FICO 10T is a revolutionary credit scoring model that uses trended data to evaluate your financial behavior over time, offering a more accurate and potentially beneficial score for consistent payers.

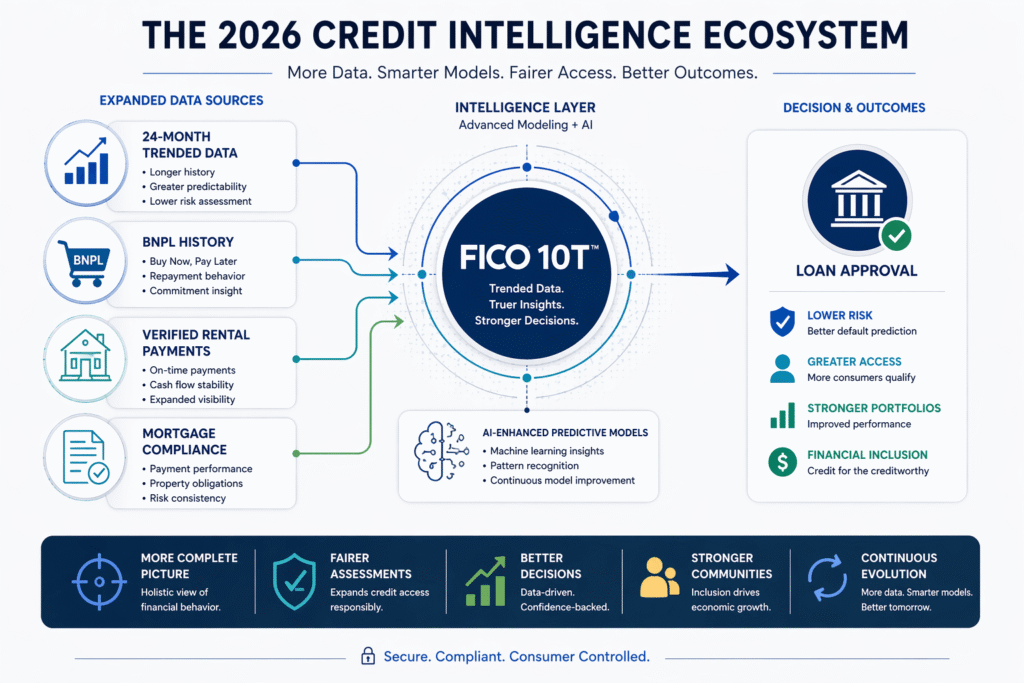

The credit landscape of 2026 has officially transitioned into a more dynamic era with the widespread adoption of the FICO 10T model. For decades, credit scoring operated on a “snapshot” logic, evaluating a consumer’s financial health based on a single point in time. In 2026, however, major lenders have pivoted toward trended data, which provides a panoramic 24-month view of a borrower’s financial trajectory. This shift allows financial institutions to move beyond static numbers and instead analyze the “momentum” of a consumer’s credit behavior, fundamentally changing how risk is assessed in the modern economy.

This evolution is driven by the need for higher predictive precision in an increasingly complex financial environment. Traditional models often failed to distinguish between a consumer who had a one-time spike in credit utilization and one who was systematically accumulating debt. By 2026, FICO 10T has solved this technical bottleneck by incorporating historical payment and balance data over a two-year window. This long-term perspective enables lenders to identify resilient financial patterns, rewarding those who demonstrate consistent deleveraging even if their current “snapshot” shows a temporary dip.

Furthermore, the 2026 credit ecosystem has reached a milestone in regulatory adoption. Following the Federal Housing Finance Agency’s (FHFA) multi-year transition plan, FICO 10T is now being used alongside VantageScore 4.0 for conforming loans sold to Fannie Mae and Freddie Mac. This technical mandate has forced a “surge of adoption” across the mortgage industry in early 2026, ensuring that the most advanced predictive analytics are now the standard for the largest asset class in the American economy.

Technical Breakdown: The Power of Trended Data

The technical core of FICO 10T lies in its ability to parse Trended Credit Bureau Data. Unlike previous versions (like FICO 8 or 9), which primarily looked at the current balance-to-limit ratio, the 10T model evaluates the velocity of that balance over the previous 24+ months. This historical lens allows the algorithm to detect whether a consumer is “trending up” in debt or “trending down” toward financial stability, providing a much more accurate risk profile. In 2026, the FICO 10T algorithm prioritizes four critical variables to determine this trend:

- Balance Trajectory: Whether total debt levels are increasing, decreasing, or remaining stable over the 24-month lookback.

- Payment Consistency: The regularity of monthly payments and the frequency of “total balance” payoffs.

- Credit Utilization Trends: How the ratio of debt-to-available-credit has fluctuated over time, rather than just its current state.

- New Credit Velocity: The frequency and timing of new account openings, analyzed for signs of “credit hunger” or strategic growth.

This multi-dimensional approach technically allows for a more “inclusive” scoring environment. By looking at the long-term trend, the 2026 model can safely approve borrowers who may have had a minor setback a year ago but have since demonstrated an impeccable recovery trajectory. This makes FICO 10T a significantly more powerful tool for lenders who aim to reduce default rates—potentially by as much as 10% for new bankcards—while expanding access to creditworthy individuals.

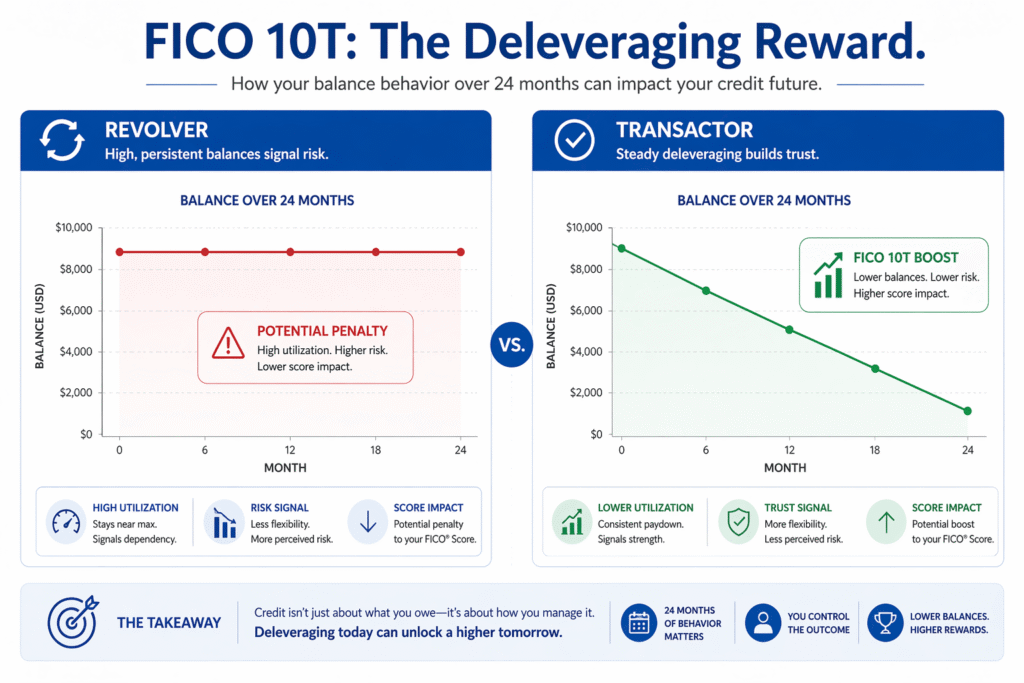

The “Transactor” Advantage vs. The “Revolver” Penalty

One of the most profound impacts of FICO 10T in 2026 is its technical differentiation between “Transactors” and “Revolvers”. Transactors are consumers who use their credit cards but pay off the full balance every month, while Revolvers carry a balance from month to month, accruing interest. Under older FICO models, these two profiles could technically have the same score if their “snapshot” utilization was identical on the day the data was pulled.

In 2026, FICO 10T eliminates this ambiguity. The model technically rewards the Transactor by recognizing their 24-month history of full payoffs as a sign of lower risk. Conversely, Revolvers who consistently carry high balances see a “penalty” in their trended score, as the algorithm interprets the persistent debt as a sign of financial strain. This distinction encourages a “Deleveraging Behavior,” where consumers are incentivized to pay down debt systematically to maintain a high 10T score.

The 2026 FICO 10T model represents a shift toward behavioral rewards; by recognizing the long-term effort of debt reduction, it provides a technical advantage to those who demonstrate consistent financial discipline over time.

Beyond Credit Cards: Integrating BNPL and Rental History

As of early 2026, the FICO 10T ecosystem has expanded to include alternative data sources that were previously invisible to most lenders. A major milestone was reached in March 2026 with the introduction of the “FICO Score 10T BNPL” model, which specifically incorporates Buy Now, Pay Later (BNPL) account data. This allows the millions of consumers who use BNPL services to have their on-time payments contribute to their overall credit score, helping them build “Trended Credit Intelligence” without traditional credit cards.

The 2026 model also places a higher technical value on Rental Payment History. While previous models technically supported rental data, FICO 10T is designed to pull this data more effectively as more landlords and third-party services report it to the bureaus. For “thin-file” borrowers—individuals with little traditional credit history—this rental data can be the technical trigger that moves them from “unscorable” to a “prime” credit rating, significantly expanding their financial opportunities.

Loan Approval Metrics: Impact on Mortgages and HELOCs

The implementation of FICO 10T has had a measurable impact on the Mortgage and Home Equity Line of Credit (HELOC) markets in 2026. Because mortgage lenders are now required to deliver both FICO 10T and VantageScore 4.0 data for loans sold to the Enterprises, the accuracy of interest rate pricing has improved. Borrowers with a “trending down” balance profile are now receiving more competitive rates than they would have under the legacy Classic FICO model.

| Metric | Classic FICO (Legacy) | FICO 10T (2026 Standard) |

| Data Perspective | Static “Point-in-Time” | 24-Month Trended View |

| Default Prediction | Baseline | ~9-10% More Accurate |

| Inclusion Level | Traditional Accounts Only | Includes BNPL & Rental Data |

| “Revolver” Treatment | Utilization-based | Analyzes Balance Velocity |

| Industry Adoption | Phasing out of Mortgages | Mandatory for Enterprises |

FAQ: Optimizing Your Score for the 10T Era

How can I “clean” my balance trajectory for FICO 10T in 2026?

To optimize your score for the 10T era, you must focus on consistent debt reduction. Because the model looks at a 24-month window, a single month of aggressive payment isn’t as effective as a steady, downward trend in total balances. Avoid “yo-yoing”—the practice of paying off a card only to max it out again the next month—as this “utilization volatility” is technically penalized under the trended model.

Does a 2026 Personal Loan impact my 10T score differently?

Yes. FICO 10T is better at recognizing debt consolidation. If you take out a personal loan to pay off high-interest credit card debt, the older models might have dinged you for “new credit.” In 2026, FICO 10T technically recognizes the downward trend in credit card balances as a positive signal, potentially offsetting the “new credit” ding much faster.

Are all banks using FICO 10T in 2026?

While the mortgage industry (Fannie Mae/Freddie Mac) has made a massive push, the transition is multi-year. Most major credit card issuers and auto lenders in 2026 are currently running “dual-scoring” systems—using both FICO 8/9 and FICO 10T—as they recalibrate their internal risk models. You should prepare for both, but focus on the 24-month trend to be safe across all platforms.

What happens to my score if I use BNPL in 2026?

Under the new “FICO Score 10T BNPL” rules, your BNPL accounts will start showing up on your credit report. If you pay these on time, they will technically build a positive trended history. However, because these are short-term loans, a high volume of new BNPL “openings” can look like “credit hunger,” so it is best to use them strategically rather than for every minor purchase.

How do I contest “incorrect trends” on my 2026 report?

Contesting trended data is more complex than contesting a single late payment. You must ensure that the historical balance reported for each of the 24 months is accurate. If a credit card issuer mistakenly reported a high balance for several months where you were actually lower, you must provide bank statements for those specific months to the bureaus to trigger a technical “Trend Correction”.

Can my rental history help my score if my landlord doesn’t report it?

Technically, no. FICO 10T can only score what is on the credit report. In 2026, many tenants use third-party “Rent Reporting” services that verify their bank transactions and push that data to the CRAs (Consumer Reporting Agencies). If you want your on-time rent to boost your 10T score, you must ensure that your data is being “furnished” to the bureaus through one of these verified channels.