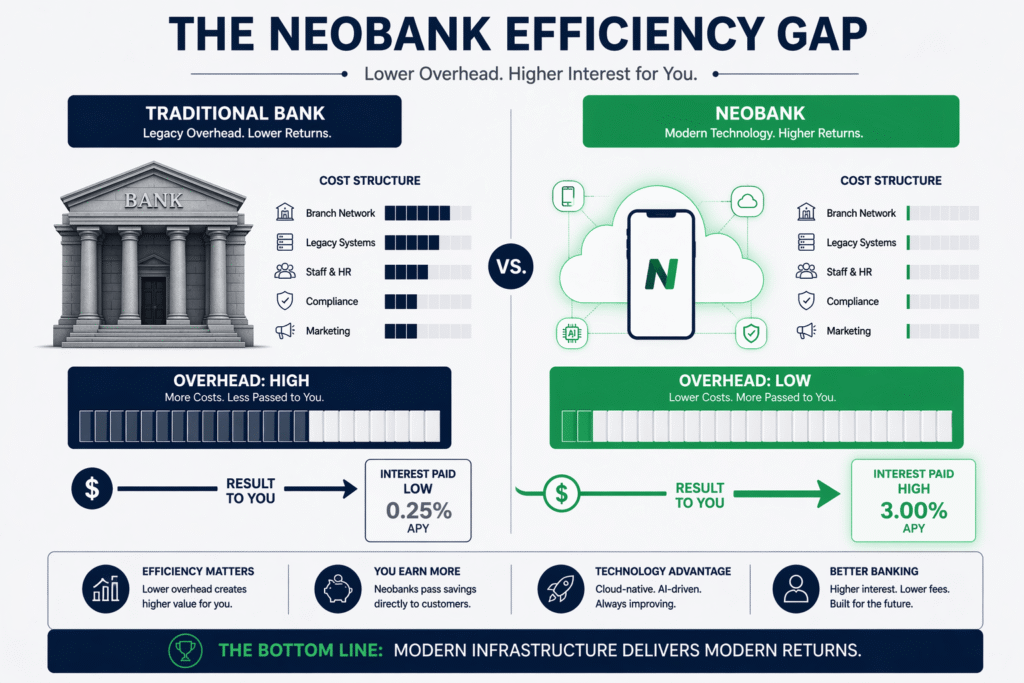

The Neobank Advantage: Infrastructure and Real-Time Settlement

The dominance of Neobanks in the 2026 HYSA market is not an accident; it is an infrastructure advantage. Traditional banks carry the massive overhead of physical branches and legacy mainframe systems from the 1980s. Neobanks, conversely, operate on cloud-native banking cores that allow them to process transactions at a fraction of the cost. This operational efficiency is technically “passed through” to the consumer in the form of higher interest rates, often 10x to 50x the national average.

In 2026, the interest rate you receive is a direct reflection of your bank’s technological efficiency; high-yield is simply the dividend paid for choosing modern infrastructure over legacy bureaucracy.

Beyond rates, the 2026 Neobank advantage lies in Settlement Velocity. Utilizing the matured “Real-Time Payments” (RTP) infrastructure, top-tier HYSAs now allow for the instant movement of funds between different financial institutions. This eliminates the “ACH Lag” of the past, where money was often out of the market for 3 to 5 business days. In 2026, your “Emergency Fund” is truly liquid, available in seconds rather than days, which technically reduces the amount of cash you need to keep in low-yield checking accounts.

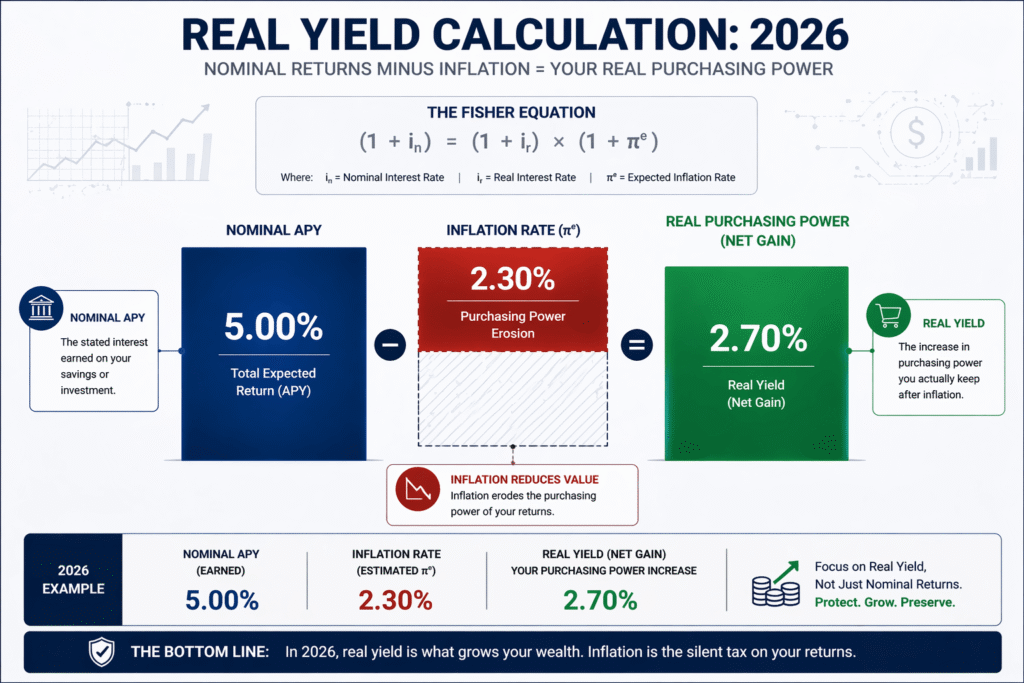

The Inflation-Adjusted Return: Calculating Real Yield

In 2026, the most important number in your dashboard is not the nominal APY, but the Real Yield. A 5% savings account in a 3% inflation environment results in a significantly different outcome than the same account in a 6% inflation environment. To protect your purchasing power, you must technically calculate the inflation-adjusted return of your cash reserves.

The standard method in 2026 for this calculation is the Fisher Equation. By subtracting the projected inflation rate (i) from the nominal interest rate (r), we find the real interest rate (R):

If the resulting R is negative, your “savings” are technically losing value every day. In 2026, the primary goal of an HYSA is to maintain a positive Real Yield, serving as a “Hard Stop” against inflationary erosion. For the strategic professional, this means shifting cash into different tiers of HYSA as the Consumer Price Index (CPI) fluctuates, ensuring that the liquidity layer of the portfolio remains a wealth-preservation tool rather than a slow-leak liability.

Safety and Compliance: FDIC and NCUA Limits in 2026

Safety remains the non-negotiable foundation of the HYSA model. In 2026, the standard FDIC (Federal Deposit Insurance Corporation) insurance limit remains at $250,000 per depositor, per insured bank. For the high-net-worth individual, “Deposit Routing” has become a vital technical strategy. Modern 2026 apps now offer “Fiduciary Sweeps” that automatically distribute deposits across a network of up to 20 different banks, technically providing up to $5,000,000 in aggregate FDIC insurance through a single user interface.

| Account Type | Average Yield (APY) | Technical Advantage | Primary Use Case |

| Traditional Savings | 0.01% – 0.05% | None (Legacy Access) | Minimal Utility |

| National Average | 0.50% – 1.00% | Basic Accessibility | General Consumer |

| Elite HYSA (Neobank) | 4.50% – 5.50%+ | Real-Time Settlement | Emergency Fund / Liquid Reserve |

| Money Market Funds | 4.80% – 5.20% | Institutional Access | Short-term Investment |

FAQ: Maximizing Your HYSA Yield

What are “Teaser Rates” and how do I spot them in 2026?

“Teaser Rates” are high introductory yields (e.g., “6% for the first 3 months”) used to acquire customers. In 2026, you should look for the “Base Rate” in the fine print. Technically, it is often better to choose an account with a stable 5% rate than a 6% teaser that drops to 3% after 90 days, as the cost and “friction” of moving funds manually often eat into the gains.

Does opening an HYSA impact my credit score in 2026?

No. Opening a savings account typically involves a “Soft Pull” of your credit report, which does not impact your FICO score. In 2026, some banks use “ChexSystems” to verify your banking history, but this is technically separate from the credit scoring used for loans. You can switch HYSAs as often as needed to chase higher yields without damaging your creditworthiness.

How are the interests from my HYSA taxed in 2026?

Interest earned in an HYSA is technically treated as Ordinary Income by the IRS. In 2026, you will receive a Form 1099-INT for any account that paid you more than $10 in interest. Because this income is taxed at your marginal rate (which may have increased due to the TCJA sunset), you should always calculate your “After-Tax Yield” when comparing HYSAs to tax-advantaged options like Municipal Bonds.

Are joint HYSAs still a good strategy for couples in 2026?

Yes, primarily because a joint account technically doubles your FDIC coverage to $500,000 at that specific institution. In 2026, most HYSA apps allow for “Sub-Accounts” or “Buckets” within a joint structure, allowing couples to technically segregate their goals (e.g., “Vacation Fund” vs. “Tax Reserve”) while benefiting from the combined interest and insurance limits.

What is “Saving Automation” in the 2026 context?

Modern automation goes beyond “recurring transfers.” In 2026, “Algo-Saving” connects to your checking account, analyzes your spending patterns, and technically identifies “Safe-to-Save” amounts that it moves to your HYSA daily. This ensures you are earning interest on every possible dollar without the risk of overdrawing your primary checking account.

How do “Buckets” or “Vaults” work technically?

In 2026, “Buckets” are logical partitions of a single bank account. They do not have separate account numbers, but the bank’s software allows you to allocate your total balance to specific goals. This is technically superior to having multiple accounts because the interest is usually calculated on the aggregate balance, which can sometimes help you reach higher “Tiered Interest” thresholds more quickly.